Bank of America 2011 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 35

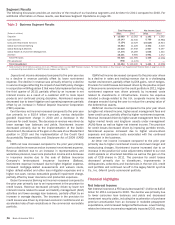

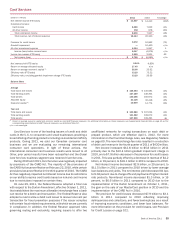

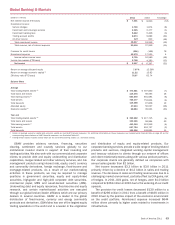

Card Services

(Dollars in millions)

Net interest income (FTE basis)

Noninterest income:

Card income

All other income

Total noninterest income

Total revenue, net of interest expense

Provision for credit losses

Goodwill impairment

All other noninterest expense

Income (loss) before income taxes

Income tax expense (FTE basis)

Net income (loss)

Net interest yield (FTE basis)

Return on average allocated equity

Return on average economic capital (1)

Efficiency ratio (FTE basis)

Efficiency ratio, excluding goodwill impairment charge (FTE basis)

Balance Sheet

Average

Total loans and leases

Total earning assets

Total assets

Allocated equity

Economic capital (1)

Year end

Total loans and leases

Total earning assets

Total assets

2011

$ 11,507

6,286

350

6,636

18,143

3,072

—

6,024

9,047

3,259

$ 5,788

9.04%

27.40

55.08

33.20

33.20

$ 126,084

127,259

130,266

21,128

10,539

$ 120,669

121,992

127,636

2010

$ 14,413

7,049

878

7,927

22,340

10,962

10,400

5,957

(4,979)

2,001

$ (6,980)

9.85%

n/m

23.62

73.22

26.66

$ 145,081

146,304

150,672

32,418

14,774

$ 137,024

138,072

138,491

% Change

(20)%

(11)

(60)

(16)

(19)

(72)

n/m

1

n/m

63

n/m

(13)

(13)

(14)

(35)

(29)

(12)

(12)

(8)

(1) Return on average economic capital and economic capital are non-GAAP financial measures. For additional information on these measures, see Supplemental Financial Data on page 32 and for

corresponding reconciliations to GAAP financial measures, see Statistical Table XVI.

n/m = not meaningful

Card Services is one of the leading issuers of credit and debit

cards in the U.S. to consumers and small businesses providing a

broad offering of lending products including co-branded and affinity

products. During 2011, we sold our Canadian consumer card

business and we are evaluating our remaining international

consumer card operations. In light of these actions, the

international consumer card business results were moved to All

Other, prior period results have been reclassified and the Global

Card Services business segment was renamed Card Services.

During 2010 and 2011, Card Services was negatively impacted

by provisions of the CARD Act. The majority of the provisions of

the CARD Act became effective on February 22, 2010, while certain

provisions became effective in the third quarter of 2010. The CARD

Act has negatively impacted net interest income due to restrictions

on our ability to reprice credit cards based on risk and card income

due to restrictions imposed on certain fees.

On June 29, 2011, the Federal Reserve adopted a final rule

with respect to the Durbin Amendment, effective October 1, 2011,

that established the maximum allowable interchange fees a bank

can receive for a debit card transaction. The Federal Reserve also

adopted a rule to allow a debit card issuer to recover one cent per

transaction for fraud prevention purposes if the issuer complies

with certain fraud-related requirements, with which we are currently

in compliance. In addition, the Federal Reserve approved rules

governing routing and exclusivity, requiring issuers to offer two

unaffiliated networks for routing transactions on each debit or

prepaid product, which are effective April 1, 2012. For more

information on the final interchange rules, see Regulatory Matters

on page 60. The new interchange fee rules resulted in a reduction

of debit card revenue in the fourth quarter of 2011 of $430 million.

Net income increased $12.8 billion to $5.8 billion in 2011

primarily due to the $10.4 billion goodwill impairment charge in

2010, and a $7.9 billion decrease in the provision for credit losses

in 2011. This was partially offset by a decrease in revenue of $4.2

billion, or 19 percent, to $18.1 billion in 2011 compared to 2010.

Net interest income decreased $2.9 billion, or 20 percent, to

$11.5 billion in 2011 compared to 2010 driven by lower average

loan balances and yields. The net interest yield decreased 81 bps

to 9.04 percent due to charge-offs and paydowns of higher interest

rate products. Noninterest income decreased $1.3 billion, or 16

percent, to $6.6 billion in 2011 compared to 2010 due to the

implementation of the Durbin Amendment on October 1, 2011,

the gain on the sale of our MasterCard position in 2010 and the

implementation of the CARD Act in 2010.

The provision for credit losses decreased $7.9 billion to $3.1

billion in 2011 compared to 2010 reflecting improving

delinquencies and collections, and fewer bankruptcies as a result

of improving economic conditions, and lower loan balances. For

more information on the provision for credit losses, see Provision

for Credit Losses on page 102.