Bank of America 2010 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

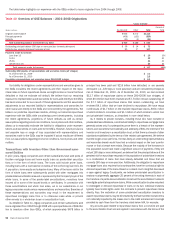

The table below highlights our experience with the GSEs related to loans originated from 2004 through 2008.

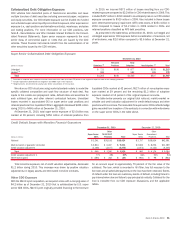

Table 10 Overview of GSE Balances – 2004–2008 Originations

(Dollars in billions)

Countrywide Other Total

Percent of

Total

Legacy Orginator

Original funded balance $846 $272

$1,118

Principal payments (406) (133)

(539)

Defaults (31) (3)

(34)

Total outstanding balance at December 31, 2010 $ 409 $ 136 $ 545

Outstanding principal balance 180 days or more past due (severely delinquent) $ 59 $ 14

$73

Defaults plus severely delinquent (principal at risk) 90 17

107

Payments made by borrower:

Less than 13

$16

15%

13-24

32

30

25-36

33

31

Greater than 36

26

24

Total payments made by borrower $ 107 100%

Outstanding GSE pipeline of representations and warranties claims (all vintages)

As of December 31, 2009

$3.3

As of December 31, 2010

2.8

Cumulative representations and warranties losses 2004-2008 vintages

$6.3

Our liability for obligations under representations and warranties given to

the GSEs considers the recent agreements and their impact on the repur-

chase rates on future repurchase claims we might receive on loans that have

defaulted or that we estimate will default. We believe that our remaining

exposure to representations and warranties for loans sold directly to the GSEs

has been accounted for as a result of these agreements and the associated

adjustments to our recorded liability for representations and warranties for

other loans sold directly to the GSEs and not covered by the agreements. We

believe our predictive repurchase models, utilizing our historical repurchase

experience with the GSEs while considering current developments, including

the recent agreements, projections of future defaults as well as certain

assumptions regarding economic conditions, home prices and other matters,

allows us to reasonably estimate the liability for obligations under represen-

tations and warranties on loans sold to the GSEs. However, future provisions

and possible loss or range of loss associated with representations and

warranties made to the GSEs may be impacted if actual results are different

from our assumptions regarding economic conditions, home prices and other

matters.

Transactions with Investors Other than Government-spon-

sored Entities

In prior years, legacy companies and certain subsidiaries have sold pools of

first-lien mortgage loans and home equity loans as private-label securitiza-

tions or in the form of whole loans. The loans sold include prime loans,

including loans with a loan balance in excess of the conforming loan limit, Alt-

A, pay-option, home equity and subprime loans. Many of the loans sold in the

form of whole loans were subsequently pooled with other mortgages into

private-label securitizations issued or sponsored by the third-party buyer of the

whole loans. In some of the private-label securitizations, monolines have

insured all or some of the issued bonds or certificates. In connection with

these securitizations and whole loan sales, we or our subsidiaries or our

legacy companies made various representations and warranties. Breaches of

these representations and warranties may result in the requirement to

repurchase mortgage loans from or to otherwise make whole or provide

other remedy to a whole-loan buyer or securitization trust.

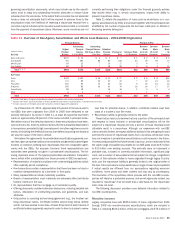

As detailed in Table 11, legacy companies and certain subsidiaries sold

loans originated from 2004 through 2008 with a principal balance of $963 bil-

lion to investors other than GSEs, of which approximately $478 billion in

principal has been paid and $216 billion have defaulted, or are severely

delinquent (i.e., 180 days or more past due) and are considered principal at-

risk at December 31, 2010. As of December 31, 2010, we had received

$13.7 billion of repurchase claims on these 2004-2008 loan vintages, of

which $6.0 billion have been resolved and $7.7 billion remain outstanding. Of

the $7.7 billion of repurchase claims that remain outstanding, we have

reviewed $4.1 billion that we have declined to repurchase. We have recog-

nized losses of $1.7 billion on the resolved repurchase claims, $631 million

of which relates to monolines and $1.1 billion of which relates to whole loan

and private-label investors, as described in more detail below.

As it relates to private investors, including those who have invested in

private-label securitizations, a contractual liability to repurchase mortgage loans

generally arises only if counterparties prove there is a breach of the represen-

tations and warranties that materially and adversely affects the interest of the

investor or all investors in a securitization trust, or that there is a breach of other

standards established by the terms of the related sale agreement. We believe

that the longer a loan performs, the less likely an underwriting representations

and warranties breach would have had a material impact on the loan’s perfor-

mance or that a breach even exists. Because the majority of the borrowers in

this population would have made a significant amount of payments if they are

not yet 180 days or more delinquent, we believe that the principal balance at the

greatest risk for repurchase requests in this population of private-label investors

is a combination of loans that have already defaulted and those that are

currently 180 days or more past due. Additionally, the obligation to repurchase

mortgage loans also requires that counterparties have the contractual right to

demand repurchase of the loans. Based on a recent court ruling that dismissed

a case against legacy Countrywide, we believe private-label securitization in-

vestors must generally aggregate 25 percent of the voting interests in each of

the tranches of a particular securitization to instruct the securitization trustee to

investigate potential repurchase claims. While a securitization trustee may elect

to investigate or demand repurchase of loans on its own, individual investors

typically have limited rights under the contracts to present repurchase claims

directly. Also, the motivation of some private-label securitization investors to

assert repurchase claims may be diminished by the fact that their investment is

not materially impacted by the losses due to the credit enhancement coverage

provided by cash flows from the tranches rated below AAA, for example.

Any amounts paid related to repurchase claims from a monoline are paid

to the securitization trust and are applied in accordance with the terms of the

58 Bank of America 2010