Bank of America 2011 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

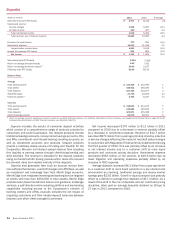

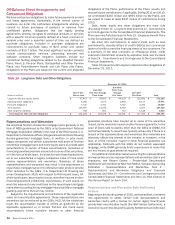

Bank of America 2011 41

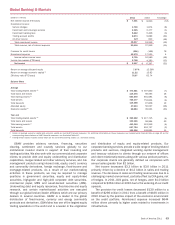

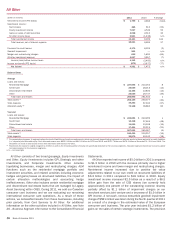

Global Commercial Banking

(Dollars in millions)

Net interest income (FTE basis)

Noninterest income:

Service charges

All other income

Total noninterest income

Total revenue, net of interest expense

Provision for credit losses

Noninterest expense

Income before income taxes

Income tax expense (FTE basis)

Net income

Net interest yield (FTE basis)

Return on average allocated equity

Return on average economic capital (1)

Efficiency ratio (FTE basis)

Balance Sheet

Average

Total loans and leases

Total earning assets

Total assets

Total deposits

Allocated equity

Economic capital (1)

Year end

Total loans and leases

Total earning assets

Total assets

Total deposits

2011

$ 7,176

2,264

1,113

3,377

10,553

(634)

4,234

6,953

2,551

$ 4,402

2.65%

10.77

21.83

40.12

$ 189,415

270,901

309,044

169,192

40,867

20,172

$ 188,262

250,882

289,985

176,941

2010

$ 8,007

2,340

879

3,219

11,226

1,979

4,130

5,117

1,899

$ 3,218

2.94%

7.38

14.07

36.79

$ 203,824

272,401

309,326

148,638

43,590

22,906

$ 194,038

274,624

312,807

161,279

% Change

(10)%

(3)

27

5

(6)

n/m

3

36

34

37

(7)

(1)

—

14

(6)

(12)

(3)

(9)

(7)

10

(1) Return on average economic capital and economic capital are non-GAAP financial measures. For additional information on these measures, see Supplemental Financial Data on page 32 and for

corresponding reconciliations to GAAP financial measures, see Statistical Table XVI.

n/m = not meaningful

Global Commercial Banking provides a wide range of lending-

related products and services, integrated working capital

management and treasury solutions to clients through our network

of offices and client relationship teams along with various product

partners. Our clients include business banking and middle-market

companies, commercial real estate firms and governments, and

are generally defined as companies with annual sales up to

$2 billion. Our lending products and services include commercial

loans and commitment facilities, real estate lending, asset-based

lending and indirect consumer loans. Our capital management and

treasury solutions include treasury management, foreign

exchange and short-term investing options. Effective in 2011,

management responsibility for the merchant services joint venture,

Banc of America Merchant Services, LLC, was moved from GBAM

to Global Commercial Banking where it more closely aligns with

the business model. Prior periods have been reclassified to reflect

this change. In 2011, we recorded $1.1 billion of impairment

charges on our investment in the joint venture. Because of the

recent transfer of the joint venture to Global Commercial Banking,

the impairment charges were recorded in All Other. For additional

information, see Note 5 – Securities to the Consolidated Financial

Statements.

Net income increased $1.2 billion to $4.4 billion in 2011 from

2010 primarily driven by an improvement in the provision for credit

losses, offset by lower revenue and higher expenses.

Revenue decreased $673 million primarily driven by lower net

interest income related to ALM activities and lower average loan

balances, partially offset by an increase in average deposits as

clients continue to maintain high levels of liquidity. Noninterest

income increased $158 million largely due to a gain on the

termination of a purchase contract, an increase in tax credit and

commercial card income, and higher investment gains in the

commercial real estate portfolio.

The provision for credit losses decreased $2.6 billion to a

benefit of $634 million for 2011 compared to 2010. The decrease

was driven by improved economic conditions and an accelerated

rate of loan resolutions in the commercial real estate portfolio.

Noninterest expense increased $104 million driven primarily

by higher FDIC expense.

The return on average economic capital increased due to higher

net income and the 12 percent decrease in average economic

capital. Economic capital decreased due to declining loan

balances and improvements in credit quality. Average allocated

equity decreased due to the same reasons as economic capital.

For more information regarding economic capital and allocated

equity, see Supplemental Financial Data on page 32.