Bank of America 2010 Annual Report Download - page 216

Download and view the complete annual report

Please find page 216 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

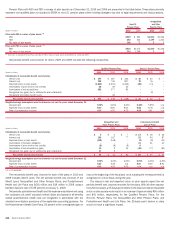

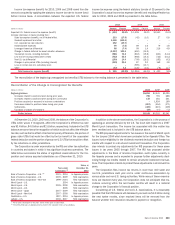

Regulatory Capital Developments

In June 2004, the Basel II Accord was published with the intent of more closely

aligning regulatory capital requirements with underlying risks, similar to

economic capital. While economic capital is measured to cover unexpected

losses, the Corporation also manages regulatory capital to adhere to regu-

latory standards of capital adequacy.

The Basel II Final Rule (Basel II Rules), which was published on Decem-

ber 7, 2007, established requirements for the U.S. implementation and

provided detailed requirements for a new regulatory capital framework related

to credit and operational risk (Pillar 1), supervisory requirements (Pillar 2) and

disclosure requirements (Pillar 3). The Corporation began Basel II parallel

implementation on April 1, 2010.

Subsequently, amended rules issued by the Basel Committee on Bank

Supervision known as Basel III were published in December 2010 along with

final Market Risk Rules issued by the Federal Reserve. The Basel III rules and

the Financial Reform Act seek to disqualify trust preferred securities and other

hybrid capital securities from Tier 1 capital treatment with the Financial

Reform Act proposing it to be phased in over a period from 2013 to 2015.

Basel III also proposes the deduction of certain assets from capital (deferred

tax assets, MSRs, investments in financial firms and pension assets, among

others, within prescribed limitations certain of which may be significant),

increased capital for counterparty credit risk, and three capital buffers to

strengthen capital levels which would be also phased in over time. The three

capital buffers include a capital conservation buffer, a countercyclical buffer

and a systematically important financial institution buffer, which would result

in a minimum Total capital ratio of at least eight percent by 2013. Market Risk

Rules include additional VaR based measurements, among others, that are

meant to further strengthen capital levels. The Corporation continues to

monitor the development and potential impact of these rules, and has

determined that given current initiatives and continued focus on all of these

rules by the date of full implementation in 2018, the Corporation must have a

Tier 1 common capital ratio of seven percent which it anticipates it will meet.

The Corporation does not expect the need to issue any common stock to meet

the new Basel proposals.

There remains significant uncertainty on the final impacts as the U.S. has

issued final rules only for Basel II and a Notice of Proposed Rulemaking for the

Market Risk Rules at this time. Impacts may change as the U.S. finalizes rules

for Basel III and the regulatory agencies interpret the final rules during the

implementation process.

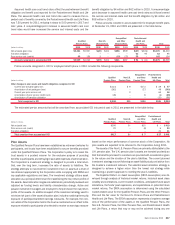

NOTE 19 Employee Benefit Plans

Pension and Postretirement Plans

The Corporation sponsors noncontributory trusteed pension plans that cover

substantially all officers and employees, a number of noncontributory non-

qualified pension plans, and postretirement health and life plans. The plans

provide defined benefits based on an employee’s compensation and years of

service. The Bank of America Pension Plan (the Pension Plan) provides

participants with compensation credits, generally based on years of service.

For account balances based on compensation credits prior to January 1,

2008, the Pension Plan allows participants to select from various earnings

measures, which are based on the returns of certain funds or common stock

of the Corporation. The participant-selected earnings measures determine

the earnings rate on the individual participant account balances in the Pen-

sion Plan. Participants may elect to modify earnings measure allocations on a

periodic basis subject to the provisions of the Pension Plan. For account

balances based on compensation credits subsequent to December 31,

2007, the account balance earnings rate is based on a benchmark rate.

For eligible employees in the Pension Plan on or after January 1, 2008, the

benefits become vested upon completion of three years of service. It is the

policy of the Corporation to fund not less than the minimum funding amount

required by ERISA.

The Pension Plan has a balance guarantee feature for account balances

with participant-selected earnings, applied at the time a benefit payment is

made from the plan that effectively provides principal protection for partic-

ipant balances transferred and certain compensation credits. The Corpora-

tion is responsible for funding any shortfall on the guarantee feature.

In May 2008, the Corporation and the IRS entered into a closing agree-

ment resolving all matters relating to an audit by the IRS of the Pension Plan

and the Bank of America 401(k) Plan. The audit included a review of voluntary

transfers by participants of 401(k) Plan accounts to the Pension Plan. In

connection with the agreement, during 2009 the Pension Plan transferred

approximately $1.2 billion of assets and liabilities associated with the trans-

ferred accounts to a newly established defined contribution plan.

As a result of acquisitions, the Corporation assumed the obligations

related to the pension plans of FleetBoston, MBNA, U.S. Trust Corporation,

LaSalle and Countrywide. These five acquired pension plans have been

merged into a separate defined benefit pension plan, which, together with

the Pension Plan, are referred to as the Qualified Pension Plans. The benefit

structures under these acquired plans have not changed and remain intact in

the merged plan. Certain benefit structures are substantially similar to the

Pension Plan discussed above; however, certain of these structures do not

allow participants to select various earnings measures; rather the earnings

rate is based on a benchmark rate. In addition, these benefit structures

include participants with benefits determined under formulas based on

average or career compensation and years of service rather than by reference

to a pension account. Certain of the other benefit structures provide partic-

ipant’s retirement benefits based on the number of years of benefit service

and a percentage of the participant’s average annual compensation during

the five highest paid consecutive years of the last ten years of employment.

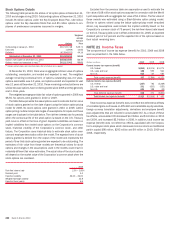

As a result of the Merrill Lynch acquisition, the Corporation assumed the

obligations related to the plans of Merrill Lynch. These plans include a

terminated U.S. pension plan, non-U.S. pension plans, nonqualified pension

plans and postretirement plans. The non-U.S. pension plans vary based on

the country and local practices. The terminated U.S. pension plan is referred

to as the Other Pension Plan.

In 1988, Merrill Lynch purchased a group annuity contract that guarantees

the payment of benefits vested under the terminated U.S. pension plan. The

Corporation, under a supplemental agreement, may be responsible for, or

benefit from actual experience and investment performance of the annuity

assets. The Corporation made no contribution in 2010 and contributed

$120 million during 2009 under this agreement. Additional contributions

may be required in the future under this agreement.

The Corporation sponsors a number of noncontributory, nonqualified

pension plans (the Nonqualified Pension Plans). As a result of acquisitions,

the Corporation assumed the obligations related to the noncontributory,

nonqualified pension plans of certain legacy companies including Merrill

Lynch. These plans, which are unfunded, provide defined pension benefits

to certain employees.

In addition to retirement pension benefits, full-time, salaried employees

and certain part-time employees may become eligible to continue participa-

tion as retirees in health care and/or life insurance plans sponsored by the

Corporation. Based on the other provisions of the individual plans, certain

retirees may also have the cost of these benefits partially paid by the

Corporation. The obligations assumed as a result of acquisitions are sub-

stantially similar to the Corporation’s postretirement health and life plans,

except for Countrywide which did not have a postretirement health and life

plan. Collectively, these plans are referred to as the Postretirement Health

and Life Plans.

214 Bank of America 2010