Bank of America 2010 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

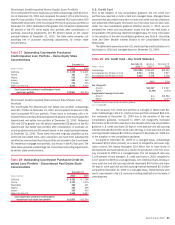

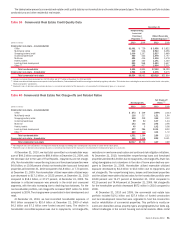

performing at December 31, 2010. Discontinued real estate TDRs deemed

collateral dependent totaled $213 million at December 31, 2010 and in-

cluded $97 million of loans classified as nonperforming and $116 million

classified as performing.

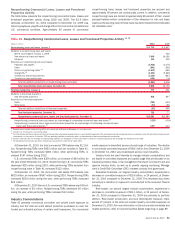

We also work with customers that are experiencing financial difficulty by

renegotiating credit card, consumer lending and small business loans (the

renegotiated TDR portfolio), while complying with Federal Financial Institutions

Examination Council (FFIEC) guidelines. Substantially all renegotiated portfo-

lio modifications are considered to be TDRs. The renegotiated TDR portfolio

may include modifications, both short- and long-term, of interest rates or

payment amounts or a combination of interest rates and payment amounts.

We make modifications primarily through internal renegotiation programs

utilizing direct customer contact, but may also utilize external renegotiation

programs. The renegotiated TDR portfolio is excluded from Table 33 as we do

not generally classify consumer non-real estate loans as nonperforming. At

December 31, 2010, our renegotiated TDR portfolio was $12.1 billion of

which $9.2 billion was current or less than 30 days past due under the

modified terms, compared to an $8.1 billion portfolio, on a held basis at

December 31, 2009, of which $5.9 billion was current or less than 30 days

past due under the modified terms. At December 31, 2009, our renegotiated

TDR portfolio, on a managed basis, was $15.8 billion of which $11.5 billion

was current or less than 30 days past due under the modified terms. For more

information on the renegotiated TDR portfolio, see Note 6 – Outstanding

Loans and Leases to the Consolidated Financial Statements.

As a result of new accounting guidance on PCI loans, beginning January 1,

2010, modifications of loans in the PCI loan portfolio do not result in removal

of the loan from the PCI loan pool. TDRs in the consumer real estate portfolio

that were removed from the PCI loan portfolio prior to the adoption of new

accounting guidance were $2.1 billion and $2.3 billion at December 31, 2010

and 2009, of which $426 million and $395 million were nonperforming.

These nonperforming loans are excluded from the table below.

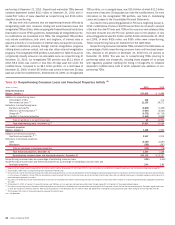

Nonperforming consumer real estate TDRs, included in the table below, as

a percentage of total nonperforming consumer loans and foreclosed proper-

ties, declined to 16 percent at December 31, 2010 from 21 percent at

December 31, 2009. This was due to nonperforming TDRs returning to

performing status and charge-offs, including those charged off to comply

with regulatory guidance clarifying the timing of charge-offs on collateral

dependent modified loans, both of which outpaced new additions of non-

performing TDRs.

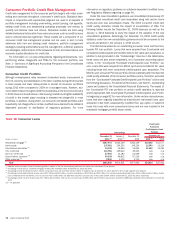

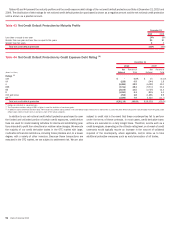

Table 33 Nonperforming Consumer Loans and Foreclosed Properties Activity

(1)

(Dollars in millions)

2010 2009

Nonperforming loans

Balance, January 1

$20,839

$9,888

Additions to nonperforming loans:

Consolidation of VIEs

448

n/a

New nonaccrual loans

(2)

21,136

29,271

Reductions in nonperforming loans:

Paydowns and payoffs

(2,809)

(1,459)

Returns to performing status

(3)

(7,647)

(4,540)

Charge-offs

(4)

(9,772)

(10,702)

Transfers to foreclosed properties

(1,341)

(1,619)

Total net additions to nonperforming loans

15

10,951

Total nonperforming loans, December 31

(5)

20,854

20,839

Foreclosed properties

Balance, January 1

1,428

1,506

Additions to foreclosed properties:

New foreclosed properties

(6, 7)

2,337

1,976

Reductions in foreclosed properties:

Sales

(2,327)

(1,687)

Write-downs

(189)

(367)

Total net reductions to foreclosed properties

(179)

(78)

Total foreclosed properties, December 31

1,249

1,428

Nonperforming consumer loans and foreclosed properties, December 31

$22,103

$22,267

Nonperforming consumer loans as a percentage of outstanding consumer loans

3.24%

3.61%

Nonperforming consumer loans and foreclosed properties as a percentage of outstanding consumer loans and

foreclosed properties

3.43

3.85

(1)

Balances do not include nonperforming LHFS of $1.0 billion and $1.6 billion at December 31, 2010 and 2009. For more information on our definition of nonperforming loans, see the discussion beginning on page 85.

(2)

2009 includes $465 million of nonperforming loans acquired from Merrill Lynch.

(3)

Consumer loans may be returned to performing status when all principal and interest is current and full repayment of the remaining contractual principal and interest is expected, or when the loan otherwise becomes well-secured and

is in the process of collection. Certain TDRs are classified as nonperforming at the time of restructure and may only be returned to performing status after considering the borrower’s sustained repayment performance for a

reasonable period, generally six months.

(4)

Our policy is not to classify consumer credit card and consumer loans not secured by real estate as nonperforming; therefore, the charge-offs on these loans have no impact on nonperforming activity and accordingly are excluded from

this table.

(5)

At December 31, 2010, 67 percent of nonperforming loans are 180 days or more past due and have been written down through charge-offs to 69 percent of the unpaid principal balance.

(6)

Our policy is to record any losses in the value of foreclosed properties as a reduction in the allowance for loan and lease losses during the first 90 days after transfer of a loan into foreclosed properties. Thereafter, all gains and losses

in value are recorded in noninterest expense. New foreclosed properties in the table above are net of $575 million and $818 million of charge-offs during 2010 and 2009, taken during the first 90 days after transfer.

(7)

2009 includes $21 million of foreclosed properties acquired from Merrill Lynch.

n/a = not applicable

86 Bank of America 2010