Bank of America 2010 Annual Report Download - page 184

Download and view the complete annual report

Please find page 184 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

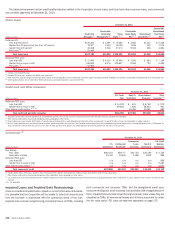

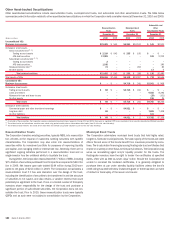

Other Asset-backed Securitizations

Other asset-backed securitizations include resecuritization trusts, municipal bond trusts, and automobile and other securitization trusts. The table below

summarizes select information related to other asset-backed securitizations in which the Corporation held a variable interest at December 31, 2010 and 2009.

(Dollars in millions)

2010 2009 2010 2009 2010 2009

December 31 December 31 December 31

Resecuritization

Trusts

Municipal Bond

Trusts

Automobile and

Other

Securitization Trusts

Unconsolidated VIEs

Maximum loss exposure

$21,425

$543

$4,261

$10,143

$141

$2,511

On-balance sheet assets

Senior securities held

(1, 2)

:

Trading account assets

$2,324

$543

$255

$155

$–

$–

AFS debt securities

17,989

–

–

–

109

2,212

Subordinate securities held

(1, 2)

:

Trading account assets

2

–

–

–

–

–

AFS debt securities

1,036

–

–

–

–

195

Residual interests held

(3)

74

–

–

203

–

83

All other assets

–

–

–

–

17

5

Total retained positions

$21,425

$543

$255

$358

$126

$2,495

Total assets of VIEs

$55,006

$7,443

$6,108

$12,247

$774

$3,636

Consolidated VIEs

Maximum loss exposure

$–

$–

$4,716

$241

$2,061

$908

On-balance sheet assets

Trading account assets

$68

$–

$4,716

$241

$–

$–

Loans and leases

–

–

–

–

9,583

8,292

Allowance for loan and lease losses

–

–

–

–

(29)

(101)

All other assets

–

–

–

–

196

25

Total assets

$68

$–

$4,716

$241

$9,750

$8,216

On-balance sheet liabilities

Commercial paper and other short-term borrowings

$–

$–

$4,921

$–

$–

$–

Long-term debt

68

–

–

–

7,681

7,308

All other liabilities

–

–

–

2

101

–

Total liabilities

$68

$–

$4,921

$2

$7,782

$7,308

(1)

As a holder of these securities, the Corporation receives scheduled principal and interest payments. During 2010 and 2009, there were no significant OTTI losses recorded on those securities classified as AFS debt securities.

(2)

The retained senior and subordinate securities were valued using quoted market prices or observable market inputs (Level 2 of the fair value hierarchy).

(3)

The retained residual interests are carried at fair value which was derived using model valuations (Level 3 of the fair value hierarchy).

Resecuritization Trusts

The Corporation transfers existing securities, typically MBS, into resecuritiza-

tion vehicles at the request of customers seeking securities with specific

characteristics. The Corporation may also enter into resecuritizations of

securities within its investment portfolio for purposes of improving liquidity

and capital, and managing credit or interest rate risk. Generally, there are no

significant ongoing activities performed in a resecuritization trust and no

single investor has the unilateral ability to liquidate the trust.

During 2010, the Corporation resecuritized $97.7 billion of MBS, including

$71.3 billion of securities purchased from third parties compared to $49.2 bil-

lion in 2009. Net losses upon sale totaled $144 million during 2010 com-

pared to net gains of $213 million in 2009. The Corporation consolidates a

resecuritization trust if it has sole discretion over the design of the trust,

including the identification of securities to be transferred in and the structure

of securities to be issued, and also retains a variable interest that could

potentially be significant to the trust. If one or a limited number of third-party

investors share responsibility for the design of the trust and purchase a

significant portion of subordinate securities, the Corporation does not con-

solidate the trust. Prior to 2010, these resecuritization trusts were typically

QSPEs and as such were not subject to consolidation by the Corporation.

Municipal Bond Trusts

The Corporation administers municipal bond trusts that hold highly rated,

long-term, fixed-rate municipal bonds. The vast majority of the bonds are rated

AAA or AA and some of the bonds benefit from insurance provided by mono-

lines. The trusts obtain financing by issuing floating-rate trust certificates that

reprice on a weekly or other basis to third-party investors. The Corporation may

serve as remarketing agent and/or liquidity provider for the trusts. The

floating-rate investors have the right to tender the certificates at specified

dates, often with as little as seven days’ notice. Should the Corporation be

unable to remarket the tendered certificates, it is generally obligated to

purchase them at par under standby liquidity facilities unless the bond’s

credit rating has declined below investment-grade or there has been an event

of default or bankruptcy of the issuer and insurer.

182 Bank of America 2010