Bank of America 2010 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

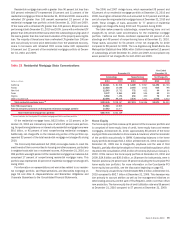

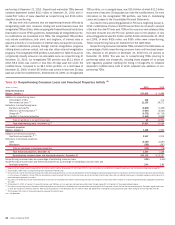

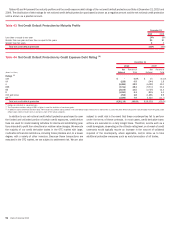

Table 37 presents commercial utilized reservable criticized exposure by

product type. Criticized exposure corresponds to the Special Mention, Sub-

standard and Doubtful asset categories as defined by regulatory authorities.

In addition to reservable loans and leases, excluding those accounted for

under the fair value option, exposure includes SBLCs, financial guarantees,

bankers’ acceptances and commercial letters of credit for which we are legally

bound to advance funds under prescribed conditions, during a specified time

period. Although funds have not been advanced, these exposure types are

considered utilized for credit risk management purposes. Total commercial

utilized reservable criticized exposure decreased $16.1 billion at Decem-

ber 31, 2010 compared to December 31, 2009, due to decreases across all

portfolios, primarily U.S. commercial and commercial real estate driven

largely by continued paydowns, payoffs and, to a diminishing extent,

charge-offs. Despite the improvements, utilized reservable criticized levels

remain elevated in commercial real estate. At December 31, 2010, approx-

imately 88 percent of the loans within commercial utilized reservable criticized

exposure were secured.

Table 37 Commercial Utilized Reservable Criticized Exposure

(Dollars in millions)

Amount Percent

(1)

Amount Percent

(1)

2010 2009

December 31

U.S. commercial

(2)

$17,195 7.44%

$28,259 11.77%

Commercial real estate

20,518 38.88

23,804 32.13

Commercial lease financing

1,188 5.41

2,229 10.04

Non-U.S. commercial

2,043 5.01

2,605 7.12

40,944 11.81

56,897 15.26

U.S. small business commercial

1,677 11.37

1,789 10.18

Total commercial utilized reservable criticized exposure

$42,621 11.80

$58,686 15.03

(1)

Percentages are calculated as commercial utilized reservable criticized exposure divided by total commercial utilized reservable exposure for each exposure category.

(2)

Excludes U.S. small business commercial exposure.

U.S. Commercial

At December 31, 2010, 57 percent and 25 percent of the U.S. commercial

loan portfolio, excluding small business, were included in Global Commercial

Banking and GBAM. The remaining 18 percent was mostly included in GWIM

(business-purpose loans for wealthy clients). Outstanding U.S. commercial

loans, excluding loans accounted for under the fair value option, decreased

$5.8 billion primarily due to reduced customer demand and continued client

utilization of the capital markets, partially offset by the adoption of new

consolidation guidance which increased loans by $5.3 billion on January 1,

2010. Compared to December 31, 2009, reservable criticized balances and

nonperforming loans and leases declined $11.1 billion and $1.5 billion. The

declines were broad-based in terms of borrowers and industries and were

driven by improved client credit profiles and liquidity. Net charge-offs de-

creased $1.3 billion in 2010 compared to 2009.

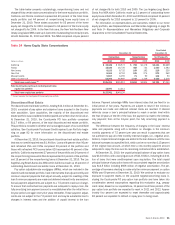

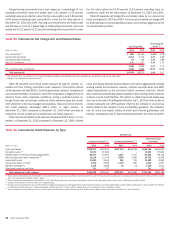

Commercial Real Estate

The commercial real estate portfolio is predominantly managed in Global

Commercial Banking and consists of loans made primarily to public and

private developers, homebuilders and commercial real estate firms. Out-

standing loans decreased $20.1 billion at December 31, 2010 compared

to December 31, 2009 due to portfolio attrition, the sale of First Republic,

transfer of certain assets to LHFS and net charge-offs. The portfolio remains

diversified across property types and geographic regions. California repre-

sents the largest state concentration at 18 percent of commercial real estate

loans and leases at December 31, 2010. For more information on geographic

and property concentrations, refer to Table 38.

Credit quality for commercial real estate is showing signs of stabilization;

however, we expect that elevated unemployment and ongoing pressure on

vacancy and rental rates will continue to affect primarily the non-homebuilder

portfolio. Compared to December 31, 2009, nonperforming commercial real

estate loans and foreclosed properties decreased in the homebuilder, retail

and land development property types, partially offset by an increase in office

and multi-use property types. Reservable criticized balances declined by

$3.3 billion primarily due to stabilization in the homebuilder portfolio and

retail and unsecured segments in the non-homebuilder portfolio, partially

offset by continued deterioration in the multi-family rental and office property

types within the non-homebuilder portfolio. Net charge-offs decreased

$685 million in 2010 compared to 2009 due to declines in the homebuilder

portfolio resulting from a slower rate of declining appraisal values.

Bank of America 2010 89