Bank of America 2010 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

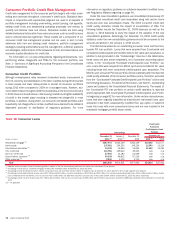

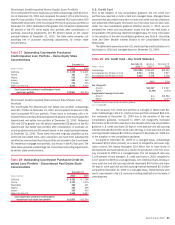

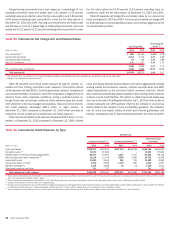

Purchased Credit-impaired Home Equity Loan Portfolio

The Countrywide PCI home equity loan portfolio outstandings were $12.6 bil-

lion at December 31, 2010 and comprised 36 percent of the total Country-

wide PCI loan portfolio. Those loans with a refreshed FICO score below 620

represented 26 percent of the Countrywide PCI home equity loan portfolio at

December 31, 2010. Refreshed CLTVs greater than 90 percent represented

85 percent of the PCI home equity loan portfolio after consideration of

purchase accounting adjustments and 85 percent based on the unpaid

principal balance at December 31, 2010. The table below presents out-

standings net of purchase accounting adjustments, by certain state

concentrations.

Table 27 Outstanding Countrywide Purchased

Credit-impaired Loan Portfolio – Home Equity State

Concentrations

(Dollars in millions)

2010 2009

December 31

California

$4,178

$4,311

Florida

750

765

Virginia

532

550

Arizona

520

542

Colorado

375

416

Other U.S./Non-U.S.

6,235

6,630

Total Countrywide purchased credit-impaired home

equity loan portfolio

$12,590

$13,214

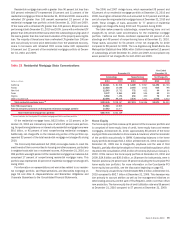

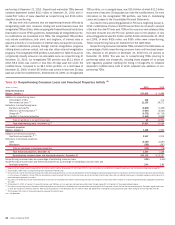

Purchased Credit-impaired Discontinued Real Estate Loan

Portfolio

The Countrywide PCI discontinued real estate loan portfolio outstandings

were $11.7 billion at December 31, 2010 and comprised 34 percent of the

total Countrywide PCI loan portfolio. Those loans to borrowers with a re-

freshed FICO score below 620 represented 62 percent of the Countrywide PCI

discontinued real estate loan portfolio at December 31, 2010. Refreshed

LTVs and CLTVs greater than 90 percent represented 55 percent of the PCI

discontinued real estate loan portfolio after consideration of purchase ac-

counting adjustments and 83 percent based on the unpaid principal balance

at December 31, 2010. Those loans that were originally classified as dis-

continued real estate loans upon acquisition and have been subsequently

modified are now excluded from this portfolio and included in the Countrywide

PCI residential mortgage loan portfolio, but remain in the PCI loan pool. The

table below presents outstandings net of purchase accounting adjustments,

by certain state concentrations.

Table 28 Outstanding Countrywide Purchased Credit-im-

paired Loan Portfolio – Discontinued Real Estate State

Concentrations

(Dollars in millions)

2010 2009

December 31

California

$6,322

$7,148

Florida

1,121

1,315

Washington

368

421

Virginia

344

399

Arizona

339

430

Other U.S./Non-U.S.

3,158

3,537

Total Countrywide purchased credit-impaired

discontinued real estate loan portfolio

$11,652

$13,250

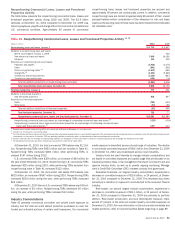

U.S. Credit Card

Prior to the adoption of new consolidation guidance, the U.S. credit card

portfolio was reported on both a held and managed basis. Managed basis

assumed that securitized loans were not sold into credit card securitizations

and presented credit quality information as if the loans had not been sold.

Under the new consolidation guidance effective January 1, 2010, we con-

solidated the credit card securitization trusts and the new held basis is

comparable to the previously reported managed basis. For more information

on the adoption of the new consolidation guidance, see Note 8 – Securitiza-

tions and Other Variable Interest Entities to the Consolidated Financial

Statements.

The table below presents certain U.S. credit card key credit statistics on a

held basis for 2010 and managed basis for December 31, 2009.

Table 29 U.S. Credit Card – Key Credit Statistics

(Dollars in millions)

December 31

2010

(1)

January 1

2010

(1)

December 31

2009

Outstandings

$113,785

$129,642 $49,453

Accruing past due 30 days or more

5,913

9,866 3,907

Accruing past due 90 days or more

3,320

5,408 2,158

2010 2009

Net charge-offs

Amount

$13,027

$6,547

Ratios

11.04%

12.50%

Supplemental managed basis data

Amount

n/a

$16,962

Ratios

n/a

12.07%

(1)

Balances reflect the impact of new consolidation guidance.

n/a = not applicable

The consumer U.S. credit card portfolio is managed in Global Card Ser-

vices. Outstandings in the U.S. credit card loan portfolio increased $64.3 bil-

lion compared to December 31, 2009 due to the adoption of the new

consolidation guidance. Compared to 2009, net charge-offs increased

$6.5 billion to $13.0 billion also due to the adoption of the new consolidation

guidance. U.S. credit card loans 30 days or more past due and still accruing

interest increased $2.0 billion while loans 90 days or more past due and still

accruing interest increased $1.2 billion compared to December 31, 2009 due

to the adoption of new consolidation guidance.

Compared to December 31, 2009 on a managed basis, outstandings

decreased $15.9 billion primarily as a result of charge-offs and lower origi-

nation volume. Net losses decreased $3.9 billion due to lower levels of

delinquencies and bankruptcies as a result of improvement in the U.S. econ-

omy compared to 2009 on a managed basis. The net charge-off ratio was

11.04 percent of total average U.S. credit card loans in 2010 compared to

12.07 percent in 2009 on a managed basis. U.S. credit card loans 30 days or

more past due and still accruing interest decreased $4.0 billion and loans

90 days or more past due and still accruing interest decreased $2.1 billion

compared to December 31, 2009 on a managed basis. These declines were

due to improvement in the U.S. economy including stabilization in the levels of

unemployment.

Bank of America 2010 83