Bank of America 2010 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

on the consolidated liabilities, subject to certain exclusions and offsets, of U.K.

group companies and U.K. branches of foreign banking groups as of each year-

end balance sheet date. As currently proposed, the bank levy rate for 2011 and

future years will be 0.075 percent per annum for certain short-term liabilities

with a rate of 0.0375 percent per annum for longer maturity liabilities and

certain deposits. The legislation is expected to be enacted in the third quarter

of 2011. We currently estimate that the cost of the U.K. bank levy will be

approximately $125 million annually beginning in 2011.

Regulatory Guidance on Collateral Dependent Loans

On February 23, 2010, regulators issued clarifying guidance, effective in the

first quarter of 2010, on modified consumer real estate loans that specifies

criteria required to demonstrate a borrower’s capacity to repay the modified

loan. In connection with this guidance, we reviewed our modified consumer

real estate loans and determined that a portion of these loans did not meet

the criteria and, therefore, were deemed collateral dependent. The guidance

requires that a modified loan deemed to be collateral dependent be written

down to its estimated collateral value even if that loan is performing. The

application of this guidance resulted in $1.0 billion of net charge-offs in 2010,

of which $822 million were home equity, $207 million were residential

mortgage and $9 million were discontinued real estate.

Making Home Affordable Program

On March 4, 2009, the U.S. Treasury provided details related to the $75 billion

Making Home Affordable program (MHA) which is focused on reducing the

number of foreclosures and making it easier for customers to refinance loans.

The MHA consists of the Home Affordable Modification Program (HAMP) which

provides guidelines on first-lien loan modifications, and the Home Affordable

Refinance Program (HARP) which provides guidelines for loan refinancing.

As part of the MHA program, on April 28, 2009, the U.S. government

announced intentions to create the second-lien modification program (2MP)

that is designed to reduce the monthly payments on qualifying home equity

loans and lines of credit under certain conditions, including completion of a

HAMP modification on the first mortgage on the property. This program

provides incentives to lenders to modify all eligible loans that fall under

the guidelines of this program. Additional clarification on government guide-

lines for the program was announced early in 2010. On April 8, 2010, we

began early implementation of the 2MP with the mailing of trial modification

offers to eligible home equity customers. We will modify eligible second liens

under this initiative regardless of whether the MHA modified “first lien” is

serviced by the Corporation or another participating servicer.

On April 5, 2010, we implemented the Home Affordable Foreclosure

Alternatives (HAFA) program, which is another addition to the HAMP that

assists borrowers with non-retention options, such as short sale or dee-

d-in-lieu options, instead of foreclosure. The HAFA program provides incen-

tives to lenders to assist all eligible borrowers that fall under the guidelines of

this program. Our first goal is to work with the borrower to determine if a loan

modification or other homeownership retention solution is available before

pursuing non-retention options such as short sales. Short sales are an

important option for homeowners who are facing financial difficulty and do

not have a viable option to remain in the home. HAFA’s short sale guidelines

are designed to streamline and standardize the process and will be compat-

ible with Bank of America’s new cooperative short sale program.

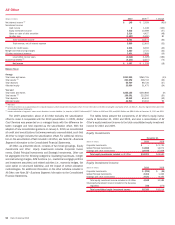

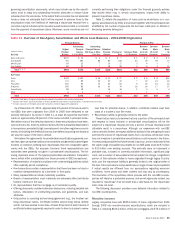

During 2010, 285,000 loan modifications were completed with a total

unpaid principal balance of $65.7 billion, including 109,000 loans with a total

unpaid principal amount of $25.5 billion that were converted from trial-period to

permanent modifications under the MHA, which include HAMP first-lien mod-

ifications and 2MP second-lien modifications. In addition, on March 26, 2010,

the U.S. government announced new changes to the MHA program guidelines

that include principal forgiveness options to the HAMP for a sub-segment of

qualified HAMP borrowers. The details around eligibility, forgiveness arrange-

ments and the incentive structures are still being finalized. However, we

implemented a forgiveness program on a subset of HAMP eligible products

under the National Home Retention Program (NHRP) in 2010.

In addition to the programs described above, we have implemented

several programs designed to help our customers. For information on these

programs, refer to Credit Risk Management beginning on page 75. We will

continue to help our customers address financial challenges through these

government programs and our own home retention programs.

Stress Tests

The Corporation has established management routines to periodically con-

duct stress tests to evaluate potential impacts to the Corporation under

hypothetical economic scenarios. These stress tests will facilitate our con-

tingency planning and management of capital and liquidity. These processes

were also used to conduct the recent secondary stress testing imposed by the

Federal Reserve and were incorporated into the Capital Plan that was sub-

mitted as part of this request, which included a proposed modest increase in

our common dividend in the second half of 2011. The results of these stress

tests may influence bank regulatory supervisory requirements concerning the

Corporation and may impact the amount or timing of dividends or distributions

to the Corporation’s stockholders. For additional information, see Capital

Management beginning on page 67 and Liquidity Risk beginning on page 71.

Other Matters

The Corporation has established guidelines and policies for managing capital

across its subsidiaries. The guidance for the Corporation’s subsidiaries with

regulatory capital requirements, including branch operations of banking sub-

sidiaries, requires each entity to maintain satisfactory capital levels. This

includes setting internal capital targets for the U.S. bank subsidiaries to

exceed “well capitalized” levels.

The U.K. has adopted increased capital and liquidity requirements for local

financial institutions, including regulated U.K. subsidiaries of non-U.K. bank

holding companies and other financial institutions as well as branches of non-

U.K. banks located in the U.K. In addition, the U.K. has proposed the creation

and production of recovery and resolution plans (commonly referred to as

living wills) by such entities. We are currently monitoring the impact of these

initiatives.

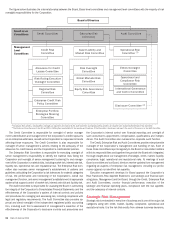

Managing Risk

Overview

Risk is inherent in every activity that we undertake. Our business exposes us

to strategic, credit, market, liquidity, compliance, operational and reputational

risk. We must manage these risks to maximize our long-term results by

ensuring the integrity of our assets and the quality of our earnings.

Strategic risk is the risk that results from adverse business decisions,

ineffective or inappropriate business plans, or failure to respond to changes

in the competitive environment, business cycles, customer preferences,

product obsolescence, regulatory environment, business strategy execution,

and/or other inherent risks of the business including reputational risk. Credit

risk is the risk of loss arising from a borrower’s or counterparty’s inability to

meet its obligations. Market risk is the risk that values of assets and liabilities

or revenues will be adversely affected by changes in market conditions such

as interest rate movements. Liquidity risk is the inability to meet contractual

and contingent financial obligations, on- or off-balance sheet, as they come

due. Compliance risk is the risk that arises from the failure to adhere to laws,

rules, regulations, or internal policies and procedures. Operational risk is the

risk of loss resulting from inadequate or failed internal processes, people and

systems, or external events. Reputational risk is the potential that negative

Bank of America 2010 63