Bank of America 2010 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

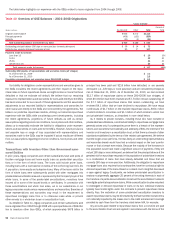

governing securitization documents, which may include use by the securiti-

zation trust to repay any outstanding monoline advances or reduce future

advances from the monolines. To the extent that a monoline has not advanced

funds or does not anticipate that it will be required to advance funds to the

securitization trust, the likelihood of receiving a repurchase request from a

monoline may be reduced as the monoline would receive limited or no benefit

from the payment of repurchase claims. Moreover, some monolines are not

currently performing their obligations under the financial guaranty policies

they issued which may, in certain circumstances, impact their ability to

present repurchase claims.

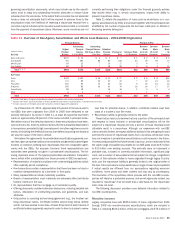

Table 11 details the population of loans sold as whole-loans or in non-

agency securitizations by entity and product together with the principal at-risk

stratified by the number of payments the borrower made prior to default or

becoming severely delinquent.

Table 11 Overview of Non-Agency Securitization and Whole Loan Balances – 2004-2008 Originations

(Dollars in billions)

By Entity

Original

Principal

Balance

Outstanding

Principal

Balance

12/31/2010

Outstanding

Principal Balance

180 Days or More

Past Due

Defaulted

Principal

Balance

Principal at

Risk

Borrower Made

G13 Payments

Borrower

Made

13 to 24

Payments

Borrower

Made

25 to 36

Payments

Borrower

Made

H36

Payments

Principal Balance Principal at Risk

Bank of America $ 100 $ 34 $ 4 $ 3 $ 7 $ 1 $ 2 $ 2 $ 2

Countrywide 716 293 86 80 166 24 46 49 47

Merrill Lynch 65 22 7 10 17 3 4 3 7

First Franklin 82 23 7 19 26 4 6 4 12

Total

(1, 2, 3)

$963 $372 $104 $112 $216 $32 $58 $58 $68

By Product

Prime $ 302 $ 124 $ 16 $ 11 $ 27 $ 2 $ 6 $ 8 $11

Alt-A 172 82 22 21 43 7 12 12 12

Pay option 150 65 30 20 50 5 15 16 14

Subprime 245 82 36 43 79 16 19 17 27

Home Equity 88 18 – 16 16 2 5 5 4

Other 6 1 – 1 1 – 1 – –

Total $963 $372 $104 $112 $216 $32 $58 $58 $68

(1)

Includes $186 billion of original principal balance related to transactions with monoline participation.

(2)

Excludes transactions sponsored by Bank of America and Merrill Lynch where no representations or warranties were assumed.

(3)

Includes exposures on third-party sponsored transactions related to legacy entity originations.

As of December 31, 2010, approximately 22 percent of the loans sold to

non-GSEs that were originated from 2004 to 2008 have defaulted or are

severely delinquent. As shown in Table 11, at least 25 payments have been

made on approximately 58 percent of the loans included in principal at-risk.

We believe many of the defaults observed in these securitizations have been,

and continue to be, driven by external factors like the substantial depreciation

in home prices, persistently high unemployment and other negative economic

trends, diminishing the likelihood that any loan defect (assuming one exists at

all) was the cause of the loan’s default.

We believe the agreements for private-label securitizations generally con-

tain less rigorous representations and warranties and generally impose higher

burdens on investors seeking loan repurchases than the comparable agree-

ments with the GSEs. For example, borrower fraud representations and

warranties were generally not given in private-label securitizations. The fol-

lowing represent some of the typical private-label securitization transaction

terms (which differ substantially from those provided in GSE transactions):

• Representation of material compliance with underwriting guidelines (which

often explicitly permit exceptions).

• Few transactions contain a representation that there has been no fraud or

material misrepresentation by a borrower or third party.

• Many representations include materiality qualifiers.

• Breach of representation must materially and adversely affect certificate

holders’ interest in the loan.

• No representation that the mortgage is of investment quality.

• Offering documents included extensive disclosures, including detailed risk

factors, description of underwriting practices and guidelines, and loan

attributes.

• Only parties to a pooling and servicing agreement (e.g., the trustee) can

bring repurchase claims. Certificate holders cannot bring claims directly

and do not have access to loan files. At least 25 percent of each tranche of

certificate holders is generally required in order to direct a trustee to review

loan files for potential claims. In addition, certificate holders must bear

costs of a trustee’s loan file review.

• Repurchase liability is generally limited to the seller.

These factors lead us to believe that only a portion of the principal at-risk

with respect to loans included in private-label securitizations will be the

subject of a repurchase request and only a portion of those requests would

ultimately result in a repurchase. Although our experience with non-GSE

claims remains limited, we expect additional activity in this area going forward

and that the volume of repurchase claims from monolines, whole-loan inves-

tors and investors in private-label securitizations could increase in the future.

It is reasonably possible that future losses may occur, and our estimate is that

the upper range of possible loss related to non-GSE sales could be $7 billion

to $10 billion over existing accruals. This estimate does not represent a

probable loss, is based on currently available information, significant judg-

ment, and a number of assumptions that are subject to change. A significant

portion of this estimate relates to loans originated through legacy Country-

wide, and the repurchase liability is generally limited to the original seller of

the loan. Future provisions and possible loss or range of loss may be impacted

if actual results are different from our assumptions regarding economic

conditions, home prices and other matters and may vary by counterparty.

The resolution of the repurchase claims process with the non-GSE counter-

parties will likely be a protracted process, and we will vigorously contest any

request for repurchase if we conclude that a valid basis for the repurchase

claim does not exist.

The following discussion provides more detailed information related to

non-GSE counterparties.

Monoline Insurers

Legacy companies have sold $185.6 billion of loans originated from 2004

through 2008 into monoline-insured securitizations, which are included in

Table 11, including $106.2 billion of first-lien mortgages and $79.4 billion of

Bank of America 2010 59