Bank of America 2011 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

74 Bank of America 2011

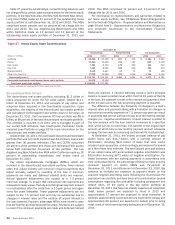

A further reduction in certain of our credit ratings or the ratings

of certain asset-backed securitizations may have a material

adverse effect on our liquidity, potential loss of access to credit

markets, the related cost of funds, our businesses and on certain

trading revenues, particularly in those businesses where

counterparty creditworthiness is critical. In addition, under the

terms of certain OTC derivative contracts and other trading

agreements, the counterparties to those agreements may require

us to provide additional collateral, or to terminate these contracts

or agreements, which could cause us to sustain losses and/or

adversely impact our liquidity. If the short-term credit ratings of

our parent company, bank or broker/dealer subsidiaries were

downgraded by one or more levels, the potential loss of access to

short-term funding sources such as repo financing, and the effect

on our incremental cost of funds could be material.

At December 31, 2011, if the rating agencies had downgraded

their long-term senior debt ratings for the Corporation or certain

subsidiaries by one incremental notch, the amount of additional

collateral contractually required by derivative contracts and other

trading agreements would have been approximately $1.6 billion

comprised of $1.2 billion for BANA and approximately $375 million

for Merrill Lynch and certain of its subsidiaries. If the agencies

had downgraded their long-term senior debt ratings for these

entities by a second incremental notch, approximately $1.1 billion

in additional collateral comprised of $871 million for BANA and

$269 million for Merrill Lynch and certain of its subsidiaries, would

have been required.

Also, if the rating agencies had downgraded their long-term

senior debt ratings for the Corporation or certain subsidiaries by

one incremental notch, the derivative liability that would be subject

to unilateral termination by counterparties as of December 31,

2011 was $2.9 billion, against which $2.7 billion of collateral had

been posted. If the rating agencies had downgraded their long-

term senior debt ratings for the Corporation or certain subsidiaries

a second incremental notch, the derivative liability that would be

subject to unilateral termination by counterparties as of December

31, 2011 was an incremental $5.6 billion, against which $5.4

billion of collateral had been posted.

While certain potential impacts are contractual and

quantifiable, the full scope of consequences of a credit ratings

downgrade to a financial institution are inherently uncertain, as

they depend upon numerous dynamic, complex and inter-related

factors and assumptions, including whether any downgrade of a

firm’s long-term credit ratings precipitates downgrades to its short-

term credit ratings, and assumptions about the potential behaviors

of various customers, investors and counterparties.

For information regarding the additional collateral and

termination payments that could be required in connection with

certain OTC derivative contracts and other trading agreements as

a result of such a credit ratings downgrade, see Note 4 – Derivatives

to the Consolidated Financial Statements and Item 1A. Risk

Factors of this Annual Report on Form 10-K.

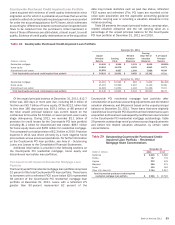

During the third quarter of 2011, Moody’s and S&P placed the

sovereign rating of the United States on review for possible

downgrade due to the possibility of a default on the government’s

debt obligations because of a failure to increase the debt limit.

On August 2, 2011, Moody’s affirmed its Aaa rating and revised

its outlook to negative. On August 5, 2011, S&P downgraded the

long-term sovereign credit rating of the United States to AA+, and

affirmed the short-term sovereign credit rating; the outlook is

negative. On November 28, 2011, Fitch affirmed its AAA long-term

rating of the United States, but changed the outlook from stable

to negative. On the same day, Fitch affirmed its F1+ short-term

rating of the U.S. All three rating agencies have indicated that they

will continue to assess fiscal projections and consolidation

measures, as well as the medium-term economic outlook for the

United States.

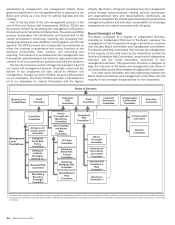

Credit Risk Management

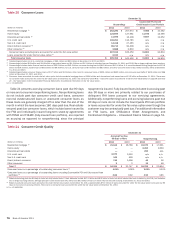

Credit quality continued to improve during 2011. Continued

economic stability and our proactive credit risk management

initiatives positively impacted the credit portfolio as charge-offs

and delinquencies continued to improve across most portfolios

and risk ratings improved in the commercial portfolios. However,

global and national economic uncertainty, home price declines and

regulatory reform continued to weigh on the credit portfolios

through December 31, 2011. For more information, see Executive

Summary – 2011 Economic and Business Environment on page

21.

Credit risk is the risk of loss arising from the inability or failure

of a borrower or counterparty to meet its obligations. Credit risk

can also arise from operational failures that result in an erroneous

advance, commitment or investment of funds. We define the credit

exposure to a borrower or counterparty as the loss potential arising

from all product classifications including loans and leases, deposit

overdrafts, derivatives, assets held-for-sale and unfunded lending

commitments which include loan commitments, letters of credit

and financial guarantees. Derivative positions are recorded at fair

value and assets held-for-sale are recorded at either fair value or

the lower of cost or fair value. Certain loans and unfunded

commitments are accounted for under the fair value option. Credit

risk for these categories of assets is not accounted for as part of

the allowance for credit losses but as part of the fair value

adjustments recorded in earnings. For derivative positions, our

credit risk is measured as the net cost in the event the

counterparties with contracts in which we are in a gain position

fail to perform under the terms of those contracts. We use the

current mark-to-market value to represent credit exposure without

giving consideration to future mark-to-market changes. The credit

risk amounts take into consideration the effects of legally

enforceable master netting agreements and cash collateral. Our

consumer and commercial credit extension and review procedures

take into account funded and unfunded credit exposures. For

additional information on derivative and credit extension

commitments, see Note 4 – Derivatives and Note 14 –

Commitments and Contingencies to the Consolidated Financial

Statements.

We manage credit risk based on the risk profile of the borrower

or counterparty, repayment sources, the nature of underlying

collateral, and other support given current events, conditions and

expectations. We classify our portfolios as either consumer or

commercial and monitor credit risk in each as discussed below.