Bank of America 2010 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

liquidity at the parent company and selected subsidiaries, including our bank

and broker/dealer subsidiaries; determining what amounts of excess liquidity

are appropriate for these entities based on analysis of debt maturities and

other potential cash outflows, including those that we may experience during

stressed market conditions; diversifying funding sources, considering our

asset profile and legal entity structure; and performing contingency planning.

Global Excess Liquidity Sources and Other Unencumbered

Assets

We maintain excess liquidity available to the parent company and selected

subsidiaries in the form of cash and high-quality, liquid, unencumbered secu-

rities. These assets serve as our primary means of liquidity risk mitigation and

we call these assets our “Global Excess Liquidity Sources.” Our cash is primarily

on deposit with central banks, such as the Federal Reserve. We limit the

composition of high-quality, liquid, unencumbered securities to U.S. government

securities, U.S. agency securities, U.S. agency MBS and a select group of

non-U.S. government securities. We believe we can quickly obtain cash for these

securities, even in stressed market conditions, through repurchase agreements

or outright sales. We hold our Global Excess Liquidity Sources in entities that

allow us to meet the liquidity requirements of our global businesses and we

consider the impact of potential regulatory, tax, legal and other restrictions that

could limit the transferability of funds among entities.

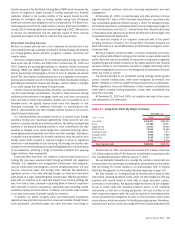

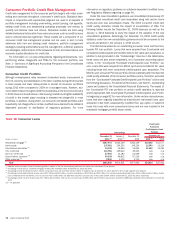

Our global excess liquidity sources increased $122 billion to $336 billion

at December 31, 2010 compared to $214 billion at December 31, 2009 and

were maintained as presented in the table below. This increase was due

primarily to liquidity generated by our bank subsidiaries through deposit

growth, loan repayments combined with lower loan demand and other factors.

Table 16 Global Excess Liquidity Sources

(Dollars in billions)

2010 2009

December 31

Parent company

$121

$99

Bank subsidiaries

180

89

Broker/dealers

35

26

Total global excess liquidity sources

$336

$214

As noted above, the excess liquidity available to the parent company is

held in cash and high-quality, liquid, unencumbered securities and totaled

$121 billion and $99 billion at December 31, 2010 and 2009. Typically,

parent company cash is deposited overnight with Bank of America, N.A.

Our bank subsidiaries’ excess liquidity sources at December 31, 2010

and 2009 were $180 billion and $89 billion. These amounts are distinct from

the cash deposited by the parent company, as described above. In addition to

their excess liquidity sources, our bank subsidiaries hold significant amounts

of other unencumbered securities that we believe could also be used to

generate liquidity, such as investment-grade ABS, MBS and municipal bonds.

Another way our bank subsidiaries can generate incremental liquidity is by

pledging a range of other unencumbered loans and securities to certain

Federal Home Loan Banks and the Federal Reserve Discount Window. The

cash we could have obtained by borrowing against this pool of specifically

identified eligible assets was approximately $170 billion and $187 billion at

December 31, 2010 and 2009. We have established operational procedures

to enable us to borrow against these assets, including regularly monitoring our

total pool of eligible loans and securities collateral. Due to regulatory restric-

tions, liquidity generated by the bank subsidiaries can only be used to fund

obligations within the bank subsidiaries and cannot be transferred to the

parent company or nonbank subsidiaries.

Our broker/dealer subsidiaries’ excess liquidity sources at December 31,

2010 and 2009 consisted of $35 billion and $26 billion in cash and high-

quality, liquid, unencumbered securities. Our broker/dealers also held

significant amounts of other unencumbered securities we believe could also

be used to generate additional liquidity, including investment-grade corporate

securities and equities. Liquidity held in a broker/dealer subsidiar y is only

available to meet the obligations of that entity and cannot be transferred to

the parent company or to any other subsidiary, often due to regulatory

restrictions and minimum requirements.

Time to Required Funding and Stress Modeling

We use a variety of metrics to determine the appropriate amounts of excess

liquidity to maintain at the parent company and our bank and broker/dealer

subsidiaries. One metric we use to evaluate the appropriate level of excess

liquidity at the parent company is “Time to Required Funding.” This debt

coverage measure indicates the number of months that the parent company

can continue to meet its unsecured contractual obligations as they come due

using only its Global Excess Liquidity Sources without issuing any new debt or

accessing any additional liquidity sources. We define unsecured contractual

obligations for purposes of this metric as maturities of senior or subordinated

debt issued or guaranteed by Bank of America Corporation or Merrill Lynch &

Co., Inc., including certain unsecured debt instruments, primarily structured

notes, which we may be required to settle for cash prior to maturity. The

ALMRC has established a target for Time to Required Funding of 21 months.

Time to Required Funding was 24 months at December 31, 2010 compared to

25 months at December 31, 2009.

We utilize liquidity stress models to assist us in determining the appro-

priate amounts of excess liquidity to maintain at the parent company and our

bank and broker/dealer subsidiaries. These risk sensitive models have be-

come increasingly important in analyzing our potential contractual and con-

tingent cash outflows beyond those outflows considered in the Time to

Required Funding analysis.

We evaluate the liquidity requirements under a range of scenarios with

varying levels of severity and time horizons. These scenarios incorporate

market-wide and Corporation-specific events, including potential credit ratings

downgrades for the parent company and our subsidiaries. We consider and

utilize scenarios based on historical experience, regulatory guidance, and

both expected and unexpected future events.

The types of contractual and contingent cash outflows we consider in our

scenarios may include, but are not limited to: upcoming contractual maturities

of unsecured debt and reductions in new debt issuance; diminished access to

secured financing markets; potential deposit withdrawals and reduced roll-

over of maturing term deposits by customers; increased draws on loan

commitments and liquidity facilities; additional collateral that counterparties

could call if our credit ratings were downgraded; collateral, margin and sub-

sidiary capital requirements arising from losses; and potential liquidity re-

quired to maintain businesses and finance customer activities.

We consider all sources of funds that we could access during each stress

scenario and focus particularly on matching available sources with corre-

sponding liquidity requirements by legal entity. We also use the stress mod-

eling results to manage our asset-liability profile and establish limits and

guidelines on certain funding sources and businesses.

Basel III Liquidity Standards

In December 2010, the Basel Committee on Bank Supervision issued “In-

ternational framework for liquidity risk measurement, standards and moni-

toring,” which includes two measures of liquidity risk. These two minimum

liquidity measures were initially introduced in guidance in December 2009 and

are considered part of Basel III.

The first liquidity measure is the Liquidity Coverage Ratio (LCR) which

identifies the amount of unencumbered, high quality liquid assets a financial

institution holds that can be used to offset the net cash outflows the insti-

tution would encounter under an acute 30-day stress scenario. The second

72 Bank of America 2010