Bank of America 2010 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

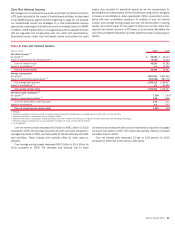

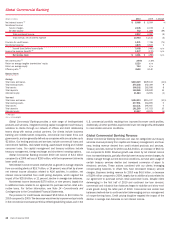

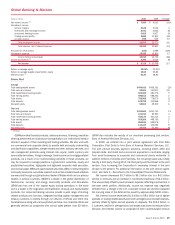

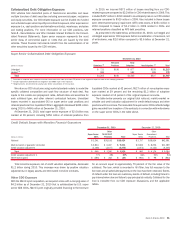

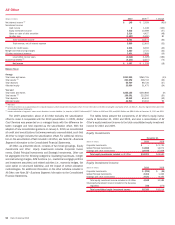

Home Loans & Insurance Key Statistics

(Dollars in millions, except as noted)

2010 2009

Loan production

Home Loans & Insurance:

First mortgage

$287,236

$354,506

Home equity

7,626

10,488

Total Corporation

(1)

:

First mortgage

298,038

378,105

Home equity

8,437

13,214

Year end

Mortgage servicing portfolio (in billions)

(2)

$2,057

$2,151

Mortgage loans serviced for investors (in billions)

1,628

1,716

Mortgage servicing rights:

Balance

14,900

19,465

Capitalized mortgage servicing rights (% of

loans serviced for investors)

92bps

113bps

(1)

In addition to loan production in Home Loans & Insurance, the remaining first mortgage and home equity loan

production is primarily in GWIM.

(2)

Servicing of residential mortgage loans, home equity lines of credit, home equity loans and discontinued real

estate mortgage loans.

First mortgage production in Home Loans & Insurance was $287.2 billion

in 2010 compared to $354.5 billion in 2009. The decrease of $67.3 billion

was primarily due to a drop in the overall size of the mortgage market driven by

weaker market demand for both refinance and purchase transactions com-

bined with a decrease in market share. Home equity production was $7.6 bil-

lion in 2010 compared to $10.5 billion in 2009. The decrease of $2.9 billion

was primarily due to more stringent underwriting guidelines for home equity

lines of credit and loans as well as lower consumer demand.

At December 31, 2010, the consumer MSR balance was $14.9 billion,

which represented 92 bps of the related unpaid principal balance compared to

$19.5 billion, or 113 bps of the related unpaid principal balance at Decem-

ber 31, 2009. The decrease in the consumer MSR balance was driven by the

impact of declining mortgage rates partially offset by the addition of new

MSRs recorded in connection with sales of loans. In addition, elevated

servicing costs, due to higher personnel expenses associated with default-

related servicing activities, reduced expected cash flows. These factors

together resulted in the 21 bps decrease in capitalized MSRs as a percentage

of loans serviced.

Bank of America 2010 47