Bank of America 2011 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

62 Bank of America 2011

The Financial Reform Act will continue to have a significant and

negative impact on our earnings through fee reductions, higher

costs and new restrictions, as well as reductions to available

capital. The Financial Reform Act may also continue to have a

material adverse impact on the value of certain assets and

liabilities held on our balance sheet. The ultimate impact of the

Financial Reform Act on our businesses and results of operations

will depend on regulatory interpretation and rulemaking, as well

as the success of any of our actions to mitigate the negative

earnings impact of certain provisions. For information on the

impact of the Financial Reform Act on our credit ratings, see

Liquidity Risk on page 70.

Transactions with Affiliates

The terms of certain of our OTC derivative contracts and other

trading agreements of the Corporation provide that upon the

occurrence of certain specified events, such as a change in our

credit ratings, Merrill Lynch and other non-bank affiliates may be

required to provide additional collateral or to provide other

remedies, or our counterparties may have the right to terminate

or otherwise diminish our rights under these contracts or

agreements. Following the recent downgrade of the credit ratings

of the Corporation and other non-bank affiliates, we have engaged

in discussions with certain derivative and other counterparties

regarding their rights under these agreements. In response to

counterparties’ inquiries and requests, we have discussed and in

some cases substituted derivative contracts and other trading

agreements, including naming BANA as the new counterparty. Our

ability to substitute or make changes to these agreements to meet

counterparties’ requests may be subject to certain limitations,

including counterparty willingness, regulatory limitations on

naming BANA as the new counterparty, and the type or amount of

collateral required. It is possible that such limitations on our ability

to substitute or make changes to these agreements, including

naming BANA as the new counterparty, could adversely affect our

results of operations.

Other Matters

The Corporation has established guidelines and policies for

managing capital across its subsidiaries. The guidance for the

Corporation’s subsidiaries with regulatory capital requirements,

including branch operations of banking subsidiaries, requires each

entity to maintain satisfactory capital levels. This includes setting

internal capital targets for the U.S. bank subsidiaries to exceed

“well capitalized” levels. The U.K. has adopted increased capital

and liquidity requirements for local financial institutions, including

regulated U.K. subsidiaries of non-U.K. bank holding companies

and other financial institutions as well as branches of non-U.K.

banks located in the U.K. In addition, the U.K. has proposed the

creation and production of recovery and resolution plans,

commonly referred to as living wills, by such entities. We are

currently monitoring the impact of these initiatives.

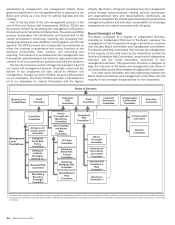

Managing Risk

Overview

Risk is inherent in every material business activity that we

undertake. Our business exposes us to strategic, credit, market,

liquidity, compliance, operational and reputational risk. We must

manage these risks to maximize our long-term results by ensuring

the integrity of our assets and the quality of our earnings.

Strategic risk is the risk that results from adverse business

decisions, ineffective or inappropriate business plans, or failure

to respond to changes in the competitive environment, business

cycles, customer preferences, product obsolescence, regulatory

environment, business strategy execution, and/or other inherent

risks of the business including reputational risk. Credit risk is the

risk of loss arising from a borrower’s or counterparty’s inability to

meet its obligations. Market risk is the risk that values of assets

and liabilities or revenues will be adversely affected by changes

in market conditions such as interest rate movements. Liquidity

risk is the inability to meet contractual and contingent financial

obligations, on-or off-balance sheet, as they come due. Compliance

risk is the risk that arises from the failure to adhere to laws, rules,

regulations, or internal policies and procedures. Operational risk

is the risk of loss resulting from inadequate or failed internal

processes, people and systems, or external events. Reputational

risk is the potential that negative publicity regarding an

organization’s conduct or business practices will adversely affect

its profitability, operations or customer base, or result in costly

litigation or require other measures. Reputational risk is evaluated

along with all of the risk categories and throughout the risk

management process, and as such is not discussed separately

herein. The following sections, Strategic Risk Management on

page 65, Capital Management on page 65, Liquidity Risk on

page 70, Credit Risk Management on page 74, Market Risk

Management on page 106, Compliance Risk Management and

Operational Risk Management both on page 113, address in more

detail the specific procedures, measures and analyses of the major

categories of risk that we manage.

In choosing when and how to take risks, we evaluate our

capacity for risk and seek to protect our brand and reputation, our

financial flexibility, the value of our assets and the strategic

potential of the Corporation. We intend to maintain a strong and

flexible financial position. We also intend to focus on maintaining

our relevance and value to customers, employees and

shareholders. As part of our efforts to achieve these objectives,

we continue to build a comprehensive risk management culture

and to implement governance and control measures to strengthen

that culture.

We take a comprehensive approach to risk management. We

have a defined risk framework and clearly articulated risk appetite

which is approved annually by the Corporation’s Board of Directors

(the Board). Risk management planning is integrated with

strategic, financial and customer/client planning so that goals and

responsibilities are aligned across the organization. Risk is

managed in a systematic manner by focusing on the Corporation

as a whole as well as managing risk across the enterprise and

within individual business units, products, services and

transactions, and across all geographic locations. We maintain a

governance structure that delineates the responsibilities for risk

management activities, as well as governance and oversight of

those activities.

Executive management assesses, and the Board oversees, the

risk-adjusted returns of each business segment. Management

reviews and approves strategic and financial operating plans, and

recommends to the Board for approval a financial plan annually.

By allocating economic capital to and establishing a risk appetite

for a business segment, we seek to effectively manage the ability

to take on risk. Economic capital is assigned to each business

segment using a risk-adjusted methodology incorporating each

segment’s stand-alone credit, market, interest rate and operational