Bank of America 2010 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

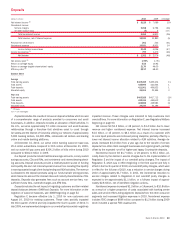

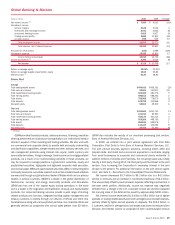

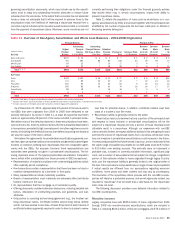

GWIM results include the impact of migrating clients and their related

deposit and loan balances to or from Deposits,Home Loans & Insurance and

the ALM portfolio as presented in the table below. The directional shift of total

deposits migrated was mainly due to client segmentation threshold changes.

Subsequent to the date of migration, the associated net interest income,

noninterest income and noninterest expense are recorded in the business to

which the clients migrated.

Migration Summary

(Dollars in millions)

2010 2009

Average

Total deposits – GWIM from (to) Deposits

$3,086

$(30,638)

Total loans – GWIM to Home Loans & Insurance and the

ALM portfolio

(1,405)

(12,033)

Year end

Total deposits – GWIM from (to) Deposits

$7,232

$(42,521)

Total loans – GWIM to Home Loans & Insurance and the

ALM portfolio

(1,625)

(17,241)

Net income decreased $369 million, or 22 percent, to $1.3 billion driven

in part by higher noninterest expense, the tax-related effect of the sale of the

Columbia Management long-term asset management business and lower net

interest income, partially offset by higher noninterest income and lower credit

costs. Net interest income decreased $157 million, or three percent, to

$5.8 billion as the positive impact of higher deposit levels was more than

offset by lower revenue from corporate ALM activity. Noninterest income

increased $691 million, or seven percent, to $10.8 billion primarily due to

higher asset management fees driven by stronger markets, continued long-

term assets under management flows and higher transactional activity. Pro-

vision for credit losses decreased $415 million, or 39 percent, to $646 million

driven by stabilization of the portfolios and the recognition of a single large

commercial charge-off in 2009. Noninterest expense increased $1.2 billion,

or 10 percent, to $13.6 billion driven by increases in revenue-related ex-

penses, higher support costs and personnel costs associated with further

investment in the business.

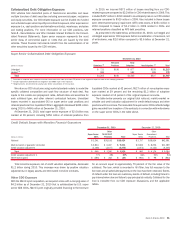

Client Balances

The table below presents client balances which consist of assets under

management, client brokerage assets, assets in custody, client deposits,

and loans and leases.

Client Balances by Type

(Dollars in millions)

2010 2009

December 31

Assets under management

$ 643,955

$749,851

Client brokerage assets

(1)

1,480,231

1,402,977

Assets in custody

126,203

144,012

Client deposits

266,444

224,839

Loans and leases

101,020

99,571

Less: Client brokerage assets, assets in custody

and deposits included in assets under

management

(379,310)

(348,738)

Total client balances

(2)

$2,238,543

$2,272,512

(1)

Client brokerage assets include non-discretionary brokerage and fee-based assets.

(2)

2009 balance includes the Columbia Management long-term asset management business representing

$114.6 billion, net of eliminations, which was sold on May 1, 2010.

The decrease in client balances was due to the sale of the Columbia

Management long-term asset management business, outflows in MLGWM’s

non-fee based brokerage assets and outflows in BACM’s money market

assets due to the continued low rate environment, partially offset by higher

market levels and inflows in client deposits, long-term assets under man-

agement (AUM) and fee-based brokerage assets.

Bank of America 2010 53