Bank of America 2011 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

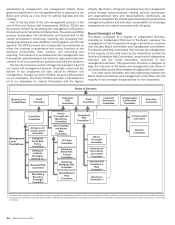

60 Bank of America 2011

the mortgages in the Covered Trusts for these documentation

issues.

We estimate that the costs associated with additional servicing

obligations under the BNY Mellon Settlement contributed $400

million to the 2011 valuation charge related to the MSR asset.

The additional servicing actions are consistent with the consent

orders with the OCC and the Federal Reserve.

In addition, in connection with the Servicing Resolution

Agreements, BANA has agreed to implement certain additional

servicing changes. The uniform servicing standards established

under the Servicing Resolution Agreements are broadly consistent

with the residential mortgage servicing practices imposed by the

OCC consent order, however they are more prescriptive and cover

a broader range of our residential mortgage servicing activities.

These standards are intended to strengthen procedural

safeguards and documentation requirements associated with

foreclosure, bankruptcy, and loss mitigation activities, as well as

addressing the imposition of fees and the integrity of

documentation, with a goal of ensuring greater transparency for

borrowers. These uniform servicing standards also obligate us to

implement compliance processes reasonably designed to provide

assurance of the achievement of these objectives. Compliance

with the uniform servicing standards will be assessed by a monitor

based on the measurement of outcomes with respect to these

objectives. Implementation of these uniform servicing standards

is expected to incrementally increase costs associated with the

servicing process, but is not expected to result in material delays

or dislocation in the performance of our mortgage servicing

obligations, including the completion of foreclosures.

Regulatory Matters

See Item 1A. Risk Factors of this Annual Report on Form 10-K and

Note 14 – Commitments and Contingencies to the Consolidated

Financial Statements for additional information regarding

regulatory matters and risks.

Financial Reform Act

The Dodd-Frank Wall Street Reform and Consumer Protection Act

(Financial Reform Act), which was signed into law on July 21, 2010,

enacts sweeping financial regulatory reform and has altered and

will continue to alter the way in which we conduct certain

businesses, increase our costs and reduce our revenues. Many

aspects of the Financial Reform Act remain subject to final

rulemaking and will take effect over several years, making it difficult

to anticipate the precise impact on the Corporation, our customers

or the financial services industry.

Debit Interchange Fees

On June 29, 2011, the Federal Reserve adopted a final rule with

respect to the Durbin Amendment effective on October 1, 2011

which, among other things, established a regulatory cap for many

types of debit interchange transactions to equal no more than 21

cents plus five bps of the value of the transaction. The Federal

Reserve also adopted a rule to allow a debit card issuer to recover

one cent per transaction for fraud prevention purposes if the issuer

complies with certain fraud-related requirements, with which we

are currently in compliance. The Federal Reserve also approved

rules governing routing and exclusivity, requiring issuers to offer

two unaffiliated networks for routing transactions on each debit

or prepaid product, which are effective April 1, 2012. For additional

information, see Card Services on page 35.

Limitations on Proprietary Trading

On October 11, 2011, the Federal Reserve, OCC, FDIC and

Securities and Exchange Commission (SEC), representing four of

the five regulatory agencies charged with promulgating regulations

implementing limitations on proprietary trading as well as the

sponsorship of or investment in hedge funds and private equity

funds (the Volcker Rule) established by the Financial Reform Act,

released for comment proposed implementing regulations. On

January 11, 2012, the Commodity Futures Trading Commission

(CFTC), the fifth agency, released for comment its proposed

regulations under the Volcker Rule. The proposed regulations

include clarifications to the definition of proprietary trading and

distinctions between permitted and prohibited activities. However,

in light of the complexity of the proposed regulations and the large

volume of comments received (the proposal requested comments

on over 1,300 questions on 400 different topics), it is not possible

to predict the content of the final regulations or when they will be

issued.

The statutory provisions of the Volcker Rule will become

effective on July 21, 2012, whether or not the final regulations are

adopted, and it gives certain financial institutions two years from

the effective date, with opportunities for additional extensions, to

bring activities and investments into compliance. Although GBAM

exited its stand-alone proprietary trading business as of June 30,

2011 in anticipation of the Volcker Rule and further to our initiative

to optimize our balance sheet, the ultimate impact of the Volcker

Rule on us remains uncertain. However, based upon the content

of the proposed regulations, it is possible that the implementation

of the Volcker Rule could limit or restrict our remaining trading

activities. Implementation of the Volcker Rule could also limit or

restrict our ability to sponsor and hold ownership interests in hedge

funds, private equity funds and other subsidiary operations,

increase our operational and compliance costs, reduce our trading

revenues and adversely affect our results of operations. For

additional information about our trading business, see GBAM on

page 43.

Derivatives

The Financial Reform Act includes measures to broaden the scope

of derivative instruments subject to regulation by requiring clearing

and exchange trading of certain derivatives; imposing new capital,

margin, reporting, registration and business conduct requirements

for certain market participants; and imposing position limits on

certain OTC derivatives. The Financial Reform Act required

regulators to promulgate the rulemakings necessary to implement

these regulations by July 16, 2011. However, the rulemaking

process was not completed as of this date, and is not expected

to conclude until well into 2012. Further, the regulators granted

temporary relief from certain requirements that would have taken

effect on July 16, 2011 absent any rulemaking. The SEC temporary

relief is effective until final rules relevant to each requirement

become effective. The CFTC temporary relief is effective until the

earlier of July 16, 2012 or the date on which final rules relevant

to each requirement become effective. The ultimate impact of

these derivatives regulations and the time it will take to comply

continues to remain uncertain. The final regulations will impose

additional operational and compliance costs on us and may require

us to restructure certain businesses, thereby negatively impacting

our revenues and results of operations.