Bank of America 2011 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

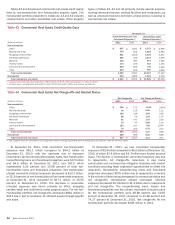

Bank of America 2011 101

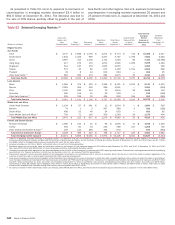

At December 31, 2011 and 2010, 60 percent and 70 percent

of our emerging markets exposure was in Asia Pacific. Emerging

markets exposure in Asia Pacific decreased by $8.5 billion driven

by a $19.0 billion decrease related to the sale of CCB shares,

partially offset by increases in loans and securities predominately

in India, China (excluding CCB) and South Korea.

At December 31, 2011 and 2010, 26 percent and 21 percent

of our emerging markets exposure was in Latin America. Latin

America emerging markets exposure increased $2.5 billion driven

by increases in securities and local exposure in Brazil.

At December 31, 2011 and 2010, eight percent and six percent

of our emerging markets exposure was in Middle East and Africa,

with an increase of $926 million primarily driven by increases in

loans and derivatives in United Arab Emirates, and by increases

in loans in Other Middle East and Africa. At December 31, 2011

and 2010, six percent and three percent of the emerging markets

exposure was in Central and Eastern Europe, with the increase

driven by an increase in loans in the Russian Federation.

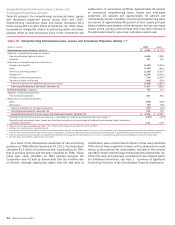

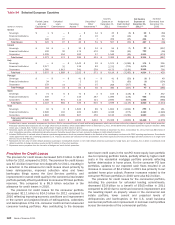

Certain European countries, including Greece, Ireland, Italy,

Portugal and Spain, have experienced varying degrees of financial

stress. Risks from the continued debt crisis in Europe could

continue to disrupt the financial markets which could have a

detrimental impact on global economic conditions and sovereign

and non-sovereign debt in these countries. Uncertainty in the

progress of debt restructuring negotiations and the lack of a clear

resolution to the crisis have led to continued volatility in European

financial markets, as well as global financial markets. In December

2011, the ECB announced initiatives to address European bank

liquidity and funding concerns by providing low-cost, three-year

loans to banks, and expanding collateral eligibility. In early 2012,

S&P, Fitch and Moody’s downgraded the credit ratings of several

European countries, and S&P downgraded the credit rating of the

EFSF, adding to concerns about investor appetite for continued

support in stabilizing the affected countries.

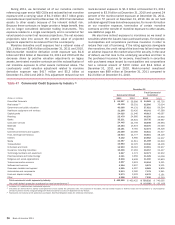

Table 54 shows our direct sovereign and non-sovereign

exposures, excluding consumer credit card exposure, in these

countries at December 31, 2011. Our total sovereign and non-

sovereign exposure to these countries was $15.3 billion at

December 31, 2011 compared to $16.6 billion at December 31,

2010. The total exposure to these countries, net of hedges, was

$10.5 billion at December 31, 2011 compared to $12.4 billion at

December 31, 2010, of which $252 million and $91 million was

total sovereign exposure. At December 31, 2011 and 2010, the

fair value of net credit default protection purchased was $4.9

billion and $4.2 billion.

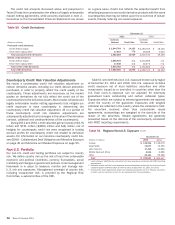

We hedge certain of our selected European country exposure

with credit default protection in the form of CDS. The majority of

our CDS contracts are with highly-rated financial institutions

primarily outside of the Eurozone and we work to limit or eliminate

correlated CDS. Due to our engagement in market-making

activities, our CDS portfolio contains contracts with various

maturities to a diverse set of counterparties.

In addition to our direct sovereign and non-sovereign exposures,

a significant deterioration of the European debt crisis could result

in material reductions in the value of sovereign debt and other

asset classes, disruptions in capital markets, widening of credit

spreads, loss of investor confidence in the financial services

industry, a slowdown in global economic activity and other adverse

developments. For additional information on the debt crisis in

Europe, see Item 1A. Risk Factors of this Annual Report on Form

10-K.

Losses could still result even if there is credit default protection

purchased because the purchased credit protection contracts only

pay out under certain scenarios and thus not all losses may be

covered by the credit protection contracts. The effectiveness of

our CDS protection as a hedge of these risks is influenced by a

number of factors, including the contractual terms of the CDS.

Generally, only the occurrence of a credit event as defined by the

CDS terms (which may include, among other events, the failure to

pay by, or restructuring of, the reference entity) results in a payment

under the purchased credit protection contracts. The

determination as to whether a credit event has occurred is made

by the relevant International Swaps and Derivatives Association,

Inc. (ISDA) Determination Committee (comprised of various ISDA

member firms) based on the terms of the CDS and facts and

circumstances for the event. Accordingly, uncertainties exist as to

whether any particular strategy or policy action for addressing

European debt crisis would constitute a credit event under the

CDS. A voluntary restructuring may not trigger a credit event under

CDS terms and consequently may not trigger a payment under the

CDS contract.