Bank of America 2010 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

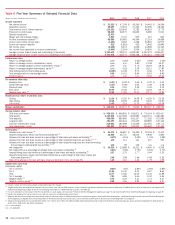

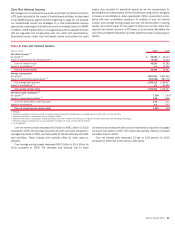

|

|

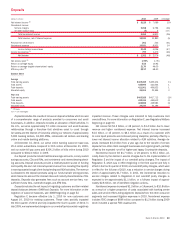

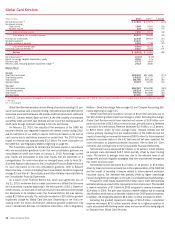

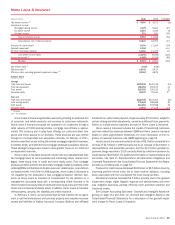

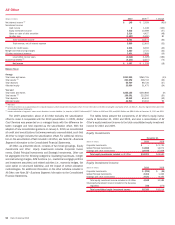

Mortgage Banking Income

Home Loans & Insurance mortgage banking income is categorized into

production and servicing income. Production income is comprised of revenue

from the fair value gains and losses recognized on our interest rate lock

commitments (IRLCs) and loans held-for-sale (LHFS), the related secondary

market execution, and costs related to representations and warranties in the

sales transactions along with other obligations incurred in the sales of

mortgage loans. In addition, production income includes revenue, which is

eliminated in All Other, for transfers of mortgage loans from Home Loans &

Insurance to the ALM portfolio related to the Corporation’s mortgage pro-

duction retention decisions.

Servicing income includes income earned in connection with servicing

activities and MSR valuation adjustments, net of economic hedge activities.

The costs associated with our servicing activities are included in noninterest

expense.

Servicing activities include collecting cash for principal, interest and

escrow payments from borrowers, disbursing customer draws for lines of

credit and accounting for and remitting principal and interest payments to

investors and escrow payments to third parties. Our home retention efforts

are also part of our servicing activities, along with responding to customer

inquiries and supervising foreclosures and property dispositions. In an effort

to avoid foreclosure, Bank of America evaluates various workout options prior

to foreclosure sale which has resulted in elongated default timelines. Our

servicing agreements with certain loan investors require us to comply with

usual and customar y standards in the liquidation of delinquent mortgage

loans. Our agreements with the GSEs provide timelines to complete the

liquidation of delinquent loans. In instances where we fail to meet these

timelines, our agreements provide the GSEs with the option to assess

compensatory fees. In 2010, the Corporation recorded an expense of ap-

proximately $230 million for estimated compensatory fees that it expects to

be assessed by the GSEs as a result of foreclosure delays. Additionally, we

may face demands and claims from private-label securitization investors

concerning alleged breaches of customary servicing standards. For additional

information on our servicing activities, see Recent Events – Certain Servicing-

related Issues beginning on page 38.

On October 18, 2010, Countrywide Home Loans Servicing, LP (which

changed its name to BAC Home Loans Servicing, LP), a wholly-owned sub-

sidiary of the Corporation, received a letter, in its capacity as servicer under

certain pooling and servicing agreements for 115 private-label residential

MBS securitizations (subsequently increased to 225 securitizations). The

letter asserted breaches of certain servicing obligations. For additional

information, see Recent Events – Private-label Residential Mortgage-backed

Securities Matters on page 39.

The table below summarizes the components of mortgage banking

income.

Mortgage Banking Income

(Dollars in millions)

2010 2009

Production income:

Core production revenue

$6,098

$7,352

Representations and warranties provision

(6,786)

(1,851)

Total production income (loss)

(688)

5,501

Servicing income:

Servicing fees

6,475

6,219

Impact of customer payments

(1)

(3,760)

(4,491)

Fair value changes of MSRs, net of economic hedge

results

(2)

376

1,539

Other servicing-related revenue

676

553

Total net servicing income

3,767

3,820

Total Home Loans & Insurance mortgage banking

income

3,079

9,321

Other business segments’ mortgage banking loss

(3)

(345)

(530)

Total consolidated mortgage banking income

$2,734

$8,791

(1)

Represents the change in the market value of the MSR asset due to the impact of customer payments received

during the year.

(2)

Includes sale of MSRs.

(3)

Includes the effect of transfers of mortgage loans from Home Loans & Insurance to the ALM portfolio in All

Other.

The production loss of $688 million represented a decrease of $6.2 billion

as representations and warranties provision increased $4.9 billion to

$6.8 billion which includes provision of $3.0 billion related to the GSE

agreements as well as adjustments to the representations and warranties

liability for other loans sold directly to the GSEs and not covered by those

agreements. Also contributing to the representations and warranties provi-

sion for the year was our continued evaluation of non-GSE exposure to

repurchases and similar claims, which led to the determination that we have

developed sufficient repurchase experience with certain non-GSE counter-

parties to record a liability related to existing and future projected claims from

such counterparties. For additional information on representations and war-

ranties, see Note 9 – Representations and Warranties Obligations and Cor-

porate Guarantees to the Consolidated Financial Statements, Recent

Events – Representations and Warranties Liability on page 37 and Represen-

tations and Warranties beginning on page 56. In addition, core production

revenue, which excludes representations and warranties provision, declined

$1.3 billion due to a decline in volume driven by a drop in the overall size of the

mortgage market and a decline in market share.

Net servicing income remained relatively flat as lower MSR results, net of

hedges, were offset by a lower impact of customer payments and higher fee

income. For additional information on MSRs and the related hedge instru-

ments, see Mortgage Banking Risk Management on page 110.

46 Bank of America 2010