Bank of America 2010 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

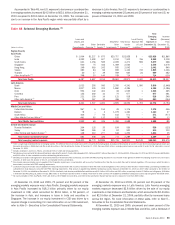

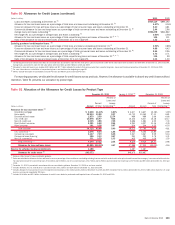

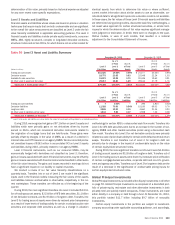

The table below includes derivatives utilized in our ALM activities including

those designated as accounting and economic hedging instruments. The fair

value of net ALM contracts increased $329 million to a gain of $12.6 billion at

December 31, 2010 compared to $12.3 billion at December 31, 2009. The

increase was primarily attributable to changes in the value of U.S. dollar-

denominated receive-fixed interest rate swaps of $3.3 billion, foreign ex-

change contracts of $2.1 billion and foreign exchange basis swaps of

$197 million. The increase was partially offset by a loss from the changes

in the value of pay-fixed interest rate swaps of $5.0 billion and option products

of $294 million.

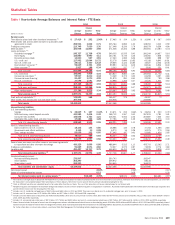

Table 55 Asset and Liability Management Interest Rate and Foreign Exchange Contracts

(Dollars in millions, average estimated duration in years)

Fair

Value Total 2011 2012 2013 2014 2015 Thereafter

Average

Estimated

Duration

Expected Maturity

December 31, 2010

Receive fixed interest rate swaps

(1, 2)

$7,364 4.45

Notional amount

$104,949 $ 8 $36,201 $ 7,909 $ 7,270 $ 8,094 $45,467

Weighted-average fixed-rate

3.94% 1.00% 2.49% 3.90% 3.66% 3.71% 5.19%

Pay fixed interest rate swaps

(1, 2)

(3,827) 6.03

Notional amount

$156,067 $50,810 $16,205 $ 1,207 $ 4,712 $10,933 $72,200

Weighted-average fixed-rate

3.02% 2.37% 2.15% 2.88% 2.40% 2.75% 3.76%

Same-currency basis swaps

(3)

103

Notional amount

$152,849 $13,449 $49,509 $31,503 $21,085 $11,431 $25,872

Foreign exchange basis swaps

(2, 4, 5)

4,830

Notional amount

235,164 21,936 39,365 46,380 41,003 23,430 63,050

Option products

(6)

(120)

Notional amount

(8)

6,572 (1,180) 2,092 2,390 603 311 2,356

Foreign exchange contracts

(2, 5, 7)

4,272

Notional amount

(8)

109,544 59,508 5,427 10,048 13,035 2,372 19,154

Futures and forward rate contracts

(21)

Notional amount

(8)

(280)(280)–––– –

Net ALM contracts $12,601

(Dollars in millions, average estimated duration in years)

Fair

Value Total 2010 2011 2012 2013 2014 Thereafter

Average

Estimated

Duration

Expected Maturity

December 31, 2009

Receive fixed interest rate swaps

(1, 2)

$4,047 4.34

Notional amount $110,597 $15,212 $ 8 $35,454 $ 7,333 $ 8,247 $44,343

Weighted-average fixed-rate 3.65% 1.61% 1.00% 2.42% 4.06% 3.48% 5.29%

Pay fixed interest rate swaps

(1, 2)

1,175 4.18

Notional amount $104,445 $ 2,500 $50,810 $14,688 $ 806 $ 3,729 $31,912

Weighted-average fixed-rate 2.83% 1.82% 2.37% 2.24% 3.77% 2.61% 3.92%

Same-currency basis swaps

(3)

107

Notional amount $ 42,881 $ 4,549 $ 8,593 $11,934 $ 5,591 $ 5,546 $ 6,668

Foreign exchange basis swaps

(2, 4, 5)

4,633

Notional amount 122,807 7,958 10,968 19,862 18,322 31,853 33,844

Option products

(6)

174

Notional amount

(8)

6,540 656 2,031 1,742 244 603 1,264

Foreign exchange contracts

(2, 5, 7)

2,144

Notional amount

(8)

103,726 63,158 3,491 3,977 6,795 10,585 15,720

Futures and forward rate contracts (8)

Notional amount

(8)

10,55910,559–––– –

Net ALM contracts

$12,272

(1)

At December 31, 2010 and 2009, the receive-fixed interest rate swap notional amounts that represented forward starting swaps and will not be effective until their respective contractual start dates were $1.7 billion and $2.5 billion,

and the forward starting pay-fixed swap positions were $34.5 billion and $76.8 billion.

(2)

Does not include basis adjustments on either fixed-rate debt issued by the Corporation or AFS debt securities which are hedged in fair value hedge relationships using derivatives designated as hedging instruments that substantially

offset the fair values of these derivatives.

(3)

At December 31, 2010 and 2009, same-currency basis swaps consist of $152.8 billion and $42.9 billion in both foreign currency and U.S. dollar-denominated basis swaps in which both sides of the swap are in the same currency.

(4)

Foreign exchange basis swaps consisted of cross-currency variable interest rate swaps used separately or in conjunction with receive-fixed interest rate swaps.

(5)

Does not include foreign currency translation adjustments on certain non-U.S. debt issued by the Corporation which substantially offset the fair values of these derivatives.

(6)

Option products of $6.6 billion at December 31, 2010 are comprised of $160 million in purchased caps/floors, $8.2 billion in swaptions and $(1.8) billion in foreign exchange options. Option products of $6.5 billion at December 31,

2009 are comprised of $177 million in purchased caps/floors and $6.3 billion in swaptions.

(7)

Foreign exchange contracts include foreign currency-denominated and cross-currency receive-fixed interest rate swaps as well as foreign currency forward rate contracts. Total notional amount was comprised of $57.6 billion in foreign

currency-denominated and cross-currency receive-fixed swaps and $52.0 billion in foreign currency forward rate contracts at December 31, 2010, and $46.0 billion in foreign currency-denominated and cross-currency receive-fixed

swaps and $57.7 billion in foreign currency forward rate contracts at December 31, 2009.

(8)

Reflects the net of long and short positions.

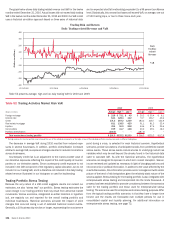

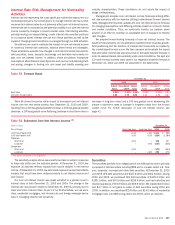

We use interest rate derivative instruments to hedge the variability in the

cash flows of our assets and liabilities, including certain compensation costs

and other forecasted transactions (collectively referred to as cash flow

hedges). The net losses on both open and terminated derivative instruments

recorded in accumulated OCI, net-of-tax, were $3.2 billion and $2.5 billion at

December 31, 2010 and 2009. These net losses are expected to be reclas-

sified into earnings in the same period as the hedged cash flows affect

earnings and will decrease income or increase expense on the respective

hedged cash flows. Assuming no change in open cash flow derivative hedge

positions and no changes to prices or interest rates beyond what is implied in

forward yield curves at December 31, 2010 the pre-tax net losses are

expected to be reclassified into earnings as follows: $1.8 billion, or 35 percent

within the next year, 80 percent within five years, and 92 percent within

10 years, with the remaining eight percent thereafter. For more information on

derivatives designated as cash flow hedges, see Note 4 – Derivatives to the

Consolidated Financial Statements.

Bank of America 2010 109