Bank of America 2010 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

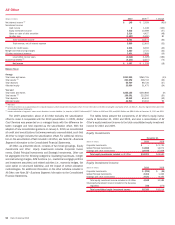

|

|

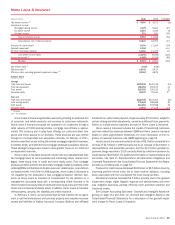

Home Loans & Insurance

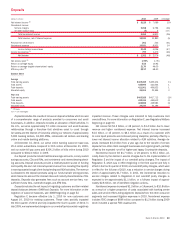

(Dollars in millions)

2010 2009 % Change

Net interest income

(1)

$4,690

$ 4,975 (6)%

Noninterest income:

Mortgage banking income

3,079

9,321 (67)

Insurance income

2,257

2,346 (4)

All other income

621

261 138

Total noninterest income

5,957

11,928 (50)

Total revenue, net of interest expense

10,647

16,903 (37)

Provision for credit losses

8,490

11,244 (24)

Goodwill impairment

2,000

–n/m

All other noninterest expense

13,163

11,705 12

Loss before income taxes

(13,006)

(6,046) (115)

Income tax benefit

(1)

(4,085)

(2,195) (86)

Net loss

$ (8,921)

$ (3,851) (132)

Net interest yield

(1)

2.52%

2.58%

Efficiency ratio

(1)

142.42

69.25

Efficiency ratio, excluding goodwill impairment charge

(1)

123.63

69.25

Balance Sheet

Average

Total loans and leases

$129,236

$130,519 (1)%

Total earning assets

186,455

193,152 (3)

Total assets

226,352

230,123 (2)

Allocated equity

26,170

20,530 27

Year end

Total loans and leases

$122,935

$131,302 (6)%

Total earning assets

173,033

188,349 (8)

Total assets

213,455

232,588 (8)

Allocated equity

23,542

27,148 (13)

(1)

FTE basis

n/m = not meaningful

Home Loans & Insurance generates revenue by providing an extensive line

of consumer real estate products and services to customers nationwide.

Home Loans & Insurance products are available to our customers through a

retail network of 5,900 banking centers, mortgage loan officers in approxi-

mately 750 locations and a sales force offering our customers direct tele-

phone and online access to our products. These products are also offered

through our correspondent loan acquisition channels. On February 4, 2011,

we announced that we are exiting the reverse mortgage origination business.

In October 2010, we exited the first mortgage wholesale acquisition channel.

These strategic changes were made to allow greater focus on our retail and

correspondent channels.

Home Loans & Insurance products include fixed and adjustable-rate first-

lien mortgage loans for home purchase and refinancing needs, reverse mort-

gages, home equity lines of credit and home equity loans. First mortgage

products are either sold into the secondary mortgage market to investors, while

retaining MSRs and the Bank of America customer relationships, or are held on

our balance sheet in All Other for ALM purposes. Home Loans & Insurance is

not impacted by the Corporation’s first mortgage production retention deci-

sions as Home Loans & Insurance is compensated for the decision on a

management accounting basis with a corresponding offset recorded in All

Other. Funded home equity lines of credit and home equity loans are held on the

Home Loans & Insurance balance sheet. In addition, Home Loans & Insurance

offers property, casualty, life, disability and credit insurance.

On February 3, 2011, we announced that we had entered into an agree-

ment to sell the lender-placed and voluntary property and casualty insurance

assets and liabilities of Balboa Insurance Company (Balboa) and affiliated

entities for an upfront cash payment of approximately $700 million, subject to

certain closing and other adjustments, as well as additional future payments.

Balboa is a wholly-owned subsidiary and part of Home Loans & Insurance.

Home Loans & Insurance includes the impact of transferring customers

and their related loan balances between GWIM and Home Loans & Insurance

based on client segmentation thresholds. For more information on the mi-

gration of customer balances, see GWIM beginning on page 52.

Home Loans & Insurance recorded a net loss of $8.9 billion compared to a

net loss of $3.9 billion in 2009 primarily due to an increase of $4.9 billion in

representations and warranties provision and the $2.0 billion goodwill im-

pairment charge recorded in 2010, partially offset by a decline in provision for

credit losses of $2.8 billion. For additional information on representations and

warranties, see Note 9 – Representations and Warranties Obligations and

Corporate Guarantees to the Consolidated Financial Statements and Repre-

sentations and Warranties on page 56.

Provision for credit losses decreased $2.8 billion to $8.5 billion driven by

improving portfolio trends which led to lower reserve additions, including

those associated with the Countrywide PCI home equity portfolio.

Noninterest expense increased $3.5 billion primarily due to the goodwill

impairment charge, higher litigation expense and default-related and other

loss mitigation expenses, partially offset by lower production expense and

insurance losses.

See Complex Accounting Estimates – Goodwill and Intangible Assets be-

ginning on page 114 and Note 10 – Goodwill and Intangible Assets to the

Consolidated Financial Statements for a discussion of the goodwill impair-

ment charge for Home Loans & Insurance.

Bank of America 2010 45