Bank of America 2010 Annual Report Download - page 189

Download and view the complete annual report

Please find page 189 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

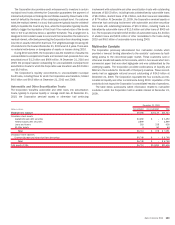

Leveraged Lease Trusts

The Corporation’s net investment in consolidated leveraged lease trusts

totaled $5.2 billion and $5.6 billion at December 31, 2010 and 2009. The

trusts hold long-lived equipment such as rail cars, power generation and

distribution equipment, and commercial aircraft. The Corporation structures

the trusts and holds a significant residual interest. The net investment

represents the Corporation’s maximum loss exposure to the trusts in the

unlikely event that the leveraged lease investments become worthless. Debt

issued by the leveraged lease trusts is nonrecourse to the Corporation. The

Corporation has no liquidity exposure to these leveraged lease trusts.

Asset Acquisition Conduits

The Corporation currently administers two asset acquisition conduits which

acquire assets on behalf of the Corporation or its customers. The Corporation

liquidated a third conduit during 2010. Liquidation of the conduit did not

impact the Corporation’s consolidated results of operations. These conduits

had total assets of $640 million and $2.2 billion at December 31, 2010 and

2009. One of the conduits acquires assets at the request of customers who

wish to benefit from the economic returns of the specified assets on a

leveraged basis, which consist principally of liquid exchange-traded equity

securities. The second conduit holds subordinate AFS debt securities for the

Corporation’s benefit. The conduits obtain funding by issuing commercial

paper and subordinate certificates to third-party investors. Repayment of the

commercial paper and certificates is assured by total return swaps between

the Corporation and the conduits. When a conduit acquires assets for the

benefit of the Corporation’s customers, the Corporation enters into

back-to-back total return swaps with the conduit and the customer such that

the economic returns of the assets are passed through to the customer. The

Corporation’s exposure to the counterparty credit risk of its customers is

mitigated by the ability to liquidate an asset held in the conduit if the customer

defaults on its obligation. The Corporation receives fees for serving as

commercial paper placement agent and for providing administrative services

to the conduits. At December 31, 2010 and 2009, the Corporation did not

hold any commercial paper issued by the asset acquisition conduits other

than incidentally and in its role as a commercial paper dealer.

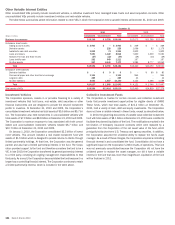

Real Estate Vehicles

The Corporation held investments in unconsolidated real estate vehicles of

$5.4 billion and $4.8 billion at December 31, 2010 and 2009, which con-

sisted of limited partnership investments in unconsolidated limited partner-

ships that finance the construction and rehabilitation of affordable rental

housing. An unrelated third party is typically the general partner and has

control over the significant activities of the partnership. The Corporation earns

a return primarily through the receipt of tax credits allocated to the affordable

housing projects. The Corporation’s risk of loss is mitigated by policies

requiring that the project qualify for the expected tax credits prior to making

its investment. The Corporation may from time to time be asked to invest

additional amounts to support a troubled project. Such additional invest-

ments have not been and are not expected to be significant.

Other Transactions

In 2010 and prior years, the Corporation transferred pools of securities to

certain independent third parties and provided financing for approximately

75 percent of the purchase price under asset-backed financing arrangements.

At December 31, 2010 and 2009, the Corporation’s maximum loss exposure

under these financing arrangements was $6.5 billion and $6.8 billion, sub-

stantially all of which was classified as loans on the Corporation’s Consol-

idated Balance Sheet. All principal and interest payments have been received

when due in accordance with their contractual terms. These arrangements are

not included in the table on page 186 because the purchasers are not VIEs.

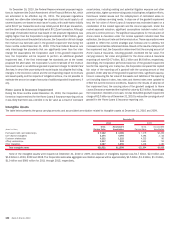

NOTE 9 Representations and Warranties

Obligations and Corporate Guarantees

Background

The Corporation securitizes first-lien residential mortgage loans, generally in the

form of MBS guaranteed by GSEs or GNMA in the case of FHA-insured and VA-

guaranteed mortgage loans. In addition, in prior years, legacy companies and

certain subsidiaries have sold pools of first-lien residential mortgage loans,

home equity loans and other second-lien loans as private-label securitizations

or in the form of whole loans. In connection with these transactions, the

Corporation or certain subsidiaries or legacy companies made various repre-

sentations and warranties. These representations and warranties, as governed

by the agreements, related to, among other things, the ownership of the loan,

the validity of the lien securing the loan, the absence of delinquent taxes or liens

against the property securing the loan, the process used to select the loan for

inclusion in a transaction, the loan’s compliance with any applicable loan

criteria, including underwriting standards, and the loan’s compliance with

applicable federal, state and local laws. Breaches of these representations

and warranties may result in a requirement to repurchase mortgage loans, or to

otherwise make whole or provide other remedy to a whole-loan buyer or

securitization trust. In such cases, the Corporation would be exposed to any

subsequent credit loss on the mortgage loans. The Corporation’s credit loss

would be reduced by any recourse to sellers of loans (i.e., correspondents) for

representations and warranties previously provided. When a loan was origi-

nated by a third-party correspondent, the Corporation typically has the right to

seek a recovery of related repurchase losses from the correspondent origina-

tor. At December 31, 2010, loans purchased from correspondents comprised

approximately 25 percent of loans underlying outstanding repurchase de-

mands. During 2010, the Corporation experienced a decrease in recoveries

from correspondents, however, the actual recovery rate may vary from period to

period based upon the underlying mix of correspondents (e.g., active, inactive,

out-of-business originators) from which recoveries are sought.

Subject to the requirements and limitations of the applicable agreements,

these representations and warranties can be enforced by the securitization

trustee or the whole-loan buyer as governed by the applicable agreement or, in

certain first-lien and home equity securitizations where monolines have

insured all or some of the related bonds issued, by the monoline insurer

at any time over the life of the loan. Importantly, in the case of non-GSE loans,

the contractual liability to repurchase arises if there is a breach of the

representations and warranties that materially and adversely affects the

interest of all investors, or if there is a breach of other standards established

by the terms of the related sale agreement. The Corporation believes that the

longer a loan performs prior to default, the less likely it is that an alleged

underwriting breach of representations and warranties had a material impact

on the loan’s performance. Historically, most demands for repurchase have

occurred within the first few years after origination, generally after a loan has

defaulted. However, in recent periods the time horizon has lengthened due to

increased repurchase request activity across all vintages.

The Corporation’s current operations are structured to limit the risk of

repurchase and accompanying credit exposure by seeking to ensure consis-

tent production of mortgages in accordance with its underwriting procedures

and by servicing those mortgages consistent with its contractual obligations.

In addition, certain securitizations include guarantees written to protect

certain purchasers of the loans from credit losses up to a specified amount.

The fair value of the probable losses to be absorbed under the representa-

tions and warranties obligations and the guarantees is recorded as an

accrued liability when the loans are sold. The liability for probable losses is

updated by accruing a representations and warranties provision in mortgage

banking income throughout the life of the loan as necessary when additional

relevant information becomes available. The methodology used to estimate

Bank of America 2010 187