Bank of America 2011 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

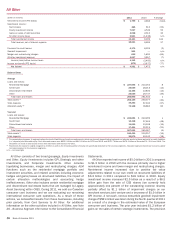

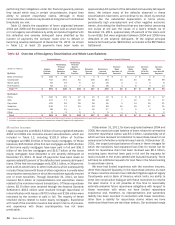

58 Bank of America 2011

has been much slower than in non-judicial states. The pace of

foreclosure sales in judicial states increased significantly by the

fourth quarter of 2011. However, there continues to be a backlog

of foreclosure inventory in judicial states. The implementation of

changes in procedures and controls, including loss mitigation

procedures related to our ability to recover on FHA-insurance

related claims, and governmental, regulatory and judicial actions,

may result in continuing delays in foreclosure proceedings and

foreclosure sales, and create obstacles to the collection of certain

fees and expenses, in both judicial and non-judicial foreclosures.

We entered into a consent order with the Federal Reserve and

BANA entered into a consent order with the OCC on April 13, 2011.

These consent orders require servicers to make several

enhancements to their servicing operations, including

implementation of a single point of contact model for borrowers

throughout the loss mitigation and foreclosure processes,

adoption of measures designed to ensure that foreclosure activity

is halted once a borrower has been approved for a modification

unless the borrower fails to make payments under the modified

loan and implementation of enhanced controls over third-party

vendors that provide default servicing support services. In

addition, the OCC consent order required that we retain an

independent consultant, approved by the OCC, to conduct a review

of all foreclosure actions pending, or foreclosure sales that

occurred, between January 1, 2009 and December 31, 2010 and

submit a plan to the OCC to remediate all financial injury to

borrowers caused by any deficiencies identified through the review.

The review is comprised of two parts: a sample file review

conducted by the independent consultant, which began in October

2011, and file reviews by the independent consultant based upon

requests for review from customers with in-scope foreclosures.

We began outreach to those customers in November 2011, and

additional outreach efforts are underway. Because the review

process is available to a large number of potentially eligible

borrowers and involves an examination of many details and

documents, each review could take several months to complete.

We cannot yet accurately determine how many borrowers will

ultimately request a review, how many borrowers will meet the

eligibility requirements or how much in compensation might

ultimately be paid to eligible borrowers.

We continue to be subject to additional borrower and non-

borrower litigation and governmental and regulatory scrutiny

related to our past and current servicing and foreclosure activities,

including those claims not covered by the Servicing Resolution

Agreements, defined below. This scrutiny may extend beyond our

pending foreclosure matters to issues arising out of alleged

irregularities with respect to previously completed foreclosure

activities. The current environment of heightened regulatory

scrutiny may subject us to inquiries or investigations that could

significantly adversely affect our reputation and result in material

costs to us.

Servicing Resolution Agreements

On February 9, 2012, we reached agreements in principle

(collectively, the Servicing Resolution Agreements) with (1) the

DOJ, various federal regulatory agencies and 49 state attorneys

general to resolve federal and state investigations into certain

origination, servicing and foreclosure practices (the Global AIP),

(2) the Federal Housing Administration (the FHA) to resolve certain

claims relating to the origination of FHA-insured mortgage loans,

primarily by Countrywide prior to and for a period following our

acquisition of that lender (the FHA AIP) and (3) each of the Federal

Reserve and the OCC regarding civil monetary penalties related

to conduct that was the subject of consent orders entered into

with the banking regulators in April 2011 (the Consent Order AIPs).

The Servicing Resolution Agreements are subject to ongoing

discussions among the parties and completion and execution of

definitive documentation, as well as required regulatory and court

approvals. There can be no assurance as to when or whether

binding settlement agreements will be reached, that they will be

on terms consistent with the Servicing Resolution Agreements, or

as to when or whether the necessary approvals will be obtained

and the settlements will be finalized.

The Global AIP calls for the establishment of certain uniform

servicing standards, upfront cash payments of approximately $1.9

billion to the state and federal governments and for borrower

restitution, approximately $7.6 billion in borrower assistance in

the form of, among other things, principal reduction, short sales,

deeds-in-lieu of foreclosure, and approximately $1.0 billion in

refinancing assistance. We could be required to make additional

payments if we fail to meet our borrower assistance and refinancing

assistance commitments over a three-year period. In addition, we

could be required to pay an additional $350 million if we fail to

meet certain first-lien principal reduction thresholds over a three-

year period. We also entered into agreements with several states

under which we committed to perform certain minimum levels of

principal reduction and related activities within those states as

part of the Global AIP, and under which we could be required to

make additional payments if we fail to meet such minimum levels.

The FHA AIP provides for an upfront cash payment of $500

million and the FHA would release us from all claims arising from

loans originated on or before April 30, 2009 that were submitted

for FHA insurance claim payments prior to January 1, 2012, and

from multiple damages and penalties for loans that were originated

on or before April 30, 2009, but had not been submitted for FHA

insurance claim payment. An additional $500 million would be

payable if we fail to meet certain principal reduction thresholds

over a three-year period.

Pursuant to an agreement in principle, the OCC agreed to hold

in abeyance the imposition of a civil monetary penalty of $164

million. Pursuant to a separate agreement in principle, the Federal

Reserve will assess a civil monetary penalty in the amount of $176

million against us. Satisfying our payment, borrower assistance

and remediation obligations under the Global AIP will satisfy any

civil monetary penalty obligations arising under these agreements

in principle. If, however, we do not make certain required payments

or undertake certain required actions under the Global AIP, the OCC

will assess, and the Federal Reserve will require us to pay, the

difference between the aggregate value of the payments and

actions under these agreements in principle and the penalty

amounts.

Under the terms of the Global AIP, the federal and participating

state governments would release us from further liability for certain

alleged residential mortgage origination, servicing and foreclosure

deficiencies. In settling origination issues related to FHA

guaranteed loans originated on or before April 30, 2009, the FHA

would provide us and our affiliates a release for all claims with

respect to such loans if an insurance claim had been submitted

to the FHA prior to January 1, 2012 and a release of multiple

damages and penalties (but not single damages) if no such claim

had been submitted.

The financial impact of the Servicing Resolution Agreements

is not expected to require any additional reserves over existing

accruals as of December 31, 2011, based on our understanding