Bank of America 2011 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

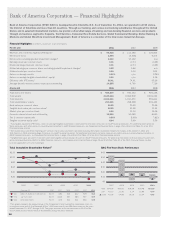

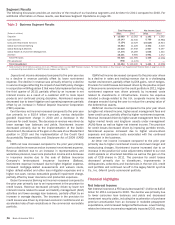

26 Bank of America 2011

Segment Results

The following discussion provides an overview of the results of our business segments and All Other for 2011 compared to 2010. For

additional information on these results, see Business Segment Operations on page 33.

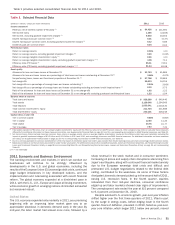

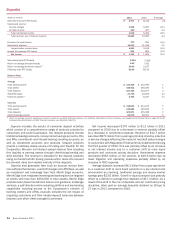

Table 3

(Dollars in millions)

Deposits

Card Services

Consumer Real Estate Services

Global Commercial Banking

Global Banking & Markets

Global Wealth & Investment Management

All Other

Total FTE basis

FTE adjustment

Total Consolidated

Business Segment Results

Total Revenue (1)

2011

$ 12,689

18,143

(3,154)

10,553

23,618

17,376

15,201

94,426

(972)

$ 93,454

2010

$ 13,562

22,340

10,329

11,226

27,949

16,289

9,695

111,390

(1,170)

$110,220

Net Income (Loss)

2011

$ 1,192

5,788

(19,529)

4,402

2,967

1,635

4,991

1,446

—

$ 1,446

2010

$ 1,362

(6,980)

(8,947)

3,218

6,297

1,340

1,472

(2,238)

—

$ (2,238)

(1) Total revenue is net of interest expense and is on a FTE basis which is a non-GAAP financial measure. For more information on this measure, see Supplemental Financial Data on page 32, and for

a corresponding reconciliation to a GAAP financial measure, see Table XV.

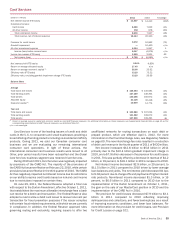

Deposits net income decreased compared to the prior year due

to a decline in revenue partially offset by lower noninterest

expense. The decline in revenue was primarily driven by a decline

in service charges reflecting the impact of overdraft policy changes

in conjunction with Regulation E that were fully implemented during

the third quarter of 2010, partially offset by an increase in net

interest income as a result of a customer shift to more liquid

products and continued pricing discipline. Noninterest expense

decreased due to lower litigation and operating expenses partially

offset by an increase in Federal Deposit Insurance Corporation

(FDIC) expense.

Card Services net income increased compared to the prior year

due primarily to a $10.4 billion non-cash, non-tax deductible

goodwill impairment charge in 2010 and a decrease in the

provision for credit losses. The decrease in revenue was driven by

lower average loan balances and yields. Noninterest income

decreased primarily due to the implementation of the Durbin

Amendment, the absence of the gain on the sale of our MasterCard

position in 2010 and the implementation of the Credit Card

Accountability Responsibility and Disclosure Act of 2009 (CARD

Act).

CRES net loss increased compared to the prior year primarily

due to a decline in revenue and an increase in noninterest expense.

Revenue declined due to an increase in representations and

warranties provision, lower core production income and a decrease

in insurance income due to the sale of Balboa Insurance

Company’s lender-placed insurance business (Balboa).

Noninterest expense increased due to higher litigation expense,

increased mortgage-related assessments and waivers costs,

higher default-related and other loss mitigation expenses and a

higher non-cash, non-tax deductible goodwill impairment charge,

partially offset by lower insurance and production expenses.

Global Commercial Banking net income increased compared to

the prior year primarily due to an improvement in the provision for

credit losses. Revenue decreased primarily driven by lower net

interest income related to asset and liability management (ALM)

activities and lower average loan balances, partially offset by an

increase in average deposits. The decrease in the provision for

credit losses was driven by improved economic conditions and an

accelerated rate of loan resolutions in the commercial real estate

portfolio.

GBAM net income decreased compared to the prior year driven

by a decline in sales and trading revenue due to a challenging

market environment, partially offset by DVA gains, net of hedges.

Provision for credit losses decreased driven by the positive impact

of the economic environment on the credit portfolio in 2011. Higher

noninterest expense was driven primarily by increased costs

related to investments in infrastructure. Income tax expense

included a charge related to the U.K. corporate income tax rate

changes enacted during the year to reduce the carrying value of

the deferred tax assets.

GWIM net income increased compared to the prior year driven

by higher net interest income, higher asset management fees and

lower credit costs, partially offset by higher noninterest expense.

Revenue increased driven by higher asset management fees from

higher market levels and long-term assets under management

(AUM) flows as well as higher net interest income. The provision

for credit losses decreased driven by improving portfolio trends.

Noninterest expense increased due to higher volume-driven

expenses and personnel costs associated with the continued

investment in the business.

All Other net income increased compared to the prior year

primarily due to higher noninterest income and lower merger and

restructuring charges. Noninterest income increased due to an

increase in the positive fair value adjustments related to our own

credit spreads on structured liabilities as well as the gain on the

sale of CCB shares in 2011. The provision for credit losses

decreased primarily due to divestitures, improvements in

delinquencies, collections and insolvencies in the non-U.S. credit

card portfolio and continued run-off in the legacy Merrill Lynch &

Co., Inc. (Merrill Lynch) commercial portfolio.

Financial Highlights

Net Interest Income

Net interest income on a FTE basis decreased $7.1 billion to $45.6

billion for 2011 compared to 2010. The decline was primarily due

to lower consumer loan balances and yields and decreased

investment security yields, including the acceleration of purchase

premium amortization from an increase in modeled prepayment

expectations, and increased hedge ineffectiveness. Lower trading-

related net interest income also negatively impacted 2011 results.