Bank of America 2010 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

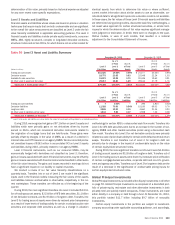

Determining whether an entity has a controlling financial interest in a VIE

requires significant judgment. An entity must assess the purpose and design

of the VIE, including explicit and implicit contractual arrangements, and the

entity’s involvement in both the design of the VIE and its ongoing activities.

The entity must then determine which activities have the most significant

impact on the economic performance of the VIE and whether the entity has

the power to direct such activities. For VIEs that hold financial assets, the

party that services the assets or makes investment management decisions

may have the power to direct the most significant activities of a VIE. Alter-

natively, a third party that has the unilateral right to replace the servicer or

investment manager or to liquidate the VIE may be deemed to be the party

with power. If there are no significant ongoing activities, the party that was

responsible for the design of the VIE may be deemed to have power. If the

entity determines that it has the power to direct the most significant activities

of the VIE, then the entity must determine if it has either an obligation to

absorb losses or the right to receive benefits that could potentially be

significant to the VIE. Such economic interests may include investments in

debt or equity instruments issued by the VIE, liquidity commitments, and

explicit and implicit guarantees.

On a quarterly basis, we reassess whether we have a controlling financial

interest and are the primary beneficiary of a VIE. The quarterly reassessment

process considers whether we have acquired or divested the power to direct

the activities of the VIE through changes in governing documents or other

circumstances. The reassessment also considers whether we have acquired

or disposed of a financial interest that could be significant to the VIE, or

whether an interest in the VIE has become significant or is no longer signif-

icant. The consolidation status of the VIEs with which we are involved may

change as a result of such reassessments. Changes in consolidation status

are applied prospectively, with assets and liabilities of a newly consolidated

VIE initially recorded at fair value. A gain or loss may be recognized upon

deconsolidation of a VIE depending on the carrying amounts of deconsoli-

dated assets and liabilities compared to the fair value of retained interests

and ongoing contractual arrangements.

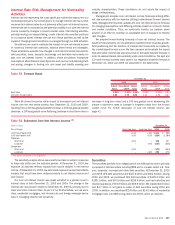

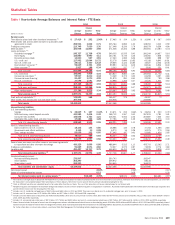

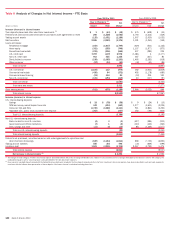

2009 Compared to 2008

The following discussion and analysis provides a comparison of our results of

operations for 2009 and 2008. This discussion should be read in conjunction

with the Consolidated Financial Statements and related Notes. Tables 6 and 7

contain financial data to supplement this discussion.

Overview

Net Income

Net income totaled $6.3 billion in 2009 compared to $4.0 billion in 2008.

Including preferred stock dividends, net loss applicable to common share-

holders was $2.2 billion, or $(0.29) per diluted share. Those results com-

pared with 2008 net income available to common shareholders of $2.6 billion,

or $0.54 per diluted share.

Net Interest Income

Net interest income on a FTE basis increased $1.9 billion to $48.4 billion for

2009 compared to 2008. The increase was driven by the improved rate

environment, the acquisitions of Countrywide and Merrill Lynch, the impact of

new draws on previously securitized accounts and the contribution from

market-based net interest income which benefited from the Merrill Lynch

acquisition. These items were partially offset by the impact of deleveraging

the ALM portfolio earlier in 2009, lower consumer loan levels and the adverse

impact of nonperforming loans. The net interest yield on a FTE basis de-

creased 33 bps to 2.65 percent for 2009 compared to 2008 due to the

factors related to the core businesses as described above.

Noninterest Income

Noninterest income increased $45.1 billion to $72.5 billion in 2009 com-

pared to 2008. Card income on a held basis decreased $5.0 billion primarily

due to higher credit losses on securitized credit card loans and lower fee

income driven by changes in consumer retail purchase and payment behavior

in the stressed economic environment. Investment and brokerage services

increased $6.9 billion primarily due to the acquisition of Merrill Lynch partially

offset by the impact of lower valuations in the equity markets driven by the

market downturn in late 2008, which improved modestly in 2009, and net

outflows in the cash funds. Investment banking income increased $3.3 billion

due to higher debt, equity and advisory fees reflecting the increased size of

the investment banking platform from the acquisition of Merrill Lynch. Equity

investment income increased $9.5 billion driven by $7.3 billion in gains on

sales of portions of our CCB investment and a $1.1 billion gain related to our

BlackRock investment. Trading account profits (losses) increased $18.1 bil-

lion primarily driven by favorable core trading results and reduced write-downs

on legacy assets partially offset by negative credit valuation adjustments on

derivative liabilities of $662 million due to improvement in the Corporation’s

credit spreads. Mortgage banking income increased $4.7 billion driven by

higher production and servicing income of $3.2 billion and $1.5 billion. These

increases were primarily due to increased volume as a result of the full-year

impact of Countrywide and higher refinance activity partially offset by lower

MSR results, net of hedges. Gains on sales of debt securities increased

$3.6 billion due to the favorable interest rate environment and improved credit

spreads. Gains were primarily driven by sales of agency MBS and CMOs. The

net loss in other decreased $1.6 billion primarily due to the $3.8 billion gain

from the contribution of our merchant processing business to a joint venture,

reduced support provided to cash funds and lower write-downs on legacy

assets offset by negative credit valuation adjustments recorded on Merrill

Lynch structured notes of $4.9 billion.

Provision for Credit Losses

The provision for credit losses increased $21.7 billion to $48.6 billion for

2009 compared to 2008 reflecting further deterioration in the economy and

housing markets across a broad range of property types, industries and

borrowers. Net charge-offs totaled $33.7 billion, or 3.58 percent of average

loans and leases for 2009 compared with $16.2 billion, or 1.79 percent for

2008. The increased level of net charge-offs is a result of the same factors

noted above.

Noninterest Expense

Noninterest expense increased $25.2 billion to $66.7 billion for 2009 com-

pared to 2008. Personnel costs and other general operating expenses rose

due to the addition of Merrill Lynch and the full-year impact of Countrywide.

Additionally, noninterest expense increased due to higher litigation costs

compared to the prior year, a $425 million pre-tax charge to pay the U.S. gov-

ernment to terminate its asset guarantee term sheet and higher FDIC insur-

ance costs including a $724 million special assessment in 2009.

Income Tax Expense

Income tax benefit was $1.9 billion for 2009 compared to expense of

$420 million for 2008 and resulted in an effective tax rate of (44.0) percent

compared to 9.5 percent in the prior year. The change in the effective tax rate

from the prior year was due to increased permanent tax preference items as

well as a shift in the geographic mix of our earnings driven by the addition of

Merrill Lynch.

Bank of America 2010 117