Bank of America 2010 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

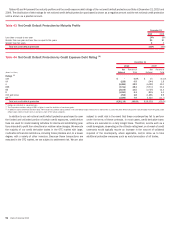

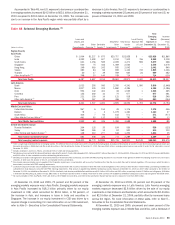

Allowance for Credit Losses

Allowance for Loan and Lease Losses

The allowance for loan and lease losses is allocated based on two compo-

nents, described below, based on whether a loan or lease is performing or

whether it has been individually identified as being impaired or has been

modified as a TDR. We evaluate the adequacy of the allowance for loan and

lease losses based on the total of these two components. The allowance for

loan and lease losses excludes loans held-for-sale and loans accounted for

under the fair value option, as fair value adjustments related to loans

measured at fair value include a credit risk component.

The first component of the allowance for loan and lease losses covers

nonperforming commercial loans, consumer real estate loans that have been

modified in a TDR, renegotiated credit card, unsecured consumer and small

business loans. These loans are subject to impairment measurement prima-

rily at the loan level based either on the present value of expected future cash

flows discounted at the loan’s original effective interest rate, or discounted at

the portfolio average contractual annual percentage rate, excluding renego-

tiated and promotionally priced loans for the renegotiated TDR portfolio.

Impairment measurement may also be based upon the collateral value or the

loan’s observable market price. When the determined or measured values are

lower than the carrying value of the loan, impairment is recognized. For

purposes of computing this specific loss component of the allowance, larger

impaired loans are evaluated individually and smaller impaired loans are

evaluated as a pool using historical loss experience for the respective product

types and risk ratings of the loans.

The second component of the allowance for loan and lease losses covers

performing consumer and commercial loans and leases which have incurred

losses that are not yet individually identifiable. The allowance for consumer

and certain homogeneous commercial loan and lease products is based on

aggregated portfolio evaluations, generally by product type. Loss forecast

models are utilized that consider a variety of factors including, but not limited

to, historical loss experience, estimated defaults or foreclosures based on

portfolio trends, delinquencies, economic trends and credit scores. Our

consumer real estate loss forecast model estimates the portion of our

homogeneous loans that will default based on individual loan attributes,

the most significant of which are refreshed LTV or CLTV, borrower credit score

as well as vintage and geography, all of which are further broken down into

current delinquency status. Incorporating refreshed LTV and CLTV into our

probability of default allows us to factor the impact of changes in home prices

into our allowance for loan and lease losses. These loss forecast models are

updated on a quarterly basis to incorporate information reflecting the current

economic environment. Included within this second component of the allow-

ance for loan and lease losses and determined separately from the proce-

dures outlined above are reserves which are maintained to cover uncertain-

ties that affect our estimate of probable losses including domestic and global

economic uncertainty and large single name defaults. We evaluate the ad-

equacy of the allowance for loan and lease losses based on the combined

total of these two components. As of December 31, 2010, inputs to the loss

forecast process resulted in reductions in the allowance for most consumer

portfolios.

The allowance for commercial loan and lease losses is established by

product type after analyzing historical loss experience by internal risk rating,

current economic conditions, industry performance trends, geographic or

obligor concentrations within each portfolio segment, and any other pertinent

information. The statistical models for commercial loans are generally up-

dated annually and utilize the Corporation’s historical database of actual

defaults and other data. The loan risk ratings and composition of the com-

mercial portfolios are updated at least quarterly to incorporate the most

recent data reflecting the current economic environment. For risk-rated com-

mercial loans, we estimate the probability of default (PD) and the loss given

default (LGD) based on the Corporation’s historical experience of defaults and

credit losses. Factors considered when assessing the internal risk rating

include the value of the underlying collateral, if applicable; the industry in

which the obligor operates; the obligor’s liquidity and other financial indica-

tors; and other quantitative and qualitative factors relevant to the obligor’s

credit risk. When estimating the allowance for loan and lease losses, man-

agement relies not only on models derived from historical experience but also

on its judgment in considering the effect on probable losses inherent in the

portfolios due to the current macroeconomic environment and trends, inher-

ent uncertainty in models, and other qualitative factors. As of December 31,

2010, updates to the loan risk ratings and composition resulted in reductions

in the allowance for all commercial portfolios.

We monitor differences between estimated and actual incurred loan and

lease losses. This monitoring process includes periodic assessments by

senior management of loan and lease portfolios and the models used to

estimate incurred losses in those portfolios.

Additions to, or reductions of, the allowance for loan and lease losses

generally are recorded through charges or credits to the provision for credit

losses. Credit exposures deemed to be uncollectible are charged against the

allowance for loan and lease losses. Recoveries of previously charged off

amounts are credited to the allowance for loan and lease losses.

The allowance for loan and lease losses for the consumer portfolio as

presented in Table 51 was $34.7 billion at December 31, 2010, an increase

of $6.9 billion from December 31, 2009. This increase was primarily related

to $10.8 billion of reserves recorded on January 1, 2010 in connection with

the adoption of new consolidation guidance, and higher reserve additions in

the non-impaired consumer real estate portfolios during the first half of 2010

amid continued stress in the housing market. These items were partially

offset by reserve reductions primarily due to improving credit quality in the

Global Card Services consumer portfolios. With respect to the consumer PCI

loan portfolios, updates to our expected principal cash flows resulted in an

increase in reserves through provision of $2.2 billion for 2010, primarily in the

home equity and discontinued real estate portfolios compared to $3.5 billion

in 2009.

The allowance for commercial loan and lease losses was $7.2 billion at

December 31, 2010, a $2.2 billion decrease from December 31, 2009. The

decrease was primarily due to improvements in the U.S. small business

commercial portfolio within Global Card Services due to improved delinquen-

cies and bankruptcies, as well as in the U.S. commercial portfolios primarily in

Global Commercial Banking and GBAM, and the commercial real estate

portfolio primarily within Global Commercial Banking reflecting improved bor-

rower credit profiles as a result of improving economic conditions.

The allowance for loan and lease losses as a percentage of total loans and

leases outstanding was 4.47 percent at December 31, 2010 compared to

4.16 percent at December 31, 2009. The increase in the ratio was mostly due

to consumer reserve increases for securitized loans consolidated under the

new consolidation guidance, which were primarily credit card loans. The

December 31, 2010 and 2009 ratios above include the impact of the PCI

loan portfolio. Excluding the PCI loan portfolio, the allowance for loan and

lease losses as a percentage of total loans and leases outstanding was

3.94 percent at December 31, 2010 compared to 3.88 percent at Decem-

ber 31, 2009.

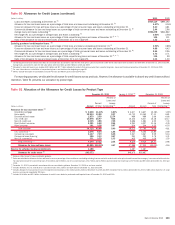

Reserve for Unfunded Lending Commitments

In addition to the allowance for loan and lease losses, we also estimate

probable losses related to unfunded lending commitments such as letters of

credit, financial guarantees and binding loan commitments, excluding com-

mitments accounted for under the fair value option. Unfunded lending com-

mitments are subject to the same assessment as funded loans, including

estimates of PD and LGD. Due to the nature of unfunded commitments, the

Bank of America 2010 101