Bank of America 2011 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 97

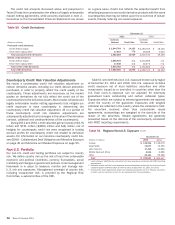

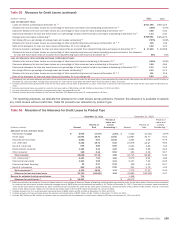

Risk Mitigation

We purchase credit protection to cover the funded portion as well

as the unfunded portion of certain credit exposures. To lower the

cost of obtaining our desired credit protection levels, credit

exposure may be added within an industry, borrower or

counterparty group by selling protection.

At December 31, 2011 and 2010, net notional credit default

protection purchased in our credit derivatives portfolio to hedge

our funded and unfunded exposures for which we elected the fair

value option, as well as certain other credit exposures, was $19.4

billion and $20.1 billion. The mark-to-market effects, including the

cost of net credit default protection hedging our credit exposure,

resulted in net gains of $121 million in 2011 compared to net

losses of $546 million in 2010.

The average VaR for these credit derivative hedges was $60

million in 2011 compared to $53 million in 2010. The average

VaR for the related credit exposure was $74 million in 2011

compared to $65 million in 2010. There is a diversification effect

between the net credit default protection hedging our credit

exposure and the related credit exposure such that the combined

average VaR was $38 million in 2011 compared to $41 million in

2010. See Trading Risk Management on page 107 for a description

of our VaR calculation for the market-based trading portfolio.

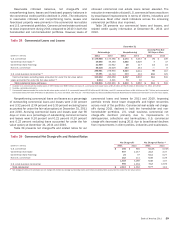

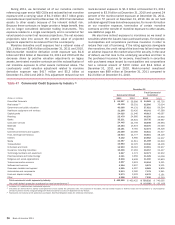

Tables 48 and 49 present the maturity profiles and the credit

exposure debt ratings of the net credit default protection portfolio

at December 31, 2011 and 2010. The distribution of debt ratings

for net notional credit default protection purchased is shown as a

negative amount.

Table 48

Less than or equal to one year

Greater than one year and less than or equal to five years

Greater than five years

Total net credit default protection

Net Credit Default Protection by Maturity Profile

December 31

2011

16%

77

7

100%

2010

14%

80

6

100%

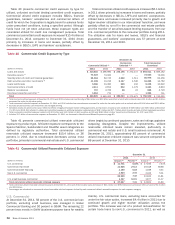

Table 49

(Dollars in millions)

Ratings (1, 2)

AAA

AA

A

BBB

BB

B

CCC and below

NR (3)

Total net credit default protection

Net Credit Default Protection by Credit Exposure Debt Rating

December 31

2011

Net

Notional

$ (32)

(779)

(7,184)

(7,436)

(1,527)

(1,534)

(661)

(203)

$ (19,356)

Percent of

Total

0.2%

4.0

37.1

38.4

7.9

7.9

3.4

1.1

100.0%

2010

Net

Notional

$—

(188)

(6,485)

(7,731)

(2,106)

(1,260)

(762)

(1,586)

$ (20,118)

Percent of

Total

—%

0.9

32.2

38.4

10.5

6.3

3.8

7.9

100.0%

(1) Ratings are refreshed on a quarterly basis.

(2) The Corporation considers ratings of BBB- or higher to meet the definition of investment grade.

(3) In addition to names which have not been rated, “NR” includes $(15) million and $(1.5) billion in net credit default swap index positions at December 31, 2011 and 2010. While index positions are

principally investment grade, credit default swap indices include names in and across each of the ratings categories.

In addition to our net notional credit default protection

purchased to cover the funded and unfunded portion of certain

credit exposures, credit derivatives are used for market-making

activities for clients and establishing positions intended to profit

from directional or relative value changes. We execute the majority

of our credit derivative trades in the OTC market with large,

multinational financial institutions, including broker/dealers and,

to a lesser degree, with a variety of other investors. Because these

transactions are executed in the OTC market, we are subject to

settlement risk. We are also subject to credit risk in the event that

these counterparties fail to perform under the terms of these

contracts. In most cases, credit derivative transactions are

executed on a daily margin basis. Therefore, events such as a

credit downgrade, depending on the ultimate rating level, or a

breach of credit covenants would typically require an increase in

the amount of collateral required of the counterparty, where

applicable, and/or allow us to take additional protective measures

such as early termination of all trades.

Table 50 presents the total contract/notional amount of credit

derivatives outstanding and includes both purchased and written

credit derivatives. The credit risk amounts are measured as the

net replacement cost in the event the counterparties with contracts

in a gain position to us fail to perform under the terms of those

contracts. For information on our written credit derivatives, see

Note 4 – Derivatives to the Consolidated Financial Statements.