Bank of America 2010 Annual Report Download - page 227

Download and view the complete annual report

Please find page 227 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

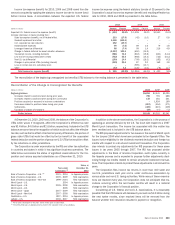

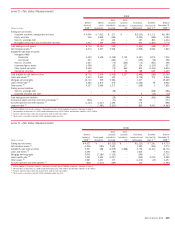

Trading Account Assets and Liabilities and Available-for-Sale

Debt Securities

The fair values of trading account assets and liabilities are primarily based on

actively traded markets where prices are based on either direct market quotes

or observed transactions. The fair values of AFS debt securities are generally

based on quoted market prices or market prices for similar assets. Liquidity is

a significant factor in the determination of the fair values of trading account

assets and liabilities and AFS debt securities. Market price quotes may not be

readily available for some positions, or positions within a market sector where

trading activity has slowed significantly or ceased. Some of these instruments

are valued using a discounted cash flow model, which estimates the fair value

of the securities using internal credit risk, interest rate and prepayment risk

models that incorporate management’s best estimate of current key assump-

tions such as default rates, loss severity and prepayment rates. Principal and

interest cash flows are discounted using an observable discount rate for

similar instruments with adjustments that management believes a market

participant would consider in determining fair value for the specific security.

Others are valued using a net asset value approach which considers the value

of the underlying securities. Underlying assets are valued using external

pricing services, where available, or matrix pricing based on the vintages

and ratings. Situations of illiquidity generally are triggered by the market’s

perception of credit uncertainty regarding a single company or a specific

market sector. In these instances, fair value is determined based on limited

available market information and other factors, principally from reviewing the

issuer’s financial statements and changes in credit ratings made by one or

more ratings agencies.

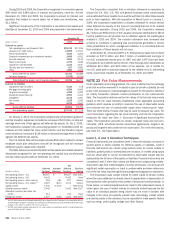

Derivative Assets and Liabilities

The fair values of derivative assets and liabilities traded in the

over-the-counter (OTC) market are determined using quantitative models that

utilize multiple market inputs including interest rates, prices and indices to

generate continuous yield or pricing curves and volatility factors to value the

position. The majority of market inputs are actively quoted and can be

validated through external sources, including brokers, market transactions

and third-party pricing services. Estimation risk is greater for derivative asset

and liability positions that are either option-based or have longer maturity

dates where observable market inputs are less readily available or are

unobservable, in which case, quantitative-based extrapolations of rate, price

or index scenarios are used in determining fair values. The fair values of

derivative assets and liabilities include adjustments for market liquidity,

counterparty credit quality and other deal specific factors, where appropriate.

The Corporation incorporates within its fair value measurements of OTC

derivatives the net credit differential between the counterparty credit risk

and the Corporation’s own credit risk. An estimate of severity of loss is also

used in the determination of fair value, primarily based on market data.

Corporate Loans and Loan Commitments

The fair values of loans and loan commitments are based on market prices,

where available, or discounted cash flow analyses using market-based credit

spreads of comparable debt instruments or credit derivatives of the specific

borrower or comparable borrowers. Results of discounted cash flow calcula-

tions may be adjusted, as appropriate, to reflect other market conditions or

the perceived credit risk of the borrower.

Mortgage Servicing Rights

The fair values of MSRs are determined using models that rely on estimates

of prepayment rates, the resultant weighted-average lives of the MSRs and

the OAS levels. For more information on MSRs, see Note 25 – Mortgage

Servicing Rights.

Loans Held-for-Sale

The fair values of LHFS are based on quoted market prices, where available,

or are determined by discounting estimated cash flows using interest rates

approximating the Corporation’s current origination rates for similar loans

adjusted to reflect the inherent credit risk.

Other Assets

The fair values of AFS marketable equity securities are generally based on

quoted market prices or market prices for similar assets. However, non-public

investments are initially valued at the transaction price and subsequently

adjusted when evidence is available to support such adjustments.

Securities Financing Agreements

The fair values of certain reverse repurchase agreements, repurchase agree-

ments and securities borrowed transactions are determined using quantita-

tive models, including discounted cash flow models that require the use of

multiple market inputs including interest rates and spreads to generate

continuous yield or pricing curves, and volatility factors. The majority of market

inputs are actively quoted and can be validated through external sources,

including brokers, market transactions and third-party pricing services.

Deposits, Commercial Paper and Other Short-term

Borrowings

The fair values of deposits, commercial paper and other short-term borrow-

ings are determined using quantitative models, including discounted cash

flow models that require the use of multiple market inputs including interest

rates and spreads to generate continuous yield or pricing curves, and volatility

factors. The majority of market inputs are actively quoted and can be validated

through external sources, including brokers, market transactions and third-

party pricing services. The Corporation considers the impact of its own credit

spreads in the valuation of these liabilities. The credit risk is determined by

reference to observable credit spreads in the secondary cash market.

Long-term Borrowings

The Corporation issues structured notes that have coupons or repayment

terms linked to the performance of debt or equity securities, indices, curren-

cies or commodities. The fair value of structured notes is estimated using

valuation models for the combined derivative and debt portions of the notes

accounted for under the fair value option. These models incorporate observ-

able and, in some instances, unobservable inputs including security prices,

interest rate yield curves, option volatility, currency, commodity or equity rates

and correlations between these inputs. The impact of the Corporation’s own

credit spreads is also included based on the Corporation’s observed sec-

ondary bond market spreads.

Asset-backed Secured Financings

The fair values of asset-backed secured financings are based on external

broker bids, where available, or are determined by discounting estimated cash

flows using interest rates approximating the Corporation’s current origination

rates for similar loans adjusted to reflect the inherent credit risk.

Bank of America 2010 225