Bank of America 2010 Annual Report Download - page 175

Download and view the complete annual report

Please find page 175 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

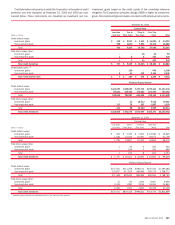

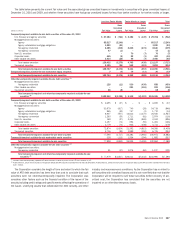

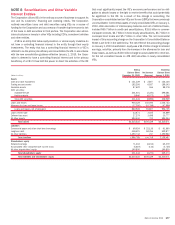

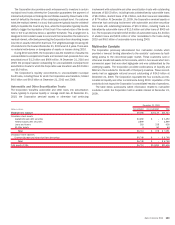

The following tables present impaired loans related to the Corporation’s home loans and commercial loan portfolio segments at December 31, 2010.

Certain impaired home loans and commercial loans do not have a related allowance as the valuation of these impaired loans, determined under current

accounting guidance, exceeded the carrying value.

Impaired Loans – Home Loans

(Dollars in millions)

Unpaid

Principal

Balance

Carrying

Value

Related

Allowance

Average

Carrying

Value

Interest

Income

Recognized

(1)

December 31, 2010 2010

With no recorded allowance

Residential mortgage $ 5,493 $ 4,382 n/a $4,429 $184

Home equity 1,411 437 n/a 493 21

Discontinued real estate 361 218 n/a 219 8

With an allowance recorded

Residential mortgage $ 8,593 $ 7,406 $1,154 $5,226 $196

Home equity 1,521 1,284 676 1,509 23

Discontinued real estate 247 177 41 170 7

Total

Residential mortgage $14,086 $11,788 $1,154 $9,655 $380

Home equity 2,932 1,721 676 2,002 44

Discontinued real estate 608 395 41 389 15

(1)

Interest income recognized includes interest accrued and collected on the outstanding balances of accruing impaired loans as well as interest cash collections on nonaccruing impaired loans for which the ultimate collectability of

principal is not uncertain. See Note 1 – Summary of Significant Accounting Principles for additional information.

n/a = not applicable

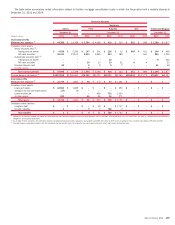

Impaired Loans – Commercial

(Dollars in millions)

Unpaid

Principal

Balance

Carrying

Value

Related

Allowance

Average

Carrying

Value

Interest

Income

Recognized

(1)

December 31, 2010 2010

With no recorded allowance

U.S. commercial $ 968 $ 441 n/a $ 547 $ 3

Commercial real estate 2,655 1,771 n/a 1,736 8

Non-U.S. commercial 46 28 n/a 9 –

U.S. small business commercial

(2)

– – n/a – –

With an allowance recorded

U.S. commercial $3,891 $3,193 $336 $3,389 $36

Commercial real estate 5,682 4,103 208 4,813 29

Non-U.S. commercial 572 217 91 190 –

U.S. small business commercial

(2)

935 892 445 1,028 34

Total

U.S. commercial $4,859 $3,634 $336 $3,936 $39

Commercial real estate 8,337 5,874 208 6,549 37

Non-U.S. commercial 618 245 91 199 –

U.S. small business commercial

(2)

935 892 445 1,028 34

(1)

Interest income recognized includes interest accrued and collected on the outstanding balances of accruing impaired loans as well as interest cash collections on nonaccruing impaired loans for which the ultimate collectability of

principal is not uncertain. See Note 1 – Summary of Significant Accounting Principles for additional information.

(2)

Includes U.S. small business commercial renegotiated TDR loans and related allowance.

n/a = not applicable

At December 31, 2010 and 2009, remaining commitments to lend ad-

ditional funds to debtors whose terms have been modified in a commercial or

consumer TDR were immaterial.

The Corporation seeks to assist customers that are experiencing financial

difficulty by renegotiating loans within the renegotiated portfolio while ensur-

ing compliance with Federal Financial Institutions Examination Council (FFIEC)

guidelines. Substantially all modifications in the renegotiated portfolio are

considered to be both TDRs and impaired loans. The renegotiated portfolio

may include modifications, both short- and long-term, of interest rates or

payment amounts or a combination thereof. The Corporation makes loan

modifications, primarily utilizing internal renegotiation programs via direct

customer contact, that manage customers’ debt exposures held only by the

Corporation. Additionally, the Corporation makes loan modifications with

consumers who have elected to work with external renegotiation agencies

and these modifications provide solutions to customers’ entire unsecured

debt structures. Under both internal and external programs, customers

receive reduced annual percentage rates with fixed payments that amortize

loan balances over a 60-month period. Under both programs, for credit card

loans, a customer’s charging privileges are revoked.

Bank of America 2010 173