Bank of America 2011 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

90 Bank of America 2011

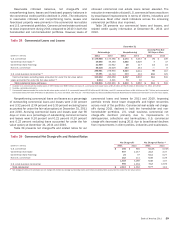

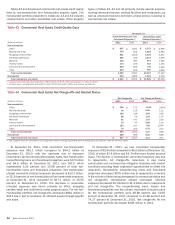

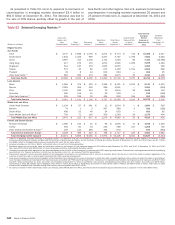

Table 40 presents commercial credit exposure by type for

utilized, unfunded and total binding committed credit exposure.

Commercial utilized credit exposure includes SBLCs, financial

guarantees, bankers’ acceptances and commercial letters of

credit for which the Corporation is legally bound to advance funds

under prescribed conditions, during a specified period. Although

funds have not yet been advanced, these exposure types are

considered utilized for credit risk management purposes. Total

commercial committed credit exposure increased $10.4 billion at

December 31, 2011 compared to December 31, 2010 driven

primarily by increases in loans and leases, partially offset by

decreases in SBLCs, LHFS and bankers’ acceptances.

Total commercial utilized credit exposure increased $6.1 billion

in 2011 driven primarily by increases in loans and leases, partially

offset by decreases in SBLCs, LHFS and bankers’ acceptances.

Utilized loans and leases increased primarily due to growth and

higher revolver utilization in our international franchise, and were

partially offset by run-off in the commercial real estate portfolio

and the transfer of securities-based lending exposures from our

U.S. commercial portfolio to the consumer portfolio during 2011.

The utilization rate for loans and leases, SBLCs and financial

guarantees, and bankers’ acceptances was 57 percent at both

December 31, 2011 and 2010.

Table 40

(Dollars in millions)

Loans and leases

Derivative assets (4)

Standby letters of credit and financial guarantees

Debt securities and other investments (5)

Loans held-for-sale

Commercial letters of credit

Bankers’ acceptances

Foreclosed properties and other (6)

Total

Commercial Credit Exposure by Type

December 31

Commercial Utilized (1)

2011

$ 316,816

73,023

55,384

11,108

5,006

2,411

797

1,964

$ 466,509

2010

$296,990

73,000

62,745

10,216

10,380

2,654

3,706

731

$460,422

Commercial

Unfunded (2, 3)

2011

$ 276,195

—

1,592

5,147

229

832

28

—

$ 284,023

2010

$272,172

—

1,511

4,546

242

1,179

23

—

$279,673

Total Commercial

Committed

2011

$ 593,011

73,023

56,976

16,255

5,235

3,243

825

1,964

$ 750,532

2010

$ 569,162

73,000

64,256

14,762

10,622

3,833

3,729

731

$ 740,095

(1) Total commercial utilized exposure at December 31, 2011 and 2010 includes loans outstanding of $6.6 billion and $3.3 billion and letters of credit with a notional value of $1.3 billion and $1.4 billion

accounted for under the fair value option.

(2) Total commercial unfunded exposure at December 31, 2011 and 2010 includes loan commitments accounted for under the fair value option with a notional value of $24.4 billion and $25.9 billion.

(3) Excludes unused business card lines which are not legally binding.

(4) Derivative assets are carried at fair value, reflect the effects of legally enforceable master netting agreements and have been reduced by cash collateral of $58.9 billion and $58.3 billion at December

31, 2011 and 2010. Not reflected in utilized and committed exposure is additional derivative collateral held of $16.1 billion and $17.7 billion which consists primarily of other marketable securities.

(5) Total commercial committed exposure consists of $16.3 billion and $14.2 billion of debt securities and $0 and $590 million of other investments at December 31, 2011 and 2010.

(6) Includes $1.3 billion of net monoline exposure at December 31, 2011, as discussed in Monoline and Related Exposure on page 95.

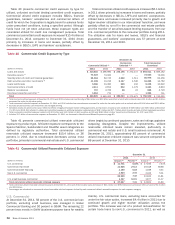

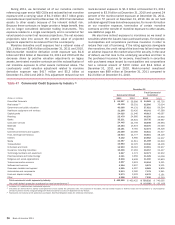

Table 41 presents commercial utilized reservable criticized

exposure by product type. Criticized exposure corresponds to the

Special Mention, Substandard and Doubtful asset categories as

defined by regulatory authorities. Total commercial utilized

reservable criticized exposure decreased $15.4 billion, or 36

percent, in 2011 due to broad-based decreases across most

portfolios, primarily in commercial real estate and U.S. commercial

driven largely by continued paydowns, sales and ratings upgrades

outpacing downgrades. Despite the improvements, utilized

reservable criticized levels remain elevated, particularly in

commercial real estate and U.S. small business commercial. At

December 31, 2011, approximately 85 percent of commercial

utilized reservable criticized exposure was secured compared to

88 percent at December 31, 2010.

Table 41

(Dollars in millions)

U.S. commercial

Commercial real estate

Commercial lease financing

Non-U.S. commercial

U.S. small business commercial

Total commercial utilized reservable criticized exposure

Commercial Utilized Reservable Criticized Exposure

December 31

2011

Amount (1)

$ 11,731

11,525

1,140

1,524

25,920

1,327

$ 27,247

Percent (2)

5.16%

27.13

5.18

2.44

7.32

10.01

7.41

2010

Amount (1)

$ 17,195

20,518

1,188

2,043

40,944

1,677

$ 42,621

Percent (2)

7.44%

38.88

5.41

5.01

11.81

11.37

11.80

(1) Total commercial utilized reservable criticized exposure at December 31, 2011 and 2010 includes loans and leases of $25.3 billion and $39.8 billion and commercial letters of credit of $1.9 billion

and $2.8 billion.

(2) Percentages are calculated as commercial utilized reservable criticized exposure divided by total commercial utilized reservable exposure for each exposure category.

U.S. Commercial

At December 31, 2011, 58 percent of the U.S. commercial loan

portfolio, excluding small business, was managed in Global

Commercial Banking and 30 percent in GBAM. The remaining 12

percent was mostly in GWIM (business-purpose loans for wealthy

clients). U.S. commercial loans, excluding loans accounted for

under the fair value option, increased $4.4 billion in 2011 due to

continued growth and higher revolver utilization across the

portfolio. This increase was net of a product reclassification for

certain trade loans to non-U.S. commercial in 2011, as well as