Bank of America 2011 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

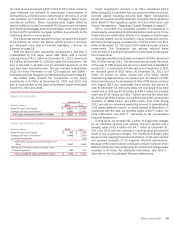

Bank of America 2011 59

of the terms of the Servicing Resolution Agreements. The

refinancing assistance commitment under the Servicing

Resolution Agreements is expected to be recognized as lower

interest income in future periods as qualified borrowers pay

reduced interest rates on loans refinanced. Although we may incur

additional operating costs (e.g., servicing costs) to implement

parts of the Servicing Resolution Agreements in future periods, it

is expected that those costs will not be material.

The Servicing Resolution Agreements do not cover claims

arising out of securitization (including representations made to

investors respecting MBS), criminal claims, private claims by

borrowers, claims by certain states for injunctive relief or actual

economic damages to borrowers related to the Mortgage

Electronic Registration Systems, Inc. (MERS), and claims by the

GSEs (including repurchase demands), among other items. Failure

to finalize the documentation related to the Servicing Resolution

Agreements, to obtain the required court and regulatory approvals,

to meet our borrower and refinancing commitments or other

adverse developments with respect to the foregoing could have a

material adverse effect on our financial condition and results of

operations.

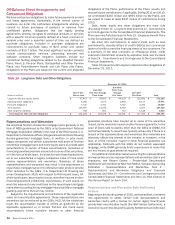

Mortgage Electronic Registration Systems, Inc.

Mortgage notes, assignments or other documents are often

required to be maintained and are often necessary to enforce

mortgage loans. There has been significant public commentary

regarding the common industry practice of recording mortgages

in the name of MERS, as nominee on behalf of the note holder,

and whether securitization trusts own the loans purported to be

conveyed to them and have valid liens securing those loans. We

currently use the MERS system for a substantial portion of the

residential mortgage loans that we originate, including loans that

have been sold to investors or securitization trusts. A component

of the OCC consent order requires significant changes in the

manner in which we service loans identifying MERS as the

mortgagee. Additionally, certain local and state governments have

commenced legal actions against us, MERS, and other MERS

members, questioning the validity of the MERS model. Other

challenges have also been made to the process for transferring

mortgage loans to securitization trusts, asserting that having a

mortgagee of record that is different than the holder of the

mortgage note could “break the chain of title” and cloud the

ownership of the loan. In order to foreclose on a mortgage loan,

in certain cases it may be necessary or prudent for an assignment

of the mortgage to be made to the holder of the note, which in the

case of a mortgage held in the name of MERS as nominee would

need to be completed by a MERS signing officer. As such, our

practice is to obtain assignments of mortgages from MERS prior

to instituting foreclosure. If certain required documents are

missing or defective, or if the use of MERS is found not to be valid,

we could be obligated to cure certain defects or in some

circumstances be subject to additional costs and expenses. Our

use of MERS as nominee for the mortgage may also create

reputational risks for us.

Impact of Foreclosure Delays

In 2011, we incurred $1.8 billion of mortgage-related assessments

and waivers costs which included $1.3 billion for compensatory

fees that we expect to be claimed by the GSEs as a result of

foreclosure delays with the remainder being out-of-pocket costs

that we do not expect to recover because of foreclosure delays.

We expect that mortgage-related assessments and waivers costs,

compensatory fees assessed by the GSEs and other costs

associated with foreclosures will remain elevated as additional

loans are delayed in the foreclosure process, although we believe

that the governing contracts, our course of dealing, and collective

past practices and understandings should inform resolution of

these matters. We also expect additional costs related to

resources necessary to perform the foreclosure process

assessment and to implement other operational changes will

continue. This will likely result in continued higher noninterest

expense, including higher default servicing costs and legal

expenses in CRES, and has impacted and may continue to impact

the value of our MSRs related to these serviced loans. It is also

possible that the delays in foreclosure sales may result in

additional costs and expenses, including costs associated with

the maintenance of properties or possible home price declines

while foreclosures are delayed. In addition, required process

changes, including those required under the consent orders with

federal bank regulators, are likely to result in further increases in

our default servicing costs over the longer term. Finally, the time

to complete foreclosure sales may continue to be protracted, which

may result in a greater number of nonperforming loans and

increased servicing advances and may impact the collectability of

such advances and the value of our MSR asset, MBS and real

estate owned properties.

An increase in the time to complete foreclosure sales also may

increase the number of severely delinquent loans in our mortgage

servicing portfolio, result in increasing levels of consumer

nonperforming loans and could have a dampening effect on net

interest margin as nonperforming assets increase. Accordingly,

delays in foreclosure sales, including any delays beyond those

currently anticipated, our continued process enhancements,

including those required under the OCC and Federal Reserve

consent orders and any issues that may arise out of alleged

irregularities in our foreclosure process could significantly increase

the costs associated with our mortgage operations.

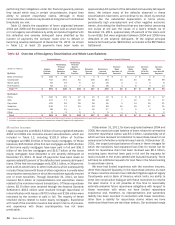

Mortgage-related Settlements – Servicing Matters

In connection with the BNY Mellon Settlement, BANA has agreed

to implement certain servicing changes. The Trustee and BANA

have agreed to clarify and conform certain servicing standards

related to loss mitigation. In particular, the BNY Mellon Settlement

would clarify that it is permissible to apply the same loss-mitigation

strategies to the Covered Trusts as are applied to BANA affiliates’

held-for-investment (HFI) portfolios. This portion of the agreement

was effective in the second quarter of 2011 and is not conditioned

on final court approval.

BANA also agreed to transfer the servicing related to certain

high-risk loans to qualified subservicers on a schedule that began

with the signing of the BNY Mellon Settlement. This servicing

transfer protocol will reduce the servicing fees payable to BANA

in the future. Upon final court approval, failure to meet the

established benchmarking standards for loans not in subservicing

arrangements can trigger the payment of agreed-upon fees.

Additionally, we and legacy Countrywide have agreed to work to

resolve with the Trustee certain mortgage documentation issues

related to the enforceability of mortgages in foreclosure and to

reimburse the related Covered Trust for any loss if BANA is unable

to foreclose on the mortgage and the Covered Trust is not made

whole by a title policy because of these documentation issues.

These agreements will terminate if final court approval of the BNY

Mellon Settlement is not obtained, although we could still have

exposure under the pooling and servicing agreements related to