Bank of America 2010 Annual Report Download - page 190

Download and view the complete annual report

Please find page 190 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

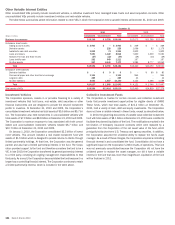

the liability for representations and warranties is a function of the represen-

tations and warranties given and considers a variety of factors, which include,

depending on the counterparty, actual defaults, estimated future defaults,

historical loss experience, estimated home prices, probability that a repur-

chase request will be received, number of payments made by the borrower

prior to default and probability that a loan will be required to be repurchased.

Historical experience also considers recent events such as the agreements

with the GSEs on December 31, 2010, as discussed below. Changes to any

one of these factors could significantly impact the estimate of the

Corporation’s liability.

Although the timing and volume has varied, repurchase and similar re-

quests have increased in recent periods from buyers and insurers, including

monolines. The Corporation expects that efforts to attempt to assert repur-

chase requests by monolines, whole-loan investors and private-label securi-

tization investors may increase in the future. A loan-by-loan review of all

properly presented repurchase requests is performed and demands have

been and will continue to be contested to the extent not considered valid. In

addition, the Corporation may reach a bulk settlement with a counterparty (in

lieu of the loan-by-loan review process), on terms determined to be advanta-

geous to the Corporation.

On December 31, 2010, the Corporation reached agreements with the

GSEs under which the Corporation paid $2.8 billion to resolve repurchase

claims involving certain residential mortgage loans sold directly to the GSEs

by entities related to legacy Countrywide. The agreements with FHLMC for

$1.28 billion extinguishes all outstanding and potential mortgage repurchase

and make-whole claims arising out of any alleged breaches of selling repre-

sentations and warranties related to loans sold directly by legacy Countrywide

to FHLMC through 2008, subject to certain exceptions the Corporation does

not believe to be material. The agreement with FNMA for $1.52 billion sub-

stantially resolves the existing pipeline of repurchase and make-whole claims

outstanding as of September 20, 2010 arising out of alleged breaches of

selling representations and warranties related to loans sold directly by legacy

Countrywide to FNMA. These agreements with the GSEs do not cover legacy

Bank of America first-lien residential mortgage loans sold directly to the GSEs,

other loans sold to the GSEs other than described above, loan servicing

obligations, other contractual obligations or loans contained in private-label

securitizations.

Overall, repurchase requests and disputes with buyers and insurers

regarding representations and warranties have increased in recent periods

which has resulted in an increase in unresolved repurchase requests for

monolines and other non-GSE counterparties. Generally the volume of unre-

solved repurchase requests from the FHA and VA for loans in GNMA-guaran-

teed securities is not significant because the requests are limited in number

and are typically resolved quickly. The volume of repurchase claims as a

percentage of the volume of loans purchased arising from loans sourced from

brokers or purchased from third-party sellers is relatively consistent with the

volume of repurchase claims as a percentage of the volume of loans origi-

nated by the Corporation or its subsidiaries or legacy companies.

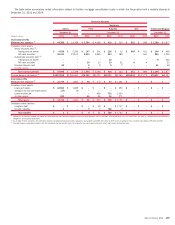

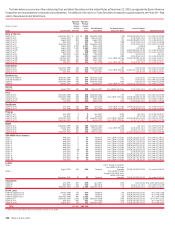

The table below presents outstanding claims by counterparty and product

type at December 31, 2010 and 2009. The information for 2010 reflects the

impact of the recent agreements with the GSEs.

Outstanding Claims by Counterparty and Product

(Dollars in millions)

2010 2009

December 31

By counterparty

GSEs

$2,821

$3,284

Monolines

4,799

2,944

Whole loan and private-label securitization investors and

other

(1)

3,067

1,372

Total outstanding claims by counterparty

$10,687

$7,600

By product type

Prime loans

$2,040

$1,778

Alt-A

1,190

1,629

Home equity

3,658

2,223

Pay option

2,889

1,122

Subprime

734

540

Other

176

308

Total outstanding claims by product type

$10,687

$7,600

(1)

December 31, 2010 includes $1.7 billion in claims contained in correspondence from private-label securitiza-

tions investors that do not have the right todemand repurchase of loans directly or the right to access loan files.

The inclusion of these claims in the amounts noted does not mean that the Corporation believes these claims

have satisfied the contractual thresholds to direct the securitization trustee to take action or are otherwise

procedurally or substantively valid.

As presented in the table on page 189, during 2010 and 2009, the

Corporation paid $5.2 billion and $2.6 billion to resolve $6.6 billion and

$3.0 billion of repurchase claims through repurchase or reimbursement to the

investor or securitization trust for losses they incurred, resulting in a loss on

the related loans at the time of repurchase or reimbursement of $3.5 billion

and $1.6 billion. The amount of loss for loan repurchases is reduced by the

fair value of the underlying loan collateral. The repurchase of loans and

indemnification payments related to first-lien and home equity repurchase

claims generally resulted from material breaches of representations and

warranties related to the loans’ material compliance with the applicable

underwriting standards, including borrower misrepresentation, credit excep-

tions without sufficient compensating factors and non-compliance with un-

derwriting procedures, although the actual representations made in a sales

transaction and the resulting repurchase and indemnification activity can vary

by transaction or investor. A direct relationship between the type of defect that

causes the breach of representations and warranties and the severity of the

realized loss has not been observed. Transactions to repurchase or indem-

nification payments related to first-lien residential mortgages primarily in-

volved the GSEs while transactions to repurchase or indemnification pay-

ments for home equity loans primarily involved the monolines.

188 Bank of America 2010