Bank of America 2011 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 65

Our Board’s Audit, Credit and Enterprise Risk Committees have

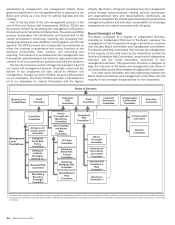

the principal responsibility for assisting the Board with enterprise-

wide oversight of the Corporation’s management and handling of

risk.

Our Audit Committee assists the Board in the oversight of,

among other things, the integrity of our consolidated financial

statements, our compliance with legal and regulatory

requirements, and the overall effectiveness of our system of

internal controls. Our Audit Committee also, taking into

consideration the Board’s allocation of the review of risk among

various committees of the Board, discusses with management

guidelines and policies to govern the process by which risk

assessment and risk management are undertaken, including the

assessment of our major financial risk exposures and the steps

management has taken to monitor and control such exposures.

Our Credit Committee oversees, among other things, the

identification and management of our credit exposures on an

enterprise-wide basis, our responses to trends affecting those

exposures, the adequacy of the allowance for credit losses and

our credit related policies.

Our Enterprise Risk Committee, among other things, oversees

our identification of, management of and planning for, material

risks on an enterprise-wide basis, including market risk, interest

rate risk, liquidity risk, operational risk and reputational risk. Our

Enterprise Risk Committee also oversees our capital management

and liquidity planning.

Each of these committees regularly reports to our Board on

risk-related matters within the committee’s responsibilities, which

collectively provides our Board with integrated, thorough insight

about our management of our enterprise-wide risks. At meetings

of our Audit, Credit and Enterprise Risk Committees and our Board,

directors receive updates from management regarding enterprise

risk management, including our performance against our risk

appetite.

Executive management develops for Board approval the

Corporation’s Risk Framework, Risk Appetite Statement, and

financial operating plans. Management monitors, and the Board

oversees, through the Credit, Enterprise Risk and Audit

Committees, financial performance, execution of the strategic and

financial operating plans, compliance with the risk appetite, and

the adequacy of internal controls.

Strategic Risk Management

Strategic risk is embedded in every business and is one of the

major risk categories along with credit, market, liquidity,

compliance, operational and reputational risks. It is the risk that

results from adverse business decisions, ineffective or

inappropriate business plans, or failure to respond to changes in

the competitive environment, business cycles, customer

preferences, product obsolescence, regulatory environment,

business strategy execution and/or other inherent risks of the

business including reputational and operational risk. In the

financial services industry, strategic risk is elevated due to

changing customer, competitive and regulatory environments. Our

appetite for strategic risk is assessed within the context of the

strategic plan, with strategic risks selectively and carefully

considered in the context of the evolving marketplace. Strategic

risk is managed in the context of our overall financial condition

and assessed, managed and acted on by the CEO and executive

management team. Significant strategic actions, such as material

acquisitions or capital actions, require review and approval of the

Board.

Executive management approves a strategic plan every two to

three years. Annually, executive management develops a financial

operating plan that implements the strategic goals for that year,

and the Board reviews and approves the plan. With oversight by

the Board, executive management ensures that the plans are

consistent with the Corporation’s strategic plan, core operating

tenets and risk appetite. The following are assessed in their

reviews: forecasted earnings and returns on capital, the current

risk profile, current capital and liquidity requirements, staffing

levels and changes required to support the plan, stress testing

results, and other qualitative factors such as market growth rates

and peer analysis. At the business level, as we introduce new

products, we monitor their performance to evaluate expectations

(e.g., for earnings and returns on capital). With oversight by the

Board, executive management performs similar analyses

throughout the year, and evaluates changes to the financial

forecast or the risk, capital or liquidity positions as deemed

appropriate to balance and optimize between achieving the

targeted risk appetite, shareholder returns and maintaining the

targeted financial strength.

We use proprietary models to measure the capital requirements

for credit, country, market, operational and strategic risks. The

economic capital assigned to each business is based on its unique

risk exposures. With oversight by the Board, executive

management assesses the risk-adjusted returns of each business

in approving strategic and financial operating plans. The

businesses use economic capital to define business strategies,

price products and transactions, and evaluate client profitability.

For additional information on how this measure is calculated, see

Supplemental Financial Data on page 32.

Capital Management

Bank of America manages its capital position to ensure capital is

sufficient to support our business activities and that capital, risk

and risk appetite are commensurate with one another, ensure

safety and soundness under adverse scenarios, take advantage

of growth and strategic opportunities, maintain ready access to

financial markets, remain a source of strength for its subsidiaries

and satisfy current and future regulatory capital requirements.

To determine the appropriate level of capital, we assess the

results of our Internal Capital Adequacy Assessment Process

(ICAAP), the current economic and market environment, and

feedback from investors, rating agencies and regulators. Based

upon this analysis we set capital guidelines for Tier 1 common

capital and Tier 1 capital to ensure we can maintain an adequate

capital position in a severe adverse economic scenario. We also

target to maintain capital in excess of the capital required per our

economic capital measurement process. For additional

information, see Economic Capital on page 69. Management and

the Board annually approve a comprehensive Capital Plan which

documents the ICAAP and related results, analysis and support

for the capital guidelines, and planned capital actions and capital

adequacy assessment.