Bank of America 2011 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

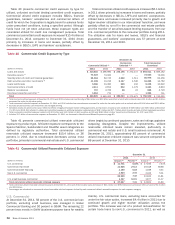

Bank of America 2011 81

In some cases, the junior-lien home equity outstanding balance

that we hold is current, but the underlying first-lien is not. For

outstanding balances in the home equity portfolio in which we

service the first-lien loan, we are able to track whether the first-

lien loan is in default. For loans in which the first-lien is serviced

by a third party, we utilize credit bureau data to estimate the

delinquency status of the first-lien. Given that the credit bureau

database we use does not include a property address for the

mortgages, we are unable to identify with certainty whether a

reported delinquent first mortgage pertains to the same property

for which we hold a second- or more junior-lien loan. As of

December 31, 2011, we estimate that $4.7 billion of current

second- or more junior-lien loans were behind a delinquent first-

lien loan. We service the first-lien loans on $1.3 billion of that

amount, with the remaining $3.4 billion serviced by third parties.

Of the $4.7 billion current second-lien loans, we estimate based

on available credit bureau data as discussed above that

approximately $2.5 billion had first-lien loans that were 120 days

or more past due, of which approximately $2.1 billion had first-

lien loans serviced by third parties.

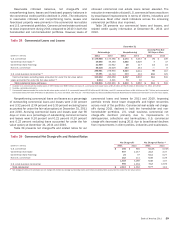

Net charge-offs decreased $2.3 billion to $4.5 billion, or 3.77

percent of the total average home equity portfolio, for 2011

compared to $6.8 billion, or 5.10 percent, for 2010 primarily driven

by favorable portfolio trends due in part to improvement in the

U.S. economy. In addition, the net charge-off amounts during 2010

were impacted by the implementation of regulatory guidance on

collateral-dependent modified loans which resulted in

$822 million in net charge-offs. Net charge-off ratios were further

impacted by lower outstanding balances primarily as a result of

paydowns and charge-offs outpacing new originations and draws

on existing lines.

There are certain characteristics of the outstanding loan

balances in the home equity portfolio that have contributed to

higher losses including those loans with a high refreshed combined

loan-to-value (CLTV), loans that were originated at the peak of home

prices in 2006 and 2007 and loans in geographic areas that have

experienced the most significant declines in home prices. Home

price declines coupled with the fact that most home equity

outstandings are secured by second-lien positions have

significantly reduced and, in some cases, eliminated all collateral

value after consideration of the first-lien position. Although the

disclosures below address each of these risk characteristics

separately, there is significant overlap in outstanding balances

with these characteristics, which has contributed to a

disproportionate share of losses in the portfolio. Outstanding

balances in the home equity portfolio with all of these higher risk

characteristics comprised 10 percent of the total home equity

portfolio at both December 31, 2011 and 2010, but have

accounted for 28 percent of the home equity net charge-offs in

2011 and 29 percent in 2010.

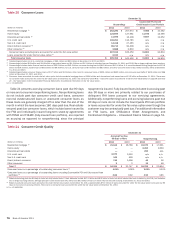

Outstanding balances in the home equity portfolio with greater

than 90 percent but less than 100 percent refreshed CLTVs

comprised 11 percent of the home equity portfolio at both

December 31, 2011 and 2010. Outstanding balances with

refreshed CLTVs greater than 100 percent comprised 32 percent

and 30 percent of the home equity portfolio at December 31, 2011

and 2010. Outstanding balances in the home equity portfolio with

a refreshed CLTV greater than 100 percent reflect loans where the

carrying value and available line of credit of the combined loans

are equal to or greater than the most recent valuation of the

property securing the loan. Depending on the value of the property,

there may be collateral in excess of the first-lien that is available

to reduce the severity of loss on the second-lien. Home price

deterioration over the past several years has contributed to an

increase in CLTV ratios. Of those outstanding balances with a

refreshed CLTV greater than 100 percent, 95 percent of the

customers were current at December 31, 2011. For second-lien

loans with a refreshed CLTV greater than 100 percent that are

current, 89 percent were also current on the underlying first-lien

loans at December 31, 2011. Outstanding balances in the home

equity portfolio to borrowers with a refreshed FICO score below

620 represented 12 percent of the home equity portfolio at both

December 31, 2011 and 2010.

Of the $112.7 billion in total home equity portfolio

outstandings, 78 percent and 75 percent at December 31, 2011

and 2010 were originated as interest-only loans, almost all of

which were HELOCs. The outstanding balance of HELOCs that have

entered the amortization period was $1.6 billion, or two percent

of total HELOCs, at December 31, 2011. The HELOCs that have

entered the amortization period have experienced a higher

percentage of early stage delinquencies and nonperforming status

when compared to the HELOC portfolio as a whole. As of

December 31, 2011, $49 million, or three percent, of outstanding

HELOCs that had entered the amortization period were accruing

past due 30 days or more compared to $1.4 billion, or one percent,

of outstanding accruing past due 30 days or more for the entire

HELOC portfolio. In addition, at December 31, 2011, $57 million,

or four percent, of outstanding HELOCs that had entered the

amortization period were nonperforming compared to $2.0 billion,

or two percent, of outstandings that were nonperforming for the

entire HELOC portfolio. Loans in our HELOC portfolio generally

have an initial draw period of 10 years and more than 85 percent

of these loans will not be required to make a fully-amortizing

payment until 2015 or later.

Although we do not actively track how many of our home equity

customers pay only the minimum amount due on their home equity

loans and lines, we can infer some of this information through a

review of our HELOC portfolio that we service and that is still in

its revolving period (i.e., customers may draw on and repay their

line of credit, but are generally only required to pay interest on a

monthly basis). During 2011, approximately 51 percent of these

customers did not pay down any principal on their HELOCs.