Bank of America 2010 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

Recent Events

Representations and Warranties Liability

On December 31, 2010, we reached agreements with Freddie Mac (FHLMC)

and Fannie Mae (FNMA), collectively the GSEs, where the Corporation paid

$2.8 billion to resolve repurchase claims involving first-lien residential mort-

gage loans sold directly to the GSEs by entities related to legacy Countrywide

(Countrywide). The agreement with FHLMC extinguishes all outstanding and

potential mortgage repurchase and make-whole claims arising out of any

alleged breaches of selling representations and warranties related to loans

sold directly by legacy Countrywide to FHLMC through 2008, subject to certain

exceptions we do not believe will be material. The agreement with FNMA

substantially resolves the existing pipeline of repurchase and make-whole

claims outstanding as of September 20, 2010 arising out of alleged breaches

of selling representations and warranties related to loans sold directly by

legacy Countrywide to FNMA. These agreements with the GSEs do not cover

outstanding and potential mortgage repurchase and make-whole claims

arising out of any alleged breaches of selling representations and warranties

to legacy Bank of America first-lien residential mortgage loans sold directly to

the GSEs or other loans sold directly to the GSEs other than described above,

loan servicing obligations, other contractual obligations or loans contained in

private-label securitizations.

As a result of these agreements and associated adjustments made to the

representations and warranties liability for other loans sold directly to the GSEs

and not covered by the agreements, the Corporation recorded a provision of

$3.0 billion during the fourth quarter of 2010. We believe that our remaining

exposure to representations and warranties for first-lien residential mortgage

loans sold directly to the GSEs has been accounted for as a result of these

agreements and the associated adjustments to our recorded liability for rep-

resentations and warranties for first-lien residential mortgage for loans sold

directly to the GSEs and not covered by the agreements as discussed above. We

believe our predictive repurchase models, utilizing our historical repurchase

experience with the GSEs while considering current developments, including the

recent agreements, projections of future defaults as well as certain assump-

tions regarding economic conditions, home prices and other matters, allows us

to reasonably estimate the liability for obligations under representations and

warranties on loans sold to the GSEs. However, future provisions for represen-

tations and warranties liability to the GSEs may be affected if actual experience

is different from our historical experience with the GSEs or our projections of

future defaults, and assumptions regarding economic conditions, home prices

and other matters, that are incorporated in the provision calculation.

Although our experience with non-GSE claims remains limited, we expect

additional activity in this area going forward and that the volume of repurchase

claims from monolines, whole-loan investors and investors in private-label

securitizations could increase in the future. It is reasonably possible that future

losses may occur, and our estimate is that the upper range of possible loss

related to non-GSE sales could be $7 billion to $10 billion over existing accruals.

This estimate does not represent a probable loss, is based on currently

available information, significant judgment, and a number of assumptions that

are subject to change. A significant portion of this estimate relates to loans

originated through legacy Countrywide, and the repurchase liability is generally

limited to the original seller of the loan. Future provisions and possible loss or

range of loss may be impacted if actual results are different from our assump-

tions regarding economic conditions, home prices and other matters and may

vary by counterparty. The resolution of the repurchase claims process with the

non-GSE counterparties will likely be a protracted process, and we will vigorously

contest any request for repurchase if we conclude that a valid basis for the

repurchase claim does not exist. For additional information about representa-

tions and warranties, see Note 9 – Representations and Warranties Obligations

and Corporate Guarantees to the Consolidated Financial Statements and

Representations and Warranties beginning on page 56.

Goodwill

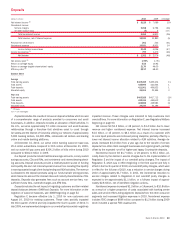

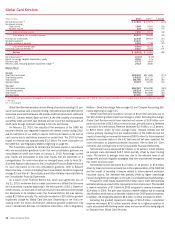

In 2010, we recorded a $10.4 billion goodwill impairment charge in Global

Card Services and a $2.0 billion goodwill impairment charge in Home Loans &

Insurance. These goodwill impairment charges are non-cash, non-tax deduct-

ible and have no impact on our reported Tier 1 and tangible equity ratios. Our

consumer and small business card products, including the debit card busi-

ness, are part of an integrated platform within Global Card Services.Basedon

the provisions of the Financial Reform Act which limit the interchange fees that

may be charged with respect to electronic debit interchange, we estimate a

revenue loss, beginning in the third quarter of 2011, of approximately

$2.0 billion annually based on current volumes and assuming limited miti-

gation within this segment. Accordingly, we performed a goodwill impairment

analysis during the three months ended September 30, 2010. This analysis

indicated that the implied fair value of the goodwill in Global Card Services

was less than the carrying value, and accordingly, we recorded a $10.4 billion

charge to reduce the carrying value to fair value.

During the three months ended December 31, 2010, we performed a

goodwill impairment analysis for Home Loans & Insurance as it was likely that

there had been a decline in its fair value as a result of increased uncertainties,

including existing and potential litigation exposure and other related risks,

higher servicing costs including loss mitigation efforts, foreclosure related

issues and the redeployment of centralized sales resources to address

servicing needs. This analysis indicated that the implied fair value of the

goodwill in Home Loans & Insurance was less than the carrying value, and

accordingly, we recorded a $2 billion charge to reduce the carrying value of

goodwill in Home Loans & Insurance.

For additional information on the goodwill impairment charges, see Com-

plex Accounting Estimates — Goodwill and Intangible Assets beginning on

page 114 and Note 10 — Goodwill and Intangible Assets to the Consolidated

Financial Statements.

Review of Foreclosure Processes

On October 1, 2010, we voluntarily stopped taking residential mortgage

foreclosure proceedings to judgment in states where foreclosure requires

a court order following a legal proceeding (judicial states). On October 8,

2010, we stopped foreclosure sales in all states in order to complete an

assessment of the related business processes. These actions generally did

not affect the initiation and processing of foreclosures prior to judgment, or

sale of vacant real estate owned properties. We took these precautionary

steps in order to ensure our processes for handling foreclosures include the

appropriate controls and quality assurance. Our review has involved an

assessment of the foreclosure process, including a review of completed

foreclosure affidavits in pending proceedings.

As a result of that review, we identified and implemented process and

control enhancements, and we intend to monitor ongoing quality results of

each process. The process and control enhancements implemented as a

result of our review are intended to strengthen the controls related to prep-

aration, execution and notarization of affidavits in judicial states and

strengthen our oversight of lawyers in the attorney network who conduct

foreclosure proceedings on our behalf, both in judicial states and in states

where foreclosures are handled without judicial supervision (non-judicial

states). This oversight includes a periodic review of a sample of foreclosure

files maintained by these attorneys, and on-site reviews of law firms in the

attorney network. In addition, our process and control enhancements for both

judicial and non-judicial states include strengthening the controls related to the

preparation and execution of other foreclosure loan documentation, including

notices of default and pre-foreclosure loss mitigation affidavits, as well as

enhanced associate training. After these enhancements were put in place, we

resumed foreclosure sales in most non-judicial states during the fourth quarter

of 2010, and expect sales to resume in the remaining non-judicial states in the

Bank of America 2010 37