Bank of America 2010 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

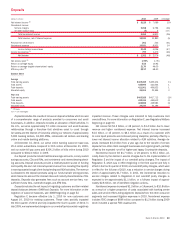

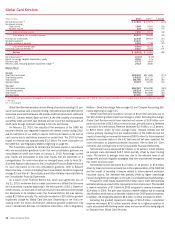

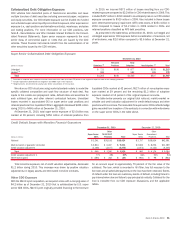

Deposits

(Dollars in millions)

2010 2009 % Change

Net interest income

(1)

$8,128

$ 7,089 15%

Noninterest income:

Service charges

5,058

6,796 (26)

All other income (loss)

(5)

5n/m

Total noninterest income

5,053

6,801 (26)

Total revenue, net of interest expense

13,181

13,890 (5)

Provision for credit losses

201

343 (41)

Noninterest expense

10,831

9,501 14

Income before income taxes

2,149

4,046 (47)

Income tax expense

(1)

797

1,470 (46)

Net income

$1,352

$ 2,576 (48)

Net interest yield

(1)

1.99%

1.75%

Return on average equity

5.58

10.92

Return on average tangible shareholders’ equity

21.70

46.00

Efficiency ratio

(1)

82.17

68.40

Balance Sheet

Average

Total earning assets

$409,359

$405,104 1%

Total assets

435,994

431,564 1

Total deposits

411,001

406,823 1

Allocated equity

24,204

23,594 3

Year end

Total earning assets

$403,926

$417,713 (3)%

Total assets

432,334

444,612 (3)

Total deposits

406,856

419,583 (3)

Allocated equity

24,273

24,186 –

(1)

FTE basis

n/m = not meaningful

Deposits includes the results of consumer deposit activities which consist

of a comprehensive range of products provided to consumers and small

businesses. In addition, Deposits includes an allocation of ALM activities. In

the U.S., we serve approximately 57 million consumer and small business

relationships through a franchise that stretches coast to coast through

32 states and the District of Columbia utilizing our network of approximately

5,900 banking centers, 18,000 ATMs, nationwide call centers and leading

online and mobile banking platforms.

At December 31, 2010, our active online banking customer base was

29.3 million subscribers compared to 29.6 million at December 31, 2009,

and our active bill pay users paid $304.3 billion of bills online during 2010

compared to $302.4 billion in 2009.

Our deposit products include traditional savings accounts, money market

savings accounts, CDs and IRAs, and noninterest- and interest-bearing check-

ing accounts. Deposit products provide a relatively stable source of funding

and liquidity. We earn net interest spread revenue from investing this liquidity

in earning assets through client-facing lending and ALM activities. The revenue

is allocated to the deposit products using our funds transfer pricing process

which takes into account the interest rates and maturity characteristics of the

deposits. Deposits also generates fees such as account service fees, non-

sufficient funds fees, overdraft charges and ATM fees.

Deposits includes the net impact of migrating customers and their related

deposit balances between GWIM and Deposits. For more information on the

migration of customer balances, see GWIM beginning on page 52.

Regulation E became effective July 1, 2010 for new customers and

August 16, 2010 for existing customers. These rules partially impacted

the third quarter of 2010 and fully impacted the fourth quarter of 2010. In

late 2009, we implemented changes in our overdraft policies which negatively

impacted revenue. These changes were intended to help customers limit

overdraft fees. For more information on Regulation E, see Regulatory Matters

beginning on page 60.

Net income fell $1.2 billion, or 48 percent, to $1.4 billion due to lower

revenue and higher noninterest expense. Net interest income increased

$1.0 billion, or 15 percent, to $8.1 billion as a result of a customer shift

to more liquid products and continued pricing discipline, partially offset by a

lower net interest income allocation related to ALM activities. Average de-

posits increased $4.2 billion from a year ago due to the transfer of certain

deposits from other client managed businesses and organic growth, partially

offset by the expected run-off of higher-cost legacy Countrywide deposits.

Noninterest income fell $1.7 billion, or 26 percent, to $5.1 billion, pri-

marily driven by the decline in service charges due to the implementation of

Regulation E and the impact of our overdraft policy changes. The impact of

Regulation E, which was in effect beginning in the third quarter and fully in

effect in the fourth quarter of 2010, and overdraft policy changes, which were

in effect for the full year of 2010, was a reduction in service charges during

2010 of approximately $1.7 billion. In 2011, the incremental reduction to

service charges related to Regulation E and overdraft policy changes is

expected to be approximately $1.1 billion, or a full-year impact of approxi-

mately $2.8 billion, net of identified mitigation actions.

Noninterest expense increased $1.3 billion, or 14 percent, to $10.8 billion

as a result of a higher proportion of costs associated with banking center

sales and service efforts being aligned to Deposits from the other consumer

segments and increased litigation expenses in 2010. Noninterest expense

includes FDIC charges of $896 million compared to $1.2 billion during 2009

which included a special FDIC assessment.

Bank of America 2010 43