Bank of America 2011 Annual Report Download - page 160

Download and view the complete annual report

Please find page 160 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

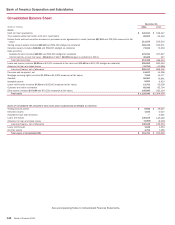

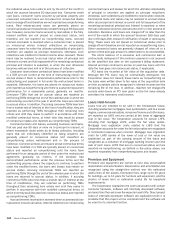

158 Bank of America 2011

the collateral value, less costs to sell, by the end of the month in

which the account becomes 60 days past due. Consumer credit

card loans, consumer loans secured by personal property and

unsecured consumer loans are not placed on nonaccrual status

prior to charge-off and therefore are not reported as nonperforming

loans. Real estate-secured loans are generally placed on

nonaccrual status and classified as nonperforming at 90 days past

due. However, consumer loans secured by real estate in the fully-

insured portfolio are not placed on nonaccrual status, and

therefore, are not reported as nonperforming loans. Accrued

interest receivable is reversed when a consumer loan is placed

on nonaccrual status. Interest collections on nonaccruing

consumer loans for which the ultimate collectability of principal is

uncertain are applied as principal reductions; otherwise, such

collections are credited to interest income when received. These

loans may be restored to accrual status when all principal and

interest is current and full repayment of the remaining contractual

principal and interest is expected, or when the loan otherwise

becomes well-secured and is in the process of collection.

Consumer loans whose contractual terms have been modified

in a TDR and are current at the time of restructuring remain on

accrual status if there is demonstrated performance prior to the

restructuring and payment in full under the restructured terms is

expected. Otherwise, the loans are placed on nonaccrual status

and reported as nonperforming until there is sustained repayment

performance for a reasonable period, generally six months.

Consumer TDRs that are on accrual status are reported as

performing TDRs through the end of the calendar year in which the

restructuring occurred or the year in which the loans are returned

to accrual status. In addition, if accruing consumer TDRs bear less

than a market rate of interest at the time of modification, they are

reported as performing TDRs throughout their remaining lives

unless and until they cease to perform in accordance with their

modified contractual terms, at which time they would be placed

on nonaccrual status and reported as nonperforming TDRs.

Commercial loans and leases, excluding business card loans,

that are past due 90 days or more as to principal or interest, or

where reasonable doubt exists as to timely collection, including

loans that are individually identified as being impaired, are

generally placed on nonaccrual status and classified as

nonperforming unless well-secured and in the process of

collection. Commercial loans and leases whose contractual terms

have been modified in a TDR are typically placed on nonaccrual

status and reported as nonperforming until the loans have

performed for an adequate period of time under the restructured

agreement, generally six months. If the borrower had

demonstrated performance under the previous terms and the

underwriting process shows the capacity to continue to perform

under the modified terms, the loans and leases may remain on

accrual status. Accruing commercial TDRs are reported as

performing TDRs through the end of the calendar year in which the

loans are returned to accrual status. In addition, if accruing

commercial TDRs bear less than a market rate of interest at the

time of modification, they are reported as performing TDRs

throughout their remaining lives unless and until they cease to

perform in accordance with their modified contractual terms, at

which time they would be placed on nonaccrual status and reported

as nonperforming TDRs.

Accrued interest receivable is reversed when a commercial loan

is placed on nonaccrual status. Interest collections on nonaccruing

commercial loans and leases for which the ultimate collectability

of principal is uncertain are applied as principal reductions;

otherwise, such collections are credited to income when received.

Commercial loans and leases may be restored to accrual status

when all principal and interest is current and full repayment of the

remaining contractual principal and interest is expected, or when

the loan otherwise becomes well-secured and is in the process of

collection. Business card loans are charged off no later than the

end of the month in which the account becomes 180 days past

due or 60 days after receipt of notification of death or bankruptcy

filing. These loans are not placed on nonaccrual status prior to

charge-off and therefore are not reported as nonperforming loans.

Other commercial loans are generally charged off when all or a

portion of the principal amount is determined to be uncollectible.

The entire balance of a consumer and commercial loan is

contractually delinquent if the minimum payment is not received

by the specified due date on the customer’s billing statement.

Interest and fees continue to accrue on past due loans until the

date the loan goes into nonaccrual status, if applicable.

PCI loans are recorded at fair value at the acquisition date.

Although the PCI loans may be contractually delinquent, the

Corporation does not classify these loans as nonperforming as

the loans were written down to fair value at the acquisition date

and the accretable yield is recognized in interest income over the

remaining life of the loan. In addition, reported net charge-offs

exclude write-downs on PCI loan pools as the fair value already

considers the estimated credit losses.

Loans Held-for-sale

Loans that are intended to be sold in the foreseeable future,

including residential mortgages, loan syndications, and to a lesser

degree, commercial real estate, consumer finance and other loans,

are reported as LHFS and are carried at the lower of aggregate

cost or fair value. The Corporation accounts for certain LHFS,

including first mortgage LHFS, under the fair value option.

Mortgage loan origination costs related to LHFS that the

Corporation accounts for under the fair value option are recognized

in noninterest expense when incurred. Mortgage loan origination

costs for LHFS carried at the lower of cost or fair value are

capitalized as part of the carrying amount of the loans and

recognized as a reduction of mortgage banking income upon the

sale of such loans. LHFS that are on nonaccrual status and are

reported as nonperforming, as defined in the policy above, are

reported separately from nonperforming loans and leases.

Premises and Equipment

Premises and equipment are carried at cost less accumulated

depreciation and amortization. Depreciation and amortization are

recognized using the straight-line method over the estimated

useful lives of the assets. Estimated lives range up to 40 years

for buildings, up to 12 years for furniture and equipment, and the

shorter of lease term or estimated useful life for leasehold

improvements.

The Corporation capitalizes the costs associated with certain

computer hardware, software and internally developed software,

and amortizes the costs over the expected useful life. Direct project

costs of internally developed software are capitalized when it is

probable that the project will be completed and the software will

be used for its intended function.