Bank of America 2010 Annual Report Download - page 192

Download and view the complete annual report

Please find page 192 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

repurchase process and the Corporation has used that experience to record a

liability related to existing and future claims from such counterparties.

At December 31, 2010, the unpaid principal balance of loans related to

unresolved repurchase requests previously received from monolines was

$4.8 billion, including $3.0 billion in repurchase requests that have been

reviewed where it is believed a valid defect has not been identified which would

constitute an actionable breach of representations and warranties and

$1.8 billion in repurchase requests that are in the process of review. As

discussed on the previous page, a portion of the repurchase requests that are

initially denied are ultimately resolved through repurchase or make-whole

payments, after additional dialogue and negotiation with the monoline insurer.

At December 31, 2010, the unpaid principal balance of loans for which the

monolines had requested loan files for review but for which no repurchase

request had been received was $10.2 billion, excluding loans that had been

paid in full. There will likely be additional requests for loan files in the future

leading to repurchase requests. Such requests may relate to loans that are

currently in securitization trusts or loans that have defaulted and are no longer

included in the unpaid principal balance of the loans in the trusts. However, it

is unlikely that a repurchase request will be received for every loan in a

securitization or every file requested or that a valid defect exists for every loan

repurchase request. In addition, any claims paid related to repurchase

requests from a monoline are paid to the securitization trust and may be

used by the securitization trust to repay any outstanding monoline advances

or reduce future advances from the monolines. To the extent that a monoline

has not advanced funds or does not anticipate that it will be required to

advance funds to the securitization trust, the likelihood of receiving a repur-

chase request from a monoline may be reduced as the monoline would

receive limited or no benefit from the payment of repurchase claims. More-

over, some monolines are not currently performing their obligations under the

financial guaranty policies they issued which may, in certain circumstances,

impact their ability to present repurchase claims.

Whole Loan Sales and Private-label Securitizations

The Corporation and its subsidiaries have limited experience with private-label

securitization repurchases as the number of recent repurchase requests

received has been limited as shown in the outstanding claims table on

page 188. The representations and warranties, as governed by the private-

label securitizations, generally require that counterparties have the ability to

both assert a claim and actually prove that a loan has an actionable defect

under the applicable contracts. While a securitization trustee may always

investigate or demand repurchase on its own action, in order for investors to

direct the securitization trustee to investigate loan files or demand the

repurchase of loans, the securitization agreements generally require the

security holders to hold a specified percentage, such as 25 percent, of the

voting rights of the outstanding securities. In addition, the Corporation be-

lieves the agreements for private-label securitizations generally contain less

rigorous representations and warranties and higher burdens on investors

seeking repurchases than the comparable agreements with the GSEs.

The majority of repurchase requests that the Corporation has received

relate to whole loan sales. Most of the loans sold in the form of whole loans

were subsequently pooled with other mortgages into private-label securitiza-

tions issued by third-party buyers of the loans. The buyers of the whole loans

received representations and warranties in the sales transaction and may

retain those rights even when the loans are aggregated with other collateral

into private-label securitizations. Properly presented repurchase requests for

these whole loans are reviewed on a loan-by-loan basis. If, after the Corpo-

ration’s review, it does not believe a claim is valid, it will deny the claim and

generally indicate a reason for the denial. When the counterparty agrees with

the Corporation’s denial of the claim, the counterparty may rescind the claim.

When there is disagreement as to the resolution of the claim, meaningful

dialogue and negotiation between the parties is generally necessary to reach

conclusion on an individual claim. Generally, a whole loan sale claimant is

engaged in the repurchase process and the Corporation and the claimant

reach resolution, either through loan-by-loan negotiation or at times, through a

bulk settlement. Through December 31, 2010, approximately 17 percent of

the whole loan claims that the Corporation initially denied have subsequently

been resolved through repurchase or make-whole payments and 53 percent

have been resolved through rescission or repayment in full by the borrower.

Although the timeline for resolution varies, once an actionable breach is

identified on a given loan, settlement is generally reached as to that loan

within 60 to 90 days. When a claim has been denied and the Corporation does

not have communication with the counterparty for six months, the Corporation

views these claims as inactive; however, they remain in the outstanding

claims balance until resolution.

On October 18, 2010, Countrywide Home Loans Servicing, LP (which

changed its name to BAC Home Loans Servicing, LP), a wholly-owned sub-

sidiary of the Corporation, in its capacity as servicer on 115 private-label

securitizations, which was subsequently extended to 225 securitizations,

received a letter that asserts breaches of certain servicing obligations,

including an alleged failure to provide notice of breaches of representations

and warranties with respect to mortgage loans included in the transactions.

Additionally, the Corporation received new claim demands totaling $1.7 billion

in correspondence from private-label securitization investors. Private-label

securitization investors generally do not have the contractual right to demand

repurchase of loans directly or the right to access loan files. The inclusion of

the $1.7 billion in outstanding claims does not mean that the Corporation

believes these claims have satisfied the contractual thresholds required for

the private-label securitization investors to direct the securitization trustee to

take action or are otherwise procedurally or substantively valid.

Liability for Representations and Warranties and

Corporate Guarantees

The liability for representations and warranties and corporate guarantees is

included in accrued expenses and other liabilities and the related provision is

included in mortgage banking income.

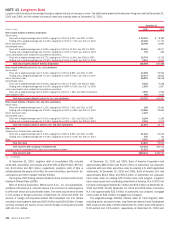

The table below presents a rollforward of the liability for representations

and warranties and corporate guarantees.

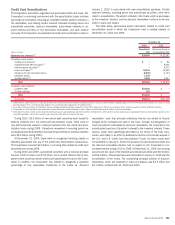

(Dollars in millions)

2010 2009

Liability for representations and warranties and

corporate guarantees, beginning of year

$3,507

$2,271

Merrill Lynch acquisition

–

580

Additions for new sales

30

41

Charge-offs

(4,803)

(1,312)

Provision

6,786

1,851

Other

(82)

76

Liability for representations and warranties

and corporate guarantees, December 31

$5,438

$3,507

The liability for representations and warranties has been established

when those obligations are both probable and reasonably estimable. As

previously discussed, the Corporation reached agreements with the GSEs

resolving repurchase claims involving certain residential mortgage loans sold

to them by entities related to legacy Countrywide. The Corporation’s liability

for obligations under representations and warranties given to the GSEs

considers the recent agreements and their impact on the repurchase rates

on future claims that may be received on loans that have defaulted or that are

estimated to default. The Corporation believes that its remaining exposure to

repurchase obligations for first-lien residential mortgage loans sold directly to

the GSEs has been accounted for as a result of these agreements and the

associated adjustments to the recorded liability for representations and

190 Bank of America 2010