Bank of America 2011 Annual Report Download - page 219

Download and view the complete annual report

Please find page 219 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 217

the SEC, the Financial Industry Regulatory Authority, the New York

Stock Exchange, the FSA and other domestic, international and

state securities regulators. In connection with formal and informal

inquiries by those agencies, such subsidiaries receive numerous

requests, subpoenas and orders for documents, testimony and

information in connection with various aspects of their regulated

activities.

In view of the inherent difficulty of predicting the outcome of

such litigation and regulatory matters, particularly where the

claimants seek very large or indeterminate damages or where the

matters present novel legal theories or involve a large number of

parties, the Corporation generally cannot predict what the eventual

outcome of the pending matters will be, what the timing of the

ultimate resolution of these matters will be, or what the eventual

loss, fines or penalties related to each pending matter may be.

In accordance with applicable accounting guidance, the

Corporation establishes an accrued liability for litigation and

regulatory matters when those matters present loss contingencies

that are both probable and estimable. In such cases, there may

be an exposure to loss in excess of any amounts accrued. When

a loss contingency is not both probable and estimable, the

Corporation does not establish an accrued liability. As a litigation

or regulatory matter develops, the Corporation, in conjunction with

any outside counsel handling the matter, evaluates on an ongoing

basis whether such matter presents a loss contingency that is

probable and estimable. If, at the time of evaluation, the loss

contingency related to a litigation or regulatory matter is not both

probable and estimable, the matter will continue to be monitored

for further developments that would make such loss contingency

both probable and estimable. Once the loss contingency related

to a litigation or regulatory matter is deemed to be both probable

and estimable, the Corporation will establish an accrued liability

with respect to such loss contingency and record a corresponding

amount of litigation-related expense. The Corporation continues

to monitor the matter for further developments that could affect

the amount of the accrued liability that has been previously

established. Excluding expenses of internal or external legal

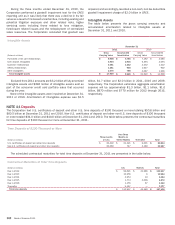

service providers, litigation-related expense of $5.6 billion was

recognized for 2011 compared to $2.6 billion for 2010.

For a limited number of the matters disclosed in this Note for

which a loss is probable or reasonably possible in future periods,

whether in excess of a related accrued liability or where there is

no accrued liability, the Corporation is able to estimate a range of

possible loss. In determining whether it is possible to provide an

estimate of loss or range of possible loss, the Corporation reviews

and evaluates its material litigation and regulatory matters on an

ongoing basis, in conjunction with any outside counsel handling

the matter, in light of potentially relevant factual and legal

developments. These may include information learned through the

discovery process, rulings on dispositive motions, settlement

discussions, and other rulings by courts, arbitrators or others. In

cases in which the Corporation possesses sufficient appropriate

information to develop an estimate of loss or range of possible

loss, that estimate is aggregated and disclosed below. There may

be other disclosed matters for which a loss is probable or

reasonably possible but such an estimate may not be possible.

For those matters where an estimate is possible, management

currently estimates the aggregate range of possible loss is $0 to

$3.6 billion in excess of the accrued liability (if any) related to

those matters. This estimated range of possible loss is based

upon currently available information and is subject to significant

judgment and a variety of assumptions, and known and unknown

uncertainties. The matters underlying the estimated range will

change from time to time, and actual results may vary significantly

from the current estimate. Those matters for which an estimate

is not possible are not included within this estimated range.

Therefore, this estimated range of possible loss represents what

the Corporation believes to be an estimate of possible loss only

for certain matters meeting these criteria. It does not represent

the Corporation’s maximum loss exposure. Information is provided

below regarding the nature of all of these contingencies and, where

specified, the amount of the claim associated with these loss

contingencies. Based on current knowledge, management does

not believe that loss contingencies arising from pending matters,

including the matters described herein, will have a material

adverse effect on the consolidated financial position or liquidity

of the Corporation. However, in light of the inherent uncertainties

involved in these matters, some of which are beyond the

Corporation’s control, and the very large or indeterminate damages

sought in some of these matters, an adverse outcome in one or

more of these matters could be material to the Corporation’s

results of operations or cash flows for any particular reporting

period.

Auction Rate Securities Litigation

Since October 2007, the Corporation, Merrill Lynch and certain

affiliates have been named as defendants in a variety of lawsuits

and other proceedings brought by customers and both individual

and institutional investors regarding auction rate securities (ARS).

These actions generally allege that defendants: (i) misled plaintiffs

into believing that there was a deeply liquid market for ARS, and

(ii) failed to adequately disclose their or their affiliates’ practice

of placing their own bids to support ARS auctions. Plaintiffs assert

that ARS auctions started failing from August 2007 through

February 2008 when defendants and other broker/dealers

stopped placing those “support bids.” In addition to the matters

described in more detail below, numerous arbitrations and

individual lawsuits have been filed against the Corporation, Merrill

Lynch and certain affiliates by parties who purchased ARS and are

seeking relief that includes compensatory and punitive damages

totaling in excess of $1.2 billion, as well as rescission, among

other relief.

Securities Actions

The Corporation and Merrill Lynch face a number of civil actions

relating to the sales of ARS and management of ARS auctions,

including two putative class action lawsuits in which plaintiffs seek

to recover the alleged losses in market value of ARS securities

purportedly caused by defendants’ actions. Plaintiffs also seek

unspecified damages, including rescission, other compensatory

and consequential damages, costs, fees and interest. The first

action, In Re Merrill Lynch Auction Rate Securities Litigation, is the

result of the consolidation of two class action suits in the U.S.

District Court for the Southern District of New York. These suits

were brought by two Merrill Lynch customers on behalf of all

persons who purchased ARS in auctions managed by Merrill Lynch,

against Merrill Lynch and Merrill Lynch, Pierce, Fenner & Smith

Incorporated (MLPF&S). On March 31, 2010, the U.S. District Court

for the Southern District of New York granted Merrill Lynch’s motion

to dismiss. Plaintiffs appealed and on November 14, 2011, the

U.S. Court of Appeals for the Second Circuit affirmed the district

court’s dismissal. Plaintiffs’ time to seek a writ of certiorari to the

U.S. Supreme Court expired on February 13, 2012, and, as a result,