Bank of America 2010 Annual Report Download - page 173

Download and view the complete annual report

Please find page 173 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

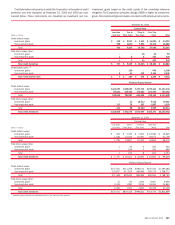

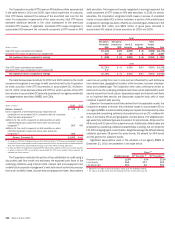

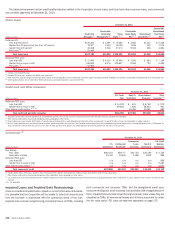

Nonperforming Loans and Leases

The table below includes the Corporation’s nonperforming loans and leases,

including nonperforming TDRs, and loans accruing past due 90 days or more

at December 31, 2010 and 2009. Nonperforming loans and leases exclude

performing TDRs and loans accounted for under the fair value option. Non-

performing LHFS are excluded from nonperforming loans and leases as they

are recorded at either fair value or the lower of cost or fair value. In addition,

PCI, consumer credit card, business card loans and in general, consumer

loans not secured by real estate, including renegotiated loans, are not

considered nonperforming and are therefore excluded from nonperforming

loans and leases in the table. See Note 1 – Summary of Significant Account-

ing Principles for further information on the criteria to determine if a loan is

classified as nonperforming. Real estate-secured past due consumer loans

insured by the FHA are reported as performing since the principal repayment

is insured by the FHA.

(Dollars in millions)

2010 2009 2010 2009

December 31 December 31

Nonperforming Loans

and Leases

Accruing Past Due

90 Days or More

Home loans

Residential mortgage

(1)

$17,691

$16,596

$16,768

$11,680

Home equity

2,694

3,804

–

–

Discontinued real estate

331

249

–

–

Credit card and other consumer

U.S. credit card

n/a

n/a

3,320

2,158

Non-U.S. credit card

n/a

n/a

599

515

Direct/Indirect consumer

90

86

1,058

1,488

Other consumer

48

104

2

3

Total consumer

20,854

20,839

21,747

15,844

Commercial

U.S. commercial

3,453

4,925

236

213

Commercial real estate

5,829

7,286

47

80

Commercial lease financing

117

115

18

32

Non-U.S. commercial

233

177

6

67

U.S. small business commercial

204

200

325

624

Total commercial

9,836

12,703

632

1,016

Total consumer and commercial

$30,690

$33,542

$22,379

$16,860

(1)

Residential mortgage loans accruing past due 90 days or more represent loans insured by the FHA. At December 31, 2010 and 2009, residential mortgage includes $8.3 billion and $2.2 billion of loans that are no longer accruing

interest as interest has been curtailed by the FHA although principal is still insured.

n/a = not applicable

Included in certain loan categories in nonperforming loans and leases in

the table above are TDRs that were classified as nonperforming. At Decem-

ber 31, 2010 and 2009, the Corporation had $3.0 billion and $2.9 billion of

residential mortgages, $535 million and $1.7 billion of home equity, $75 mil-

lion and $43 million of discontinued real estate, $175 million and $227 million

of U.S. commercial, $770 million and $246 million of commercial real estate

and $7 million and $13 million of non-U.S. commercial loans that were TDRs

and classified as nonperforming.

As a result of new accounting guidance on PCI loans, beginning January 1,

2010, modification of a PCI loan no longer results in removal of the loan from

the PCI loan pool. TDRs in the consumer real estate portfolio that were

removed from the PCI loan portfolio prior to the adoption of the new account-

ing guidance were $2.1 billion and $2.3 billion at December 31, 2010 and

2009, of which $426 million and $395 million were nonperforming. These

nonperforming loans are excluded from the table above.

Credit Quality Indicators

The Corporation monitors credit quality within its three portfolio segments

based on primary credit quality indicators. Within the home loans portfolio

segment, the primary credit quality indicators used are refreshed LTV and

refreshed FICO score. Refreshed LTV measures the carrying value of the loan

as a percentage of the value of property securing the loan, refreshed quar-

terly. Home equity loans are measured using combined LTV which measures

the carrying value of the combined loans that have liens against the property

and the available line of credit as a percentage of the appraised value of the

property securing the loan, refreshed quarterly. Refreshed FICO score mea-

sures the creditworthiness of the borrower based on the financial obligations

of the borrower and the borrower’s credit history. At a minimum, FICO scores

are refreshed quarterly, and in many cases, more frequently. Refreshed FICO

score is also a primary credit quality indicator for the credit card and other

consumer portfolio segment and the business card portfolio within U.S. small

business commercial. The Corporation’s commercial loans are evaluated

using pass rated or reservable criticized as the primary credit quality indicator.

The term reservable criticized refers to those commercial loans that are

internally classified or listed by the Corporation as special mention, substan-

dard or doubtful. These assets pose an elevated risk and may have a high

probability of default or total loss. Pass rated refers to all loans not considered

criticized. In addition to these primary credit quality indicators, the Corporation

uses other credit quality indicators for certain types of loans.

See Note 1 – Summary of Significant Accounting Principles for additional

information.

Bank of America 2010 171