Bank of America 2011 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 53

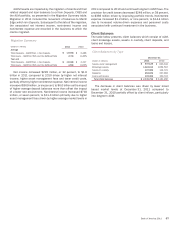

GSEs may be materially impacted if actual experiences are

different from our assumptions. The GSEs’ repurchase requests,

standards for rescission of repurchase requests, and resolution

processes have become increasingly inconsistent with the GSE’s

own past conduct and the Corporation’s interpretation of its

contractual obligations. These developments have resulted in an

increase in claims outstanding from the GSEs. We intend to

repurchase loans to the extent required under the contracts and

standards that govern our relationships with the GSEs. While we

are seeking to resolve our differences with the GSEs concerning

each party’s interpretation of the requirements of the governing

contracts, whether we will be able to achieve a resolution of these

differences on acceptable terms, and timing thereof, is subject to

significant uncertainty.

We are not able to predict changes in the behavior of the GSEs

based on our past experiences. Therefore, it is not possible to

reasonably estimate a possible loss or range of possible loss with

respect to any such potential impact in excess of current accrued

liabilities. See Complex Accounting Estimates – Representations

and Warranties on page 119 for information related to the

sensitivity of the assumptions used to estimate our liability for

obligations under representations and warranties.

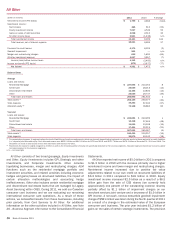

Non-Government-sponsored Enterprises

The population of private-label securitizations included in the BNY

Mellon Settlement encompasses almost all legacy Countrywide

first-lien private-label securitizations including loans originated

principally in the 2004 through 2008 vintages. For the remainder

of the population of private-label securitizations, we believe it is

probable that other claimants in certain types of securitizations

may come forward with claims that meet the requirements of the

terms of the securitizations. We have seen an increased trend in

requests for loan files from private-label securitization trustees

and an increase in repurchase claims from private-label

securitization trustees that meet the required standards. We

believe that the provisions recorded in connection with the BNY

Mellon Settlement and the additional non-GSE representations

and warranties provisions recorded in 2011 have provided for a

substantial portion of our non-GSE representations and warranties

exposure. However, it is reasonably possible that future

representations and warranties losses may occur in excess of the

amounts recorded for these exposures. In addition, we have not

recorded any representations and warranties liability for certain

potential monoline exposures and certain potential whole loan and

other private-label securitization exposures. We currently estimate

that the range of possible loss related to non-GSE representations

and warranties exposure as of December 31, 2011 could be up

to $5 billion over existing accruals. The estimated range of

possible loss for non-GSE representations and warranties does

not represent a probable loss, and is based on currently available

information, significant judgment, and a number of assumptions,

including those set forth below, that are subject to change.

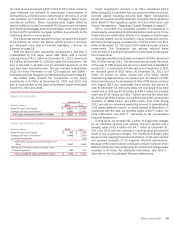

The methodology used to estimate the non-GSE

representations and warranties liability and the corresponding

range of possible loss considers a variety of factors including our

experience related to actual defaults, projected future defaults,

historical loss experience, estimated home prices and other

economic conditions. Among the factors that impact the non-GSE

representations and warranties liability and the corresponding

estimated range of possible loss are: (1) contractual loss

causation requirements, (2) the representations and warranties

provided, and (3) the requirement to meet certain presentation

thresholds. The first factor is based on our belief that a non-GSE

contractual liability to repurchase a loan generally arises only if

the counterparties prove there is a breach of representations and

warranties that materially and adversely affects the interest of the

investor or all investors, or the monoline insurer (as applicable),

in a securitization trust, and accordingly, we believe that the

repurchase claimants must prove that the alleged representations

and warranties breach was the cause of the loss. The second

factor is related to the fact that non-GSE securitizations include

different types of representations and warranties than those

provided to the GSEs. We believe the non-GSE securitizations’

representations and warranties are less rigorous and actionable

than the explicit provisions of the comparable agreements with

the GSEs without regard to any variations that may have arisen as

a result of dealings with the GSEs. The third factor is related to

the fact that certain presentation thresholds need to be met in

order for any repurchase claim to be asserted on the initiative of

investors under the non-GSE agreements. A securitization trustee

may investigate or demand repurchase on its own action, and most

agreements contain a threshold, for example 25 percent of the

voting rights per trust, that allows investors to declare a servicing

event of default under certain circumstances or to request certain

action, such as requesting loan files, that the trustee may choose

to accept and follow, exempt from liability, provided the trustee is

acting in good faith. If there is an uncured servicing event of default,

and the trustee fails to bring suit during a 60-day period, then,

under most agreements, investors may file suit. In addition to this,

most agreements also allow investors to direct the securitization

trustee to investigate loan files or demand the repurchase of loans,

if security holders hold a specified percentage, for example 25

percent, of the voting rights of each tranche of the outstanding

securities. Although we continue to believe that presentation

thresholds are a factor in the determination of probable loss, given

the BNY Mellon Settlement, the estimated range of possible loss

assumes that the presentation threshold can be met for all of the

non-GSE securitization transactions.

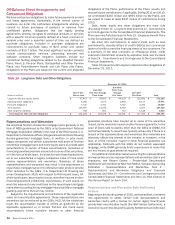

In addition, in the case of private-label securitizations, our

estimate considers implied repurchase experience based on the

BNY Mellon Settlement, adjusted to reflect differences between

the Covered Trusts and the remainder of the population of private-

label securitizations, and assumes that the conditions to the BNY

Mellon Settlement will be satisfied. For additional information

about the methodology used to estimate the non-GSE

representations and warranties liability and the corresponding

range of possible loss, see Note 9 – Representations and

Warranties Obligations and Corporate Guarantees to the

Consolidated Financial Statements.

Future provisions and/or ranges of possible loss for non-GSE

representations and warranties may be significantly impacted if

actual experiences are different from our assumptions in our

predictive models, including, without limitation, those regarding

ultimate resolution of the BNY Mellon Settlement, estimated

repurchase rates, economic conditions, estimated home prices,

consumer and counterparty behavior, and a variety of other

judgmental factors. Adverse developments with respect to one or

more of the assumptions underlying the liability for representations

and warranties and the corresponding estimated range of possible

loss could result in significant increases to future provisions and

this estimated range of possible loss. For example, if courts were

to disagree with our interpretation that the underlying agreements

require a claimant to prove that the representations and warranties

breach was the cause of the loss, it could significantly impact this