Bank of America 2011 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

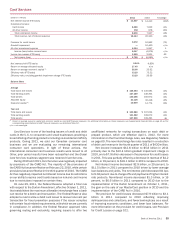

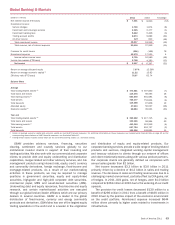

34 Bank of America 2011

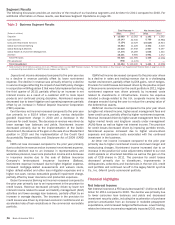

Deposits

(Dollars in millions)

Net interest income (FTE basis)

Noninterest income:

Service charges

All other income

Total noninterest income

Total revenue, net of interest expense

Provision for credit losses

Noninterest expense

Income before income taxes

Income tax expense (FTE basis)

Net income

Net interest yield (FTE basis)

Return on average allocated equity

Return on average economic capital (1)

Efficiency ratio (FTE basis)

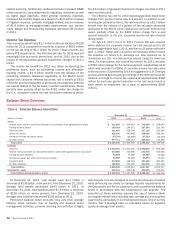

Balance Sheet

Average

Total earning assets

Total assets

Total deposits

Allocated equity

Economic capital (1)

Year end

Total earning assets

Total assets

Total deposits

Client brokerage assets

2011

$ 8,471

3,995

223

4,218

12,689

173

10,633

1,883

691

$ 1,192

2.02%

5.02

20.66

83.80

$ 419,445

445,922

421,106

23,735

5,786

$ 418,623

445,680

421,871

66,576

2010

$ 8,278

5,057

227

5,284

13,562

201

11,196

2,165

803

$ 1,362

2.00%

5.62

21.97

82.55

$ 413,595

440,030

414,877

24,222

6,247

$ 414,215

440,954

415,189

63,597

% Change

2%

(21)

(2)

(20)

(6)

(14)

(5)

(13)

(14)

(12)

1

1

2

(2)

(7)

1

1

2

5

(1) Return on average economic capital and economic capital are non-GAAP financial measures. For additional information on these measures, see Supplemental Financial Data on page 32 and for

corresponding reconciliations to GAAP financial measures, see Statistical Table XVI.

Deposits includes the results of consumer deposit activities

which consist of a comprehensive range of products provided to

consumers and small businesses. Our deposit products include

traditional savings accounts, money market savings accounts, CDs

and IRAs, noninterest- and interest-bearing checking accounts, as

well as investment accounts and products. Deposit products

provide a relatively stable source of funding and liquidity for the

Corporation. We earn net interest spread revenue from investing

this liquidity in earning assets through client-facing lending and

ALM activities. The revenue is allocated to the deposit products

using our funds transfer pricing process which takes into account

the interest rates and implied maturity of the deposits.

Deposits also generates fees such as account service fees,

non-sufficient funds fees, overdraft charges and ATM fees, as well

as investment and brokerage fees from Merrill Edge accounts.

Merrill Edge is an integrated investing and banking service targeted

at clients with less than $250,000 in total assets. Merrill Edge

provides team-based investment advice and guidance, brokerage

services, a self-directed online investing platform and key banking

capabilities including access to the Corporation’s network of

banking centers and ATMs. Deposits includes the net impact of

migrating customers and their related deposit balances between

Deposits and other client-managed businesses.

Net income decreased $170 million to $1.2 billion in 2011

compared to 2010 due to a decrease in revenue partially offset

by a decrease in noninterest expense. Revenue of $12.7 billion

was down $873 million from a year ago primarily driven by a decline

in service charges reflecting the impact of overdraft policy changes

in conjunction with Regulation E that were fully implemented during

the third quarter of 2010. This was partially offset by an increase

in net interest income due to a customer shift to more liquid

products and continued pricing discipline. Noninterest expense

decreased $563 million, or five percent, to $10.6 billion due to

lower litigation and operating expenses partially offset by an

increase in FDIC expense.

Average deposits increased $6.2 billion from a year ago driven

by a customer shift to more liquid products in a low interest rate

environment as checking, traditional savings and money market

savings grew $23.6 billion. Growth in liquid products was partially

offset by a decline in average time deposits of $17.4 billion. As a

result of the shift in the mix of deposits and our continued pricing

discipline, rates paid on average deposits declined by 16 bps to

27 bps in 2011 compared to 2010.