Bank of America 2011 Annual Report Download - page 265

Download and view the complete annual report

Please find page 265 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

|

|

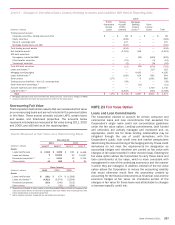

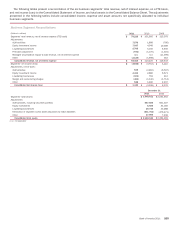

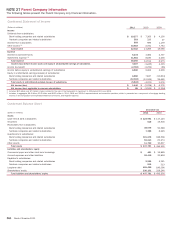

Bank of America 2011 263

firms and governments, and are generally defined as companies

with sales up to $2 billion. Lending products and services include

commercial loans and commitment facilities, real estate lending,

asset-based lending and indirect consumer loans. Capital

management and treasury solutions include treasury

management, foreign exchange and short-term investing options.

In 2011, management responsibility for the merchant services

joint venture was moved from GBAM to Global Commercial Banking.

Prior periods have been reclassified to reflect the change.

Global Banking & Markets

GBAM provides advisory services, financing, securities clearing,

settlement and custody services globally to institutional investor

clients in support of their investing and trading activities. GBAM

also works with commercial and corporate clients to provide debt

and equity underwriting and distribution capabilities, merger-

related and other advisory services, and risk management

products using interest rate, equity, credit, currency and commodity

derivatives, foreign exchange, fixed-income and mortgage-related

products. As a result of the Corporation’s market-making activities

in these products, it may be required to manage positions in

government securities, equity and equity-linked securities, high-

grade and high-yield corporate debt securities, commercial paper,

MBS and ABS. Corporate banking services provide a wide range

of lending-related products and services, integrated working

capital management and treasury solutions to clients through the

Corporation’s network of offices and client relationship teams

along with various product partners. Corporate clients are generally

defined as companies with annual sales greater than $2 billion.

Global Wealth & Investment Management

GWIM provides comprehensive wealth management capabilities

to a broad base of clients from emerging affluent to the ultra-high-

net-worth. These services include investment and brokerage

services, estate and financial planning, fiduciary portfolio

management, cash and liability management and specialty asset

management. GWIM also provides retirement and benefit plan

services, philanthropic management and asset management to

individual and institutional clients. GWIM results are impacted by

the migration of clients and their related deposit and loan balances

to or from Deposits, CRES and the ALM portfolio. Migration in the

current year includes the additional movement of balances to

Merrill Edge, which is in Deposits. Subsequent to the date of

migration, the associated net interest income, noninterest income

and noninterest expense are recorded in the business to which

the clients migrated.

All Other

All Other consists of equity investment activities including Global

Principal Investments, Strategic and other investments, and

Corporate Investments. All Other also includes liquidating

businesses, merger and restructuring charges, ALM functions such

as residential mortgage portfolio and investment securities and

related activities, including economic hedges and gains/losses on

structured liabilities, the impact of certain allocation

methodologies and accounting hedge ineffectiveness. Additionally,

All Other includes certain residential mortgage and discontinued

real estate loans that are managed by CRES. During 2011, the

Corporation sold its Canadian consumer card business and is

evaluating its remaining international consumer card operations.

As a result of these actions, the international consumer card

business results were moved to All Other from Card Services and

prior periods have been reclassified.

Basis of Presentation

The management accounting and reporting process derives

segment and business results by utilizing allocation

methodologies for revenue and expense. The net income derived

for the businesses is dependent upon revenue and cost allocations

using an activity-based costing model, funds transfer pricing, and

other methodologies and assumptions management believes are

appropriate to reflect the results of the business.

Total revenue, net of interest expense, includes net interest

income on a fully taxable-equivalent (FTE) basis and noninterest

income. The adjustment of net interest income to a FTE basis

results in a corresponding increase in income tax expense. The

segment results also reflect certain revenue and expense

methodologies that are utilized to determine net income. The net

interest income of the businesses includes the results of a funds

transfer pricing process that matches assets and liabilities with

similar interest rate sensitivity and maturity characteristics. For

presentation purposes, in segments where the total of liabilities

and equity exceeds assets, which are generally deposit-taking

segments, the Corporation allocates assets to match liabilities.

Net interest income of the business segments also includes an

allocation of net interest income generated by the Corporation’s

ALM activities.

The Corporation’s ALM activities include an overall interest rate

risk management strategy that incorporates the use of interest

rate contracts to manage fluctuations in earnings that are caused

by interest rate volatility. The Corporation’s goal is to manage

interest rate sensitivity so that movements in interest rates do not

significantly adversely affect earnings and capital. The majority of

the Corporation’s ALM activities are allocated to the business

segments and fluctuate based on performance. ALM activities

include external product pricing decisions including deposit pricing

strategies, the effects of the Corporation’s internal funds transfer

pricing process and the net effects of other ALM activities.

Certain expenses not directly attributable to a specific

business segment are allocated to the segments. The most

significant of these expenses include data and item processing

costs and certain centralized or shared functions. Data processing

costs are allocated to the segments based on equipment usage.

Item processing costs are allocated to the segments based on

the volume of items processed for each segment. The costs of

certain centralized or shared functions are allocated based on

methodologies that reflect utilization.