Bank of America 2011 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

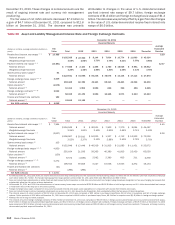

116 Bank of America 2011

more variability in market pricing or a lack of market data to use

in the valuation process. In keeping with the prudent application

of estimates and management judgment in determining the fair

value of assets and liabilities, we have in place various processes

and controls that include: a model validation policy that requires

review and approval of quantitative models used for deal pricing,

financial statement fair value determination and risk

quantification; a trading product valuation policy that requires

verification of all traded product valuations; and a periodic review

and substantiation of daily profit and loss reporting for all traded

products. Primarily through validation controls, we utilize both

broker and pricing service inputs which can and do include both

market-observable and internally-modeled values and/or valuation

inputs. Our reliance on this information is tempered by the

knowledge of how the broker and/or pricing service develops its

data with a higher degree of reliance applied to those that are

more directly observable and lesser reliance applied to those

developed through their own internal modeling. Similarly, broker

quotes that are executable are given a higher level of reliance than

indicative broker quotes, which are not executable. These

processes and controls are performed independently of the

business.

Trading account assets and liabilities are carried at fair value

based primarily on actively traded markets where prices are from

either direct market quotes or observed transactions. Liquidity is

a significant factor in the determination of the fair value of trading

account assets and liabilities. Market price quotes may not be

readily available for some positions, or positions within a market

sector where trading activity has slowed significantly or ceased.

Situations of illiquidity generally are triggered by market perception

of credit uncertainty regarding a single company or a specific

market sector. In these instances, fair value is determined based

on limited available market information and other factors,

principally from reviewing the issuer’s financial statements and

changes in credit ratings made by one or more of the rating

agencies.

Trading account profits, which represent the net amount earned

from our trading positions, can be volatile and are largely driven

by general market conditions and customer demand. Trading

account profits are dependent on the volume and type of

transactions, the level of risk assumed, and the volatility of price

and rate movements at any given time within the ever-changing

market environment. To evaluate risk in our trading activities, we

focus on the actual and potential volatility of individual positions

as well as portfolios. At a portfolio and corporate level, we use

trading limits, stress testing and tools such as VaR modeling, which

estimates a potential daily loss that we do not expect to exceed

with a specified confidence level, to measure and manage market

risk. For more information on VaR, see Trading Risk Management

on page 107.

The fair values of derivative assets and liabilities traded in the

OTC market are determined using quantitative models that require

the use of multiple market inputs including interest rates, prices

and indices to generate continuous yield or pricing curves and

volatility factors, which are used to value the positions. The majority

of market inputs are actively quoted and can be validated through

external sources including brokers, market transactions and third-

party pricing services. Estimation risk is greater for derivative asset

and liability positions that are either option-based or have longer

maturity dates where observable market inputs are less readily

available or are unobservable, in which case quantitative-based

extrapolations of rate, price or index scenarios are used in

determining fair values. The Corporation incorporates within its

fair value measurements of OTC derivatives a valuation adjustment

to reflect the credit risk associated with the net position. Positions

are netted by counterparty and fair value for net long exposures

is adjusted for counterparty credit risk while the fair value for net

short exposures is adjusted for our own credit risk. The credit

adjustments are determined by reference to existing direct market

reference costs of credit, or where direct references are not

available, a proxy is applied consistent with direct references for

other counterparties that are similar in credit risk. An estimate of

severity of loss is also used in the determination of fair value,

primarily based on market implied experience adjusted for any

more recent name specific expectations.

Level 3 Assets and Liabilities

Financial assets and liabilities whose values are based on

valuation techniques that require inputs that are both

unobservable and are significant to the overall fair value

measurement are classified as Level 3 under the fair value

hierarchy established in applicable accounting guidance. The Level

3 financial assets and liabilities include consumer MSRs, highly

structured, complex or long-dated derivative contracts and private

equity investments, as well as certain loans, MBS, ABS, structured

liabilities and CDOs. The fair value of these Level 3 financial assets

and liabilities is determined using pricing models, discounted cash

flow methodologies or similar techniques for which the

determination of fair value requires significant management

judgment or estimation.