Bank of America 2011 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

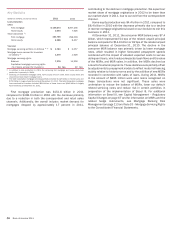

40 Bank of America 2011

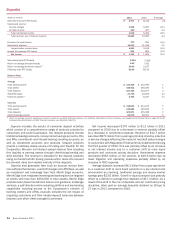

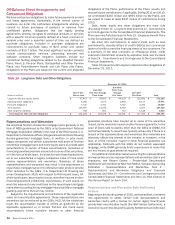

Key Statistics

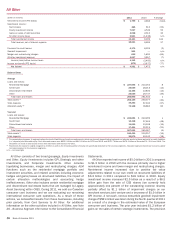

(Dollars in millions, except as noted)

Loan production

CRES:

First mortgage

Home equity

Total Corporation (1):

First mortgage

Home equity

Year end

Mortgage servicing portfolio (in billions) (2, 3)

Mortgage loans serviced for investors

(in billions) (3)

Mortgage servicing rights:

Balance

Capitalized mortgage servicing rights

(% of loans serviced for investors)

2011

$ 139,273

3,694

151,756

4,388

$ 1,763

1,379

7,378

54

bps

2010

$ 287,236

7,626

298,038

8,437

$ 2,057

1,628

14,900

92

bps

(1) In addition to loan production in CRES, the remaining first mortgage and home equity loan

production is primarily in GWIM.

(2) Servicing of residential mortgage loans, home equity lines of credit, home equity loans and

discontinued real estate mortgage loans.

(3) The total Corporation mortgage servicing portfolio included $1,029 billion in Home Loans and

$734 billion in Legacy Asset Servicing at December 31, 2011. The total Corporation mortgage

loans serviced for investors included $831 billion in Home Loans and $548 billion in Legacy

Asset Servicing at December 31, 2011.

First mortgage production was $151.8 billion in 2011

compared to $298.0 billion in 2010 with the decrease primarily

due to a reduction in both the correspondent and retail sales

channels. Additionally, the overall industry market demand for

mortgages dropped by approximately 17 percent in 2011,

contributing to the decline in mortgage production. We expect our

market share of mortgage originations in 2012 to be lower than

our market share in 2011, due to our exit from the correspondent

channel.

Home equity production was $4.4 billion in 2011 compared to

$8.4 billion in 2010 with the decrease primarily due to a decline

in reverse mortgage originations based on our decision to exit this

business in 2011.

At December 31, 2011, the consumer MSR balance was $7.4

billion, which represented 54 bps of the related unpaid principal

balance compared to $14.9 billion or 92 bps of the related unpaid

principal balance at December 31, 2010. The decline in the

consumer MSR balance was primarily driven by lower mortgage

rates, which resulted in higher forecasted prepayment speeds

combined with the impact of elevated expected costs to service

delinquent loans, which reduced expected cash flows and the value

of the MSRs, and MSR sales. In addition, the MSRs declined as

a result of customer payments. These declines were partially offset

by adjustments to prepayment models to reflect muted refinancing

activity relative to historic norms and by the addition of new MSRs

recorded in connection with sales of loans. During 2011, MSRs

in the amount of $896 million were sold. Gains recognized on

these transactions were not significant. These sales were

undertaken to reduce the balance of MSRs, lower our default-

related servicing costs and reduce risk in certain portfolios in

preparation of the implementation of Basel III. For additional

information on Basel III, see Capital Management – Regulatory

Capital Changes on page 67 and for information on MSRs and the

related hedge instruments, see Mortgage Banking Risk

Management on page 113 and Note 25 – Mortgage Servicing Rights

to the Consolidated Financial Statements.