Bank of America 2011 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 55

The GSEs’ repurchase requests, standards for rescission of

repurchase requests and resolution processes have become

increasingly inconsistent with their past conduct as well as our

interpretation of our contractual obligations. Notably, in recent

periods we have been experiencing elevated levels of new claims

from the GSEs, including claims on loans on which borrowers have

made a significant number of payments (e.g., at least 25

payments) or on loans which had defaulted more than 18 months

prior to the repurchase request, in each case, in numbers that

were not expected based on historical experience. Also, the criteria

and the processes by which the GSEs are ultimately willing to

resolve claims have changed in ways that are unfavorable to us.

These developments have resulted in an increase in claims

outstanding from the GSEs. We intend to repurchase loans to the

extent required under the contracts and standards that govern our

relationships with the GSEs. While we are seeking to resolve our

differences with the GSEs concerning each party’s interpretation

of the requirements of the governing contracts, whether we will be

able to achieve a resolution of these differences on acceptable

terms and timing thereof, is subject to significant uncertainty.

Beginning in February 2012, we are no longer delivering

purchase money and non-MHA refinance first-lien residential

mortgage products into FNMA MBS pools because of the expiration

and mutual non-renewal of certain contractual delivery

commitments and variances that permit efficient delivery of such

loans to FNMA. While we continue to have a valid agreement with

FNMA permitting the delivery of purchase money and non-MHA

refinance first-lien residential mortgage products without such

contractual variances, the delivery of such products without

contractual delivery commitments and variances would involve

time and expense to implement the necessary operational and

systems changes and otherwise present practical operational

issues. The non-renewal of these variances was influenced, in part,

by our ongoing differences with FNMA in other contexts, including

repurchase claims. We do not expect this change to have a material

impact on our CRES business, as we expect to rely on other sources

of liquidity to actively extend mortgage credit to our customers

including continuing to deliver such products into FHLMC MBS

pools. Additionally, we continue to deliver MHA refinancing

products into FNMA MBS pools and continue to engage in dialogue

to attempt to address these differences.

On June 30, 2011, FNMA issued an announcement requiring

servicers to report, effective October 1, 2011, all MI rescission

notices with respect to loans sold to FNMA. The announcement

also confirmed FNMA’s view of its position that a mortgage

insurance company’s issuance of a MI rescission notice

constitutes a breach of the lender’s representations and

warranties and permits FNMA to require the lender to repurchase

the mortgage loan or promptly remit a make-whole payment

covering FNMA’s loss even if the lender is contesting the MI

rescission notice. A related announcement included a ban on bulk

settlements with mortgage insurers that provide for loss sharing

in lieu of rescission. According to FNMA’s announcement, through

June 30, 2012, lenders have 90 days to appeal FNMA’s repurchase

request and 30 days (or such other time frame specified by FNMA)

to appeal after that date. According to FNMA’s announcement, in

order to be successful in its appeal, a lender must provide

documentation confirming reinstatement or continuation of

coverage. This announcement could result in more repurchase

requests from FNMA than the assumptions in our estimated

liability contemplate. We also expect that in many cases

(particularly in the context of individual or bulk rescissions being

contested through litigation), we will not be able to resolve MI

rescission notices with the mortgage insurance companies before

the expiration of the appeal period prescribed by the FNMA

announcement. We have informed FNMA that we do not believe

that the new policy is valid under our contracts with FNMA, and

that we do not intend to repurchase loans under the terms set

forth in the new policy. Our pipeline of outstanding repurchase

claims from the GSEs resulting solely on MI rescission notices

has increased during 2011 by $935 million to $1.2 billion at

December 31, 2011. If we are required to abide by the terms of

the new FNMA policy, our representations and warranties liability

will likely increase.

Experience with Investors Other than Government-

sponsored Enterprises

In prior years, legacy companies and certain subsidiaries have

sold pools of first-lien mortgage loans and home equity loans as

private-label securitizations or in the form of whole loans. As

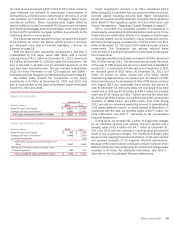

detailed in Table 12, legacy companies and certain subsidiaries

sold loans originated from 2004 through 2008 with an original

principal balance of $963 billion to investors other than GSEs

(although the GSEs are investors in certain private-label

securitizations), of which approximately $506 billion in principal

has been paid and $239 billion has defaulted or are severely

delinquent at December 31, 2011.

As it relates to private-label securitizations, a contractual

liability to repurchase mortgage loans generally arises only if

counterparties prove there is a breach of the representations and

warranties that materially and adversely affects the interest of the

investor or all investors in a securitization trust or of the monoline

insurer or other financial guarantor (as applicable). We believe that

the longer a loan performs, the less likely it is that an alleged

representations and warranties breach had a material impact on

the loan’s performance or that a breach even exists. Because the

majority of the borrowers in this population would have made a

significant number of payments if they are not yet 180 days or

more past due, we believe that the principal balance at the greatest

risk for repurchase claims in this population of private-label

securitization investors is a combination of loans that have already

defaulted and those that are currently severely delinquent.

Additionally, the obligation to repurchase loans also requires that

counterparties have the contractual right to demand repurchase

of the loans (presentation thresholds). While we believe the

agreements for private-label securitizations generally contain less

rigorous representations and warranties and place higher burdens

on investors seeking repurchases than the explicit provisions of

the comparable agreements with the GSEs without regard to any

variations that may have arisen as a result of dealings with the

GSEs, the agreements generally include a representation that

underwriting practices were prudent and customary.

Any amounts paid related to repurchase claims from a monoline

insurer are paid to the securitization trust and are applied in

accordance with the terms of the governing securitization

documents, which may include use by the securitization trust to

repay any outstanding monoline advances or reduce future

advances from the monolines. To the extent that a monoline has

not advanced funds or does not anticipate that it will be required

to advance funds to the securitization trust, the likelihood of

receiving a repurchase claim from a monoline may be reduced as

the monoline would receive limited or no benefit from the payment

of repurchase claims. Moreover, some monolines are not currently