Bank of America 2011 Annual Report Download - page 204

Download and view the complete annual report

Please find page 204 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

202 Bank of America 2011

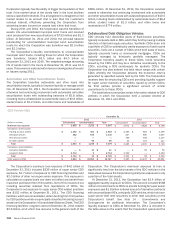

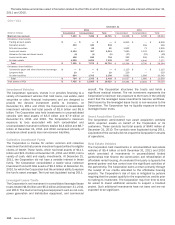

Outstanding Claims by Counterparty and Product

(Dollars in millions)

By counterparty (1)

GSEs

Monolines

Whole loan and private-label securitization investors

and other (2)

Total outstanding claims by counterparty

By product type (1)

Prime loans

Alt-A

Home equity

Pay option

Subprime

Other

Total outstanding claims by product type

December 31

2011

$ 6,258

3,082

4,912

$ 14,252

$ 3,928

2,333

2,872

3,588

891

640

$ 14,252

2010

$ 2,821

4,678

3,188

$ 10,687

$ 2,040

1,190

3,658

2,889

734

176

$ 10,687

(1) Excludes certain MI rescission notices. However, includes $1.2 billion of repurchase requests

received from the GSEs that have resulted solely from MI rescission notices. For additional

information, see Mortgage Insurance Rescission Notices in this Note.

(2) Amounts for December 31, 2011 and 2010 included $1.7 billion in demands contained in

correspondence from private-label securitizations investors in the Covered Trusts that do not

have the right to demand repurchase of loans directly or the right to access loan files. For

additional information, see Settlement with Bank of New York Mellon, as Trustee in this Note.

The number of repurchase claims as a percentage of the

number of loans purchased arising from loans sourced from

brokers or purchased from third-party sellers is relatively

consistent with the number of repurchase claims as a percentage

of the number of loans originated by the Corporation or its

subsidiaries or legacy companies.

Mortgage Insurance Rescission Notices

In addition to repurchase claims, the Corporation receives notices

from mortgage insurance companies of claim denials,

cancellations, or coverage rescission (collectively, MI rescission

notices) and the amount of such notices have remained elevated.

When there is disagreement with the mortgage insurer as to the

resolution of a MI rescission notice, meaningful dialogue and

negotiation are generally necessary between the parties to reach

a conclusion on an individual notice. The level of engagement of

the mortgage insurance companies varies and on-going litigation

involving some of the mortgage insurance companies over

individual and bulk rescissions or claims for rescission limits the

ability of the Corporation to engage in constructive dialogue leading

to resolution. For loans sold to GSEs or private-label securitization

trusts (including those wrapped by the monoline bond insurers),

a MI rescission may give rise to a claim for breach of the applicable

representations and warranties, depending on the governing sales

contracts. In those cases where the governing contract contains

a MI-related representation and warranty which upon rescission

requires the Corporation to repurchase the affected loan or

indemnify the investor for the related loss, the Corporation realizes

the loss without the benefit of MI. If the Corporation is required

to repurchase a loan or indemnify the investor as a result of a

different breach of representations and warranties and there has

been a MI rescission, or if the Corporation holds the loan for

investment, it realizes the loss without the benefit of MI. In addition,

mortgage insurance companies have in some cases asserted the

ability to curtail MI payments, which in these cases would reduce

the MI proceeds available to reduce the loss on the loan. While a

legitimate MI rescission may constitute a valid basis for

repurchase or other remedies under the GSE agreements and a

small number of private-label MBS securitizations, and a MI

rescission notice may result in a repurchase request, the

Corporation believes MI rescission notices in and of themselves

are not valid repurchase requests.

On June 30, 2011, FNMA issued an announcement requiring

servicers to report, effective October 1, 2011, all MI rescissions,

cancellations and claim denials (together, rescissions) with

respect to loans sold to FNMA. The announcement also confirmed

FNMA’s view of its position that a mortgage insurance company’s

issuance of a MI rescission notice constitutes a breach of the

lender’s representations and warranties and permits FNMA to

require the lender to repurchase the mortgage loan or promptly

remit a make-whole payment covering FNMA’s loss even if the

lender is contesting the MI rescission notice. A related

announcement included a ban on bulk settlements with mortgage

insurers that provide for loss sharing in lieu of rescission.

According to FNMA’s announcement, through June 30, 2012,

lenders have 90 days to appeal FNMA’s repurchase request and

30 days (or such other time frame specified by FNMA) to appeal

after that date. According to FNMA’s announcement, in order to be

successful in its appeal, a lender must provide documentation

confirming reinstatement or continuation of coverage. This

announcement could result in more repurchase requests from

FNMA than the assumptions in the Corporation’s estimated liability

contemplate. The Corporation also expects that in many cases

(particularly in the context of individual or bulk rescissions being

contested through litigation), it will not be able to resolve MI

rescission notices with the mortgage insurance companies before

the expiration of the appeal period prescribed by the FNMA

announcement. The Corporation has informed FNMA that it does

not believe that the new policy is valid under its contracts with

FNMA, and that it does not intend to repurchase loans under the

terms set forth in the new policy. The Corporation’s pipeline of

outstanding repurchase claims from the GSEs resulting solely on

MI rescission notices has increased during 2011 by $935 million

to $1.2 billion at December 31, 2011. If it is required to abide by

the terms of the new FNMA policy, the Corporation’s

representations and warranties liability will likely increase.

At December 31, 2011, the Corporation had approximately

90,000 open MI rescission notices compared to 72,000 at

December 31, 2010. Through December 31, 2011, 26 percent of

the MI rescission notices received have been resolved. Of those

resolved, 24 percent were resolved through the Corporation’s

acceptance of the MI rescission, 46 percent were resolved through

reinstatement of coverage or payment of the claim by the mortgage

insurance company, and 30 percent were resolved on an aggregate

basis through settlement, policy commutation or similar

arrangement. As of December 31, 2011, 74 percent of the MI

rescission notices the Corporation has received have not yet been

resolved. Of those not yet resolved, 48 percent are implicated by

ongoing litigation where no loan-level review is currently

contemplated (nor required to preserve the Corporation’s legal

rights). In this litigation, the litigating mortgage insurance

companies are also seeking bulk rescission of certain policies,

separate and apart from loan-by-loan denials or rescissions. The

Corporation is in the process of reviewing 11 percent of the

remaining open MI rescission notices, and the Corporation has

reviewed and is contesting the MI rescission with respect to 89

percent of these remaining open MI rescission notices. Of the

remaining open MI rescission notices, 29 percent are also the