Bank of America 2011 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 33

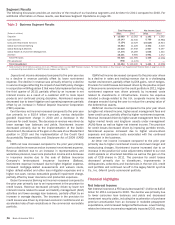

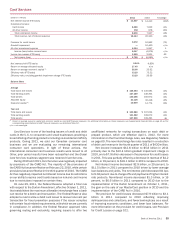

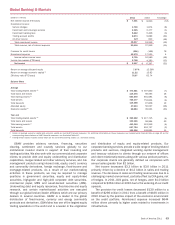

Core Net Interest Income

We manage core net interest income which is reported net interest

income on a FTE basis adjusted for the impact of market-based

activities. As discussed in the GBAM business segment section

on page 43, we evaluate our market-based results and strategies

on a total market-based revenue approach by combining net

interest income and noninterest income for GBAM. An analysis of

core net interest income, core average earning assets and core

net interest yield on earning assets, all of which adjust for the

impact of market-based activities from reported net interest

income on a FTE basis, is shown below. We believe the use of this

non-GAAP presentation in Table 9 provides additional clarity in

assessing our results.

Table 9

(Dollars in millions)

Net interest income (FTE basis)

As reported (1)

Impact of market-based net interest income (2)

Core net interest income

Average earning assets

As reported

Impact of market-based earning assets (2)

Core average earning assets

Net interest yield contribution (FTE basis)

As reported (1)

Impact of market-based activities (2)

Core net interest yield on earning assets

Core Net Interest Income

2011

$ 45,588

(3,813)

41,775

1,834,659

(448,776)

$ 1,385,883

2.48%

0.53

3.01%

2010

$ 52,693

(4,430)

48,263

1,897,573

(512,804)

$1,384,769

2.78%

0.71

3.49%

(1) Net interest income and net interest yield include fees earned on overnight deposits placed

with the Federal Reserve of $186 million and $368 million for 2011 and 2010.

(2) Represents the impact of market-based amounts included in GBAM.

Core net interest income decreased $6.5 billion to $41.8 billion

for 2011 compared to 2010. The decline was primarily due to

lower consumer loan balances and yields and decreased

investment security yields, including the acceleration of purchase

premium amortization from an increase in modeled prepayment

expectations and increased hedge ineffectiveness. These

decreases were partially offset by ongoing reductions in our debt

footprint and lower interest rates paid on deposits.

Core average earning assets increased $1.1 billion to $1,385.9

billion for 2011 compared to 2010. The increase was primarily

due to growth in investment securities partially offset by declines

in consumer loans.

Core net interest yield decreased 48 bps to 3.01 percent for

2011 compared to 2010 primarily due to the factors noted above.

In addition, the yield curve flattened significantly with long-term

rates near historical lows at December 31, 2011. This has resulted

in net interest yield compression as assets have repriced down

and liability yields have declined less significantly due to the

absolute low level of short-end rates.

Business Segment Operations

Segment Description and Basis of Presentation

We report the results of our operations through six business

segments: Deposits, Card Services, CRES, Global Commercial

Banking, GBAM and GWIM, with the remaining operations recorded

in All Other.

We prepare and evaluate segment results using certain non-

GAAP financial measures, many of which are discussed in

Supplemental Financial Data on page 32. We begin by evaluating

the operating results of the segments which by definition exclude

merger and restructuring charges.

The management accounting and reporting process derives

segment and business results by utilizing allocation

methodologies for revenue and expense. The net income derived

for the businesses is dependent upon revenue and cost allocations

using an activity-based costing model, funds transfer pricing, and

other methodologies and assumptions management believes are

appropriate to reflect the results of the business.

Total revenue, net of interest expense, includes net interest

income on a FTE basis and noninterest income. The adjustment

of net interest income to a FTE basis results in a corresponding

increase in income tax expense. The segment results also reflect

certain revenue and expense methodologies that are utilized to

determine net income. The net interest income of the businesses

includes the results of a funds transfer pricing process that

matches assets and liabilities with similar interest rate sensitivity

and maturity characteristics. For presentation purposes, in

segments where the total of liabilities and equity exceeds assets,

which are generally deposit-taking segments, we allocate assets

to match liabilities. Net interest income of the business segments

also includes an allocation of net interest income generated by

certain of our ALM activities.

Our ALM activities include an overall interest rate risk

management strategy that incorporates the use of various

derivatives and cash instruments to manage fluctuations in

earnings and capital that are caused by interest rate volatility. Our

goal is to manage interest rate sensitivity so that movements in

interest rates do not significantly adversely affect earnings and

capital. The majority of our ALM activities are allocated to the

business segments and fluctuate based on performance. ALM

activities include external product pricing decisions including

deposit pricing strategies, the effects of our internal funds transfer

pricing process and the net effects of other ALM activities.

Certain expenses not directly attributable to a specific business

segment are allocated to the segments. The most significant of

these expenses include data and item processing costs and

certain centralized or shared functions. Data processing costs are

allocated to the segments based on equipment usage. Item

processing costs are allocated to the segments based on the

volume of items processed for each segment. The costs of certain

centralized or shared functions are allocated based on

methodologies that reflect utilization.

Equity is allocated to business segments and related

businesses using a risk-adjusted methodology incorporating each

segment’s credit, market, interest rate, strategic and operational

risk components. The nature of these risks is discussed further

on page 62. We benefit from the diversification of risk across these

components which is reflected as a reduction to allocated equity

for each segment. The total amount of average allocated equity

reflects both risk-based capital and the portion of goodwill and

intangibles specifically assigned to the business segments. The

risk-adjusted methodology is periodically refined and such

refinements are reflected as changes to allocated equity in each

segment.

For more information on selected financial information for the

business segments and reconciliations to consolidated total

revenue, net income (loss) and year-end total assets, see Note 26

– Business Segment Information to the Consolidated Financial

Statements.