Bank of America 2011 Annual Report Download - page 175

Download and view the complete annual report

Please find page 175 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 173

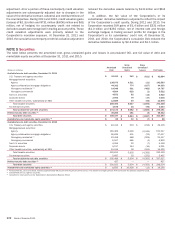

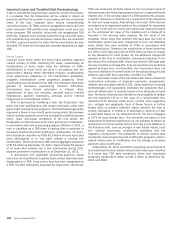

At December 31, 2011, the accumulated net unrealized gains

on AFS debt securities included in accumulated OCI were $3.1

billion, net of the related income tax expense of $1.9 billion. At

December 31, 2011 and 2010, the Corporation had

nonperforming AFS debt securities of $140 million and $44 million.

The Corporation recorded OTTI losses on AFS debt securities

for 2011 and 2010 as presented in the table below. A debt security

is impaired when its fair value is less than its amortized cost. If

the Corporation intends or will more-likely-than-not be required to

sell the debt securities prior to recovery, the entire impairment is

recorded in the Consolidated Statement of Income. For debt

securities the Corporation does not intend or will not more-likely-

than-not be required to sell, an analysis is performed to determine

if any of the impairment is due to credit or whether it is due to

other factors (e.g., interest rate). Credit losses are considered

unrecoverable and are recorded in the Consolidated Statement of

Income with the remaining unrealized losses recorded in

accumulated OCI. In certain instances, the credit loss on a debt

security may exceed the total impairment, in which case, the

portion of the credit loss that exceeds the total impairment is

recorded as an unrealized gain in accumulated OCI. Balances in

the table below exclude $9 million and $51 million of unrealized

gains recorded in accumulated OCI related to these securities for

2011 and 2010.

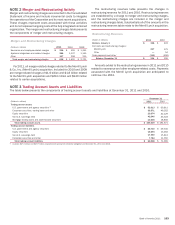

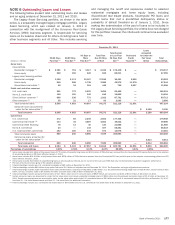

Net Impairment Losses Recognized in Earnings

(Dollars in millions)

Total OTTI losses (unrealized and realized)

Unrealized OTTI losses recognized in accumulated OCI

Net impairment losses recognized in earnings

Total OTTI losses (unrealized and realized)

Unrealized OTTI losses recognized in accumulated OCI

Net impairment losses recognized in earnings

Total OTTI losses (unrealized and realized)

Unrealized OTTI losses recognized in accumulated OCI

Net impairment losses recognized in earnings

2011

Non-agency

Residential

MBS

$ (348)

61

$ (287)

2010

$ (1,305)

817

$ (488)

2009

$ (2,240)

672

$ (1,568)

Non-agency

Commercial

MBS

$ (10)

—

$ (10)

$ (19)

15

$(4)

$(6)

—

$(6)

Non-U.S.

Securities

$—

—

$—

$ (276)

16

$ (260)

$ (360)

—

$ (360)

Corporate

Bonds

$—

—

$—

$(6)

2

$(4)

$ (87)

—

$ (87)

Other

Taxable

Securities

$(2)

—

$(2)

$ (568)

357

$ (211)

$ (815)

—

$ (815)

Total

$ (360)

61

$ (299)

$ (2,174)

1,207

$ (967)

$ (3,508)

672

$ (2,836)

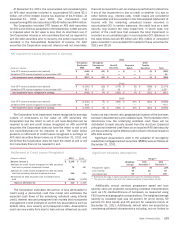

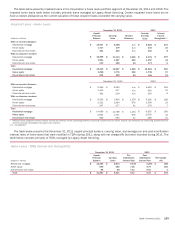

The Corporation’s net impairment losses recognized in earnings

consist of write-downs to fair value on AFS securities the

Corporation has the intent to sell or will more-likely-than-not be

required to sell and credit losses recognized on AFS and HTM

securities the Corporation does not have the intent to sell or will

not more-likely-than-not be required to sell. The table below

presents a rollforward of credit losses recognized in earnings on

AFS debt securities these losses as of December 31, 2011 and

2010 that the Corporation does not have the intent to sell or will

not more-likely-than-not be required to sell.

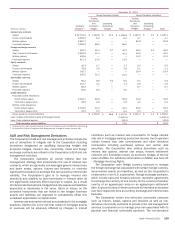

Rollforward of Credit Losses Recognized

(Dollars in millions)

Balance, January 1

Additions for credit losses recognized on debt securities

that had no previous impairment losses

Additions for credit losses recognized on debt securities

that had previously incurred impairment losses

Reductions for debt securities sold or intended to be

sold

Balance, December 31

2011

$ 2,148

72

149

(2,059)

$ 310

2010

$ 3,155

487

421

(1,915)

$ 2,148

The Corporation estimates the portion of loss attributable to

credit using a discounted cash flow model and estimates the

expected cash flows of the underlying collateral using internal

credit, interest rate and prepayment risk models that incorporate

management’s best estimate of current key assumptions such as

default rates, loss severity and prepayment rates. Assumptions

used can vary widely from loan to loan and are influenced by such

factors as loan interest rate, geographical location of the borrower,

borrower characteristics and collateral type. The Corporation then

determines how the underlying collateral cash flows will be

distributed to each security issued from the structure. Expected

principal and interest cash flows on an impaired AFS debt security

are discounted using the effective yield of each individual impaired

AFS debt security.

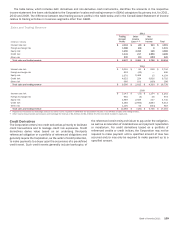

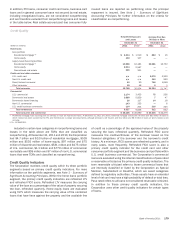

Significant assumptions used in the valuation of non-agency

residential mortgage-backed securities (RMBS) were as follows at

December 31, 2011.

Significant Valuation Assumptions

Prepayment speed

Loss severity

Life default rate

Weighted-

average

10%

49

50

Range (1)

10th

Percentile (2)

3%

15

2

90th

Percentile (2)

22%

62

100

(1) Represents the range of inputs/assumptions based upon the underlying collateral.

(2) The value of a variable below which the indicated percentile of observations will fall.

Additionally, annual constant prepayment speed and loss

severity rates are projected considering collateral characteristics

such as LTV, creditworthiness of borrowers as measured using

FICO scores and geographic concentrations. The weighted-average

severity by collateral type was 43 percent for prime bonds, 50

percent for Alt-A bonds and 60 percent for subprime bonds at

December 31, 2011. Additionally, default rates are projected by

considering collateral characteristics including, but not limited to