Bank of America 2010 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

authority for Global Markets Risk Management including trading risk manage-

ment. The GRC’s focus is to take a forward-looking view of the primary credit

and market risks impacting GBAM and prioritize those that need a proactive

risk mitigation strategy. Market risks that impact lines of business outside of

GBAM are monitored and governed by their respective governance authorities.

The GRC monitors significant daily revenues and losses by business and

the primary drivers of the revenues or losses. Thresholds are in place for each

of our businesses in order to determine if the revenue or loss is considered to

be significant for that business. If any of the thresholds are exceeded, an

explanation of the variance is provided to the GRC. The thresholds are

developed in coordination with the respective risk managers to highlight

those revenues or losses that exceed what is considered to be normal daily

income statement volatility.

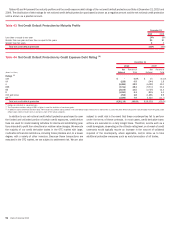

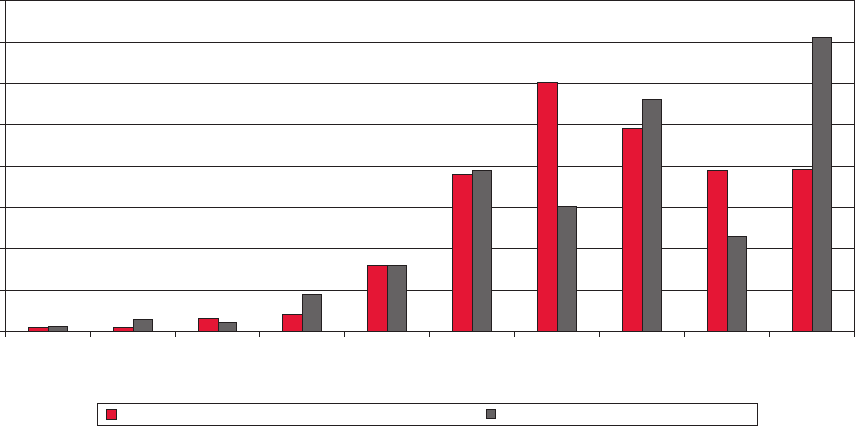

The histogram below is a graphic depiction of trading volatility and illus-

trates the daily level of trading-related revenue for the twelve months ended

December 31, 2010, as compared with the twelve months ended Decem-

ber 31, 2009. During the twelve months ended December 31, 2010, positive

trading-related revenue was recorded for 90 percent of the trading days of

which 75 percent were daily trading gains of over $25 million, four percent of

the trading days had losses greater than $25 million and the largest loss was

$102 million. This can be compared to the twelve months ended Decem-

ber 31, 2009, where positive trading-related revenue was recorded for 88 per-

cent of the trading days of which 72 percent were daily trading gains of over

$25 million, six percent of the trading days had losses greater than $25 mil-

lion and the largest loss was $100 million.

Histogram of Daily Trading-related Revenue

< -100 -100 to -75 -75 to -50 -50 to -25 -25 to 0 0 to 25 25 to 50 50 to 75 75 to 100 > 100

Revenue (dollars in millions)

Twelve Months Ended December 31, 2010 Twelve Months Ended December 31, 2009

80

70

60

50

40

30

20

10

0

Number of Days

To evaluate risk in our trading activities, we focus on the actual and

potential volatility of individual positions as well as portfolios. VaR is a key

statistic used to measure market risk. In order to manage day-to-day risks,

VaR is subject to trading limits both for our overall trading portfolio and within

individual businesses. All limit excesses are communicated to management

for review.

A VaR model simulates the value of a portfolio under a range of hypo-

thetical scenarios in order to generate a distribution of potential gains and

losses. VaR represents the worst loss the portfolio is expected to experience

based on historical trends with a given level of confidence and depends on the

volatility of the positions in the portfolio and on how strongly their risks are

correlated. Within any VaR model, there are significant and numerous as-

sumptions that will differ from company to company. In addition, the accuracy

of a VaR model depends on the availability and quality of historical data for

each of the positions in the portfolio. A VaR model may require additional

modeling assumptions for new products that do not have extensive historical

price data or for illiquid positions for which accurate daily prices are not

consistently available.

A VaR model is an effective tool in estimating ranges of potential gains and

losses on our trading portfolios. There are however many limitations inherent

in a VaR model as it utilizes historical results over a defined time period to

estimate future performance. Historical results may not always be indicative

of future results and changes in market conditions or in the composition of the

underlying portfolio could have a material impact on the accuracy of the VaR

model. In order for the VaR model to reflect current market conditions, we

update the historical data underlying our VaR model on a bi-weekly basis and

regularly review the assumptions underlying the model.

We continually review, evaluate and enhance our VaR model so that it

reflects the material risks in our trading portfolio. Nevertheless, due to the

limitations mentioned above, we have historically used the VaR model as only

one of the components in managing our trading risk and also use other

techniques such as stress testing and desk level limits. Periods of extreme

market stress influence the reliability of these techniques to varying degrees.

The accuracy of the VaR methodology is reviewed by backtesting (i.e.,

comparing actual results against expectations derived from historical data)

the VaR results against the daily profit and loss. Graphic representation of the

backtesting results with additional explanation of backtesting excesses are

reported to the GRC. Backtesting excesses occur when trading losses exceed

VaR. Senior management reviews and evaluates the results of these tests. In

periods of market stress, the GRC members communicate daily to discuss

losses and VaR limit excesses. As a result of this process, the lines of

business may selectively reduce risk. Where economically feasible, positions

are sold or macroeconomic hedges are executed to reduce the exposure.

Bank of America 2010 105