Bank of America 2011 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 27

These decreases were partially offset by ongoing reductions in our

debt footprint and lower interest rates paid on deposits. The net

interest yield on a FTE basis decreased 30 bps to 2.48 percent

for 2011 compared to 2010 as the yield continues to be under

pressure due to the aforementioned items and the low rate

environment. We expect net interest income to continue to be

muted based on the current forward yield curve in 2012.

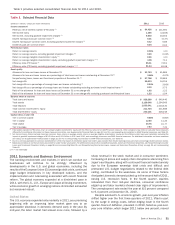

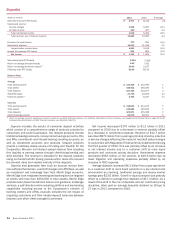

Noninterest Income

Table 4

(Dollars in millions)

Card income

Service charges

Investment and brokerage services

Investment banking income

Equity investment income

Trading account profits

Mortgage banking income (loss)

Insurance income

Gains on sales of debt securities

Other income

Net impairment losses recognized in earnings on

available-for-sale debt securities

Total noninterest income

Noninterest Income

2011

$ 7,184

8,094

11,826

5,217

7,360

6,697

(8,830)

1,346

3,374

6,869

(299)

$ 48,838

2010

$ 8,108

9,390

11,622

5,520

5,260

10,054

2,734

2,066

2,526

2,384

(967)

$ 58,697

Noninterest income decreased $9.9 billion to $48.8 billion for

2011 compared to 2010. The following highlights the significant

changes.

Card income decreased $924 million primarily due to the

implementation of new interchange fee rules under the Durbin

Amendment, which became effective on October 1, 2011 and

the CARD Act provisions that were implemented during 2010.

Service charges decreased $1.3 billion largely due to the impact

of overdraft policy changes in conjunction with Regulation E,

which became effective in the third quarter of 2010.

Equity investment income increased $2.1 billion. The results for

2011 included $6.5 billion of gains on the sale of CCB shares,

$836 million of CCB dividends and a $377 million gain on the

sale of our investment in BlackRock, Inc. (BlackRock), partially

offset by $1.1 billion of impairment charges on our merchant

services joint venture. The prior year included $2.5 billion of net

gains which included the sales of certain strategic investments,

$2.3 billion of gains in our Global Principal Investments (GPI)

portfolio which included both cash gains and fair value

adjustments, and $535 million of CCB dividends.

Trading account profits decreased $3.4 billion primarily due to

adverse market conditions and extreme volatility in the credit

markets compared to the prior year. DVA gains, net of hedges,

on derivatives were $1.0 billion in 2011 compared to $262

million in 2010 as a result of a widening of our credit spreads.

In conjunction with regulatory reform measures GBAM exited its

stand-alone proprietary trading business as of June 30, 2011.

Proprietary trading revenue was $434 million for the six months

ended June 30, 2011 compared to $1.4 billion for 2010.

Mortgage banking income decreased $11.6 billion primarily due

to an $8.8 billion increase in the representations and warranties

provision which was largely related to the BNY Mellon

Settlement. Also contributing to the decline was lower

production income due to a reduction in new loan origination

volumes partially offset by an increase in servicing income.

Other income increased $4.5 billion primarily due to positive

fair value adjustments of $3.3 billion related to widening of our

own credit spreads on structured liabilities compared to $18

million in 2010. In addition, 2011 included a $771 million gain

on the sale of Balboa as well as a $1.2 billion gain on the

exchange of certain trust preferred securities for common stock

and debt.

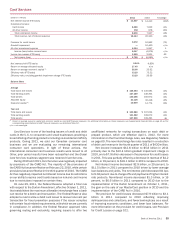

Provision for Credit Losses

The provision for credit losses decreased $15.0 billion to $13.4

billion for 2011 compared to 2010. The provision for credit losses

was $7.4 billion lower than net charge-offs for 2011, resulting in

a reduction in the allowance for credit losses driven primarily by

lower delinquencies, improved collection rates and fewer

bankruptcy filings across the Card Services portfolio, and

improvement in overall credit quality in the commercial real estate

portfolio partially offset by additions to consumer PCI loan portfolio

reserves. This compared to a $5.9 billion reduction in the

allowance for credit losses in 2010. We expect reductions in the

allowance for credit losses to be lower in 2012.

The provision for credit losses related to our consumer portfolio

decreased $11.1 billion to $14.3 billion for 2011 compared to

2010. The provision for credit losses related to our commercial

portfolio including the provision for unfunded lending commitments

decreased $3.9 billion to a benefit of $915 million for 2011

compared to 2010.

Net charge-offs totaled $20.8 billion, or 2.24 percent of average

loans and leases for 2011 compared to $34.3 billion, or 3.60

percent for 2010. The decrease in net charge-offs was primarily

driven by improvements in general economic conditions that

resulted in lower delinquencies, improved collection rates and

fewer bankruptcy filings across the Card Services portfolio as well

as lower losses in the home equity portfolio driven primarily by

fewer delinquent loans. For more information on the provision for

credit losses, see Provision for Credit Losses on page 102.

Noninterest Expense

Table 5

(Dollars in millions)

Personnel

Occupancy

Equipment

Marketing

Professional fees

Amortization of intangibles

Data processing

Telecommunications

Other general operating

Goodwill impairment

Merger and restructuring charges

Total noninterest expense

Noninterest Expense

2011

$ 36,965

4,748

2,340

2,203

3,381

1,509

2,652

1,553

21,101

3,184

638

$ 80,274

2010

$ 35,149

4,716

2,452

1,963

2,695

1,731

2,544

1,416

16,222

12,400

1,820

$ 83,108

Noninterest expense decreased $2.8 billion to $80.3 billion

for 2011 compared to 2010. The prior year included goodwill

impairment charges of $12.4 billion compared to $3.2 billion for

2011.

Personnel expense increased $1.8 billion for 2011 attributable

to personnel costs related to the continued build-out of certain

businesses, technology costs as well as increases in default-